How to Write an Insurance Appraisal Demand Letter

Your car insurance policy is more than just a monthly bill; it’s a contract filled with rights you might not even know you have. When an insurance company gives you a lowball offer for your vehicle’s damage or diminished value, it can feel like they hold all the power. But hidden within your policy is a powerful tool designed for this exact situation: the appraisal clause. To activate this right, you need to send a formal insurance appraisal demand letter. This letter is your official notice that you are moving the dispute out of a frustrating negotiation and into a binding resolution process. It tells the insurer that you understand your rights and are prepared to enforce them. This guide will walk you through when and how to use this letter to take control of your claim and fight for the full compensation you are owed.

Key Takeaways

- Use Appraisal for Value Disputes Only: This process is your best move when the only disagreement is about money, like the cost of repairs or your car’s diminished value. It is not designed to solve arguments over who was at fault or if your claim is covered by the policy.

- Build Your Case Before You Write: A strong demand letter is backed by solid proof. Before writing, collect all your key documents like independent repair estimates, damage photos, and your insurance policy. This preparation shows the insurer you are serious and ready to support your claim.

- Understand the Process is Binding: Once the appraisal process is complete, the decision on your claim’s value is legally final. Since you only get one shot, it’s critical to have a strong strategy and a qualified appraiser in your corner from the very beginning.

What Is an Insurance Appraisal Demand Letter?

When you and your insurance company can’t agree on the cost of your car’s repairs or its loss in value, it can feel like you’ve hit a dead end. But your policy likely has a built-in tool for this exact situation: the appraisal clause. An insurance appraisal demand letter is the formal letter you send to the insurer to officially start this process. It’s your way of saying, “We disagree on the numbers, so let’s bring in some independent experts to figure out a fair amount.” This isn’t a request for the insurance company to simply reconsider its offer. It’s a powerful step that legally requires them to participate in the appraisal process as outlined in your policy.

Sending this letter moves your claim out of a frustrating back-and-forth negotiation and into a structured dispute resolution process. It’s a critical tool for holding insurers accountable and is often used to fight for fair compensation in property damage and diminished value claims. By formally invoking this clause, you take control of the situation instead of waiting for the insurer to make a better offer that may never come. It signals that you understand your rights and are prepared to enforce them. While you can write this letter yourself, having an attorney handle it ensures the language is precise and legally sound, showing the insurer you are serious about getting what you’re owed from the very beginning.

Appraisal Demand vs. Standard Demand Letter

It’s easy to confuse an appraisal demand letter with a standard demand letter, but they serve very different functions. A standard demand letter is a broad request for payment that can cover all aspects of your claim. An appraisal demand letter has one specific job: to resolve a disagreement over the dollar amount of your loss.

Think of it this way: if you and the insurer agree that the accident caused the damage (this is called “coverage”) but are miles apart on the repair cost, the appraisal process is the right tool. An insurance appraisal is used when the only thing left to argue about is the money. It doesn’t address who was at fault or whether your policy covers the incident in the first place. It’s a focused, efficient way to settle a valuation dispute without getting into a larger legal battle.

Your Policy’s Appraisal Clause: What It Is and Where to Find It

The appraisal clause is the part of your insurance contract that gives you the right to demand an appraisal. It’s a powerful but often overlooked provision. This clause typically states that if you and the insurance company fail to agree on the amount of loss, either party can make a written demand for an appraisal.

To find it, pull out your auto insurance policy documents and look for a section titled “Physical Damage Coverage,” “Damage to Your Auto,” or something similar. The language is usually very direct. As the legal experts at Pro Policyholder explain, the clause provides a clear path for resolving valuation disputes. Once invoked, it sets a specific process in motion where both you and the insurer hire independent appraisers to settle the matter. Knowing this clause exists is the first step toward using it to your advantage.

When Should You Send an Appraisal Demand?

Knowing when to send an appraisal demand letter is just as important as knowing how to write it. This isn’t your first move; it’s a strategic step for when the claims process goes sideways. Invoking your policy’s appraisal clause formally tells the insurer you’re serious about getting a fair payout and can break a stalemate. Here are the key moments when sending this letter makes the most sense.

You’ve Received a Lowball Offer

It’s common for an insurer’s first offer to be disappointingly low. They are often hoping you’ll accept a quick, small payout and move on. If your own repair estimates show the damages are worth significantly more, this is your cue. Instead of getting stuck in endless arguments, sending an appraisal demand formally rejects their lowball number. It shows you are serious about getting what your claim is actually worth and moves the process toward an evaluation based on evidence, not the insurer’s opening bid.

You Disagree on the Payout, Not the Cause

The appraisal process is designed for a very specific disagreement: when you and the insurer agree on what caused the damage but can’t agree on the cost to fix it. This process isn’t for debating who was at fault or whether your policy covers the incident. It’s strictly for disputes over the dollar amount. If the only thing holding up your claim is a disagreement over the value of the damage or the cost of repairs, invoking the appraisal clause is the right move to get things unstuck and bring in neutral experts to assess the loss.

Negotiations Have Hit a Wall

Have you gone back and forth with the claims adjuster, only for them to refuse to move from their initial position? When good-faith negotiations break down, you need a new strategy. Sending a formal appraisal demand letter is a powerful way to break the stalemate. It takes the decision out of the hands of an uncooperative adjuster and puts it into a structured, impartial process defined by your policy. When you’ve hit a wall, Gastley Law can help you with all of your property damage claims.

To Settle a Diminished Value Dispute

Even after perfect repairs, a car with an accident history is worth less than it was before the crash. This loss in value is known as diminished value, and it’s a frequent point of conflict with insurers. They might deny the claim outright or offer a fraction of what you’ve actually lost. The appraisal clause is a perfect tool for fighting this. It allows you to challenge a low diminished value offer by bringing in an independent expert to assess the true loss in your vehicle’s market value, providing a credible figure to counter the insurer’s lowball number.

What to Gather Before You Write Your Letter

Sending an appraisal demand letter isn’t something you should do on a whim. To make your letter as effective as possible, you need to do a little homework first. Think of it as building your case file before you ever step into a “courtroom.” When you have all your evidence organized and ready to go, you’re not just sending a letter; you’re presenting a well-supported argument that the insurance company can’t easily ignore. This preparation is the foundation of a successful appraisal demand and can dramatically shift the dynamic in your favor.

Taking the time to gather these documents accomplishes two things. First, it makes the writing process much smoother, as you’ll have all the necessary facts and figures at your fingertips. Second, and more importantly, it signals to the insurer that you are serious, organized, and prepared to fight for the fair value you’re owed. It shows them you’re not an easy target for a lowball offer. An unprepared claimant might be seen as someone who will eventually give up, but a well-documented claim demands respect and proper attention. Before you type a single word, make sure you have these key items on hand.

Your Policy and All Correspondence

First things first, grab your car insurance policy. You’ll need to read through it carefully to find the appraisal clause. This is usually located in the section covering physical damage, which might be labeled “Damage to Your Auto” or something similar. This clause is the key that allows you to formally demand an appraisal, so confirming its existence is your starting point. Alongside your policy, gather every piece of communication you’ve had with the insurance company. This includes emails, formal letters, and any other documents they’ve sent you. Having a complete record creates a clear paper trail of your claim’s history and the insurer’s initial offers. If you’re struggling to interpret the language in your policy, our team can help you understand your rights and our services.

Independent Repair Estimates

The insurance company has its own idea of what your repairs should cost, but that doesn’t mean you have to accept it. This is where independent repair estimates become your best friend. Take your vehicle to one or two reputable body shops and ask for detailed estimates for the repairs. These documents from third-party experts serve as a powerful benchmark for what your claim is actually worth. They provide concrete evidence that the insurer’s offer is too low and substantiate your demand for a higher amount. When you have professional estimates in hand, you’re no longer just arguing about opinions; you’re presenting facts. This strengthens your position significantly in any negotiation or appraisal process.

Photos and Damage Records

A picture is worth a thousand words, especially when it comes to property damage. Before any repairs are made, take clear, well-lit photographs of your vehicle from every angle. Capture wide shots of the car and close-ups of every dent, scratch, and broken part. This visual evidence is crucial for showing the true extent of the damage. In addition to photos, keep a folder with all your repair bills and receipts. This documentation creates an undeniable record of the damages and the costs incurred to fix them. This evidence is vital for supporting your claim for repair costs and for proving the diminished value of your car after the accident.

A Log of Your Insurer Communications

Keeping track of conversations can feel tedious, but it’s an essential step. Create a simple log of every phone call and interaction you have with the insurance company. For each entry, note the date, the time, the name of the person you spoke with, and a brief summary of the conversation. This detailed record helps you keep your facts straight and prevents the insurer from going back on their word. It also shows that you are an organized and diligent claimant. If things get complicated and you find yourself overwhelmed by the back-and-forth, it might be a sign that you need support. Don’t hesitate to contact us for guidance on how to handle difficult insurer communications.

What to Include in Your Appraisal Demand Letter

Think of your appraisal demand letter as your official opening move. It needs to be clear, professional, and leave no room for misinterpretation. Getting it right from the start can prevent unnecessary back-and-forth and show the insurance company you mean business. Your letter should be a complete package that contains everything the insurer needs to process your request without delay. Let’s walk through exactly what you need to include to make your letter as effective as possible.

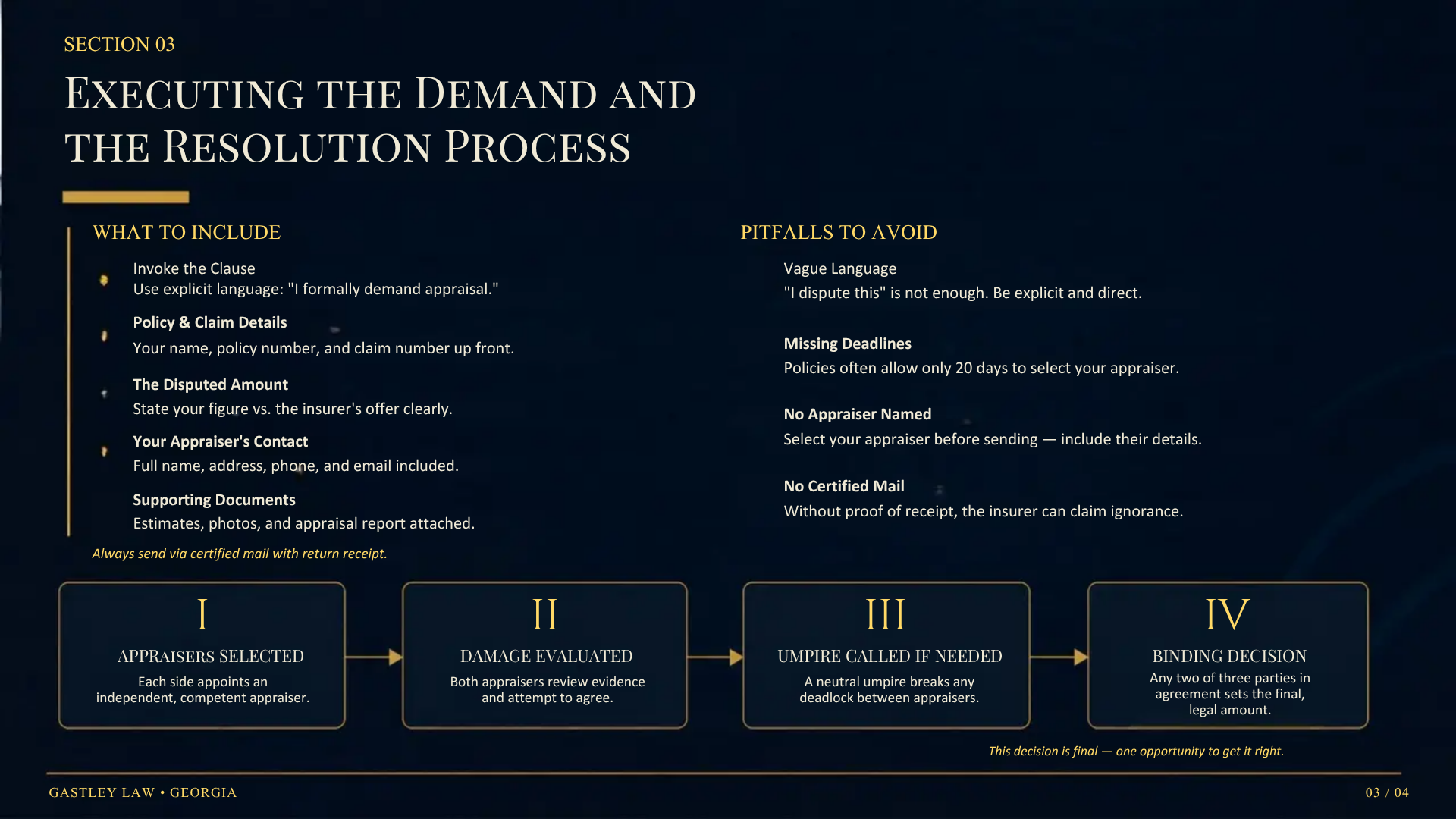

Formally State You’re Invoking the Appraisal Clause

This is the most important part of your letter, so don’t bury it. Start by clearly and formally stating that you are invoking the appraisal clause in your policy. Use direct language like, “I am writing to make a formal demand for appraisal” or “This letter serves as my formal invocation of the appraisal clause.” This sets a serious tone and immediately communicates your intent. Vague language can give the insurer an excuse to ignore or misinterpret your request. By being direct, you create an official record of your demand and start the clock on the appraisal process, putting the ball squarely in their court to respond.

Your Policy and Claim Information

To avoid any administrative delays, make it easy for the insurance company to find your file. Near the top of your letter, clearly list your full name, policy number, and claim number. This information is essential for the claims adjuster to locate your case and begin the process. Before you write, double-check your policy documents, usually under a section like “Damage to Your Auto” or “Physical Damage Coverage,” to confirm the appraisal clause exists and to have your policy number handy. Including these details upfront shows you are organized and helps streamline the entire procedure, getting you closer to a fair resolution.

The Specific Amount in Dispute

Your letter needs to be specific about the money. The appraisal clause is designed to resolve disagreements over the amount of a loss, not whether the loss is covered. Clearly state the dollar amount you believe you are owed and how it differs from the insurer’s offer. For example, you might write, “The insurance company has offered $2,000 for the diminished value of my vehicle, but my independent appraisal values the loss at $5,500, leaving a disputed amount of $3,500.” This precision is crucial, whether you’re disputing repair costs or the vehicle’s diminished value after an accident. Being explicit removes ambiguity and focuses the appraisal process on the exact financial disagreement.

Your Appraiser’s Contact Details

Invoking the appraisal clause means you have to select your own competent, independent appraiser. Once you’ve chosen someone, you must include their full name, business address, phone number, and email address in your demand letter. This is not an optional step. The insurance company’s appraiser will need to coordinate directly with yours to either reach an agreement or select a neutral umpire. Providing this information from the outset demonstrates that you are prepared and serious about moving forward. It signals that you have already taken concrete steps to support your claim, which can encourage the insurer to take your demand more seriously.

Attach Your Supporting Documents

Your letter is your official demand, but your supporting documents are your proof. Gather and attach copies of everything that substantiates your claim. This includes your independent appraisal report, photos of the damage, repair estimates from trusted body shops, and any other evidence you’ve collected. Organizing these documents and including them with your letter builds a powerful, evidence-based case from the very beginning. It provides the insurance company with all the information they need to understand your position fully. Our firm can help you identify and organize the crucial evidence needed for these types of property damage claims. A well-documented claim is much harder for an insurer to dismiss.

Send It via Certified Mail

Once your letter is written and your documents are attached, don’t just drop it in a standard mailbox. Send your entire packet via certified mail with a return receipt requested. This step is critical because it provides you with legal proof that the insurance company received your demand and on what date. The return receipt will be mailed back to you with a signature from the recipient. This creates an official paper trail and prevents the insurer from claiming they never got your letter. It holds them accountable for responding within the timeframe specified by your policy or state law, ensuring your claim keeps moving forward.

Common Mistakes to Avoid

Writing an appraisal demand letter is a powerful step, but a few simple errors can derail the process before it even starts. Insurance companies handle these letters all the time, and they know what to look for. Any mistake can give them a reason to delay or deny your request. To make sure your letter is effective, you need to be precise and professional. Think of it like building a case; every piece needs to be in the right place. Let’s walk through the most common pitfalls so you can sidestep them and keep your claim moving forward.

Being Vague About Invoking the Clause

This isn’t the time for subtle hints. Your letter needs to be crystal clear that you are formally invoking the appraisal clause in your policy. A common mistake is using language that’s too soft or ambiguous, which an insurer might choose to interpret as a simple inquiry rather than a formal demand. You should explicitly state something like, “I formally demand appraisal for my claim.” This direct language removes any doubt about your intentions and legally triggers the appraisal process outlined in your policy. Being direct shows the insurance company you understand your rights and are serious about getting a fair valuation for your diminished value claim.

Missing Key Deadlines

The appraisal process runs on a strict clock, and missing a deadline can be fatal to your claim. Once you send your demand letter, the countdown begins. Your policy will specify the timelines, but often you and the insurance company have a set number of days, like 20 days, to select your respective appraisers. If you fail to name your appraiser within this window, you could forfeit your right to the appraisal process entirely. Read your policy’s appraisal clause carefully to understand every deadline. Acting quickly is essential. If you’re feeling overwhelmed by the timelines, remember that legal professionals handle these processes daily.

Forgetting Your Appraiser’s Information

When you demand appraisal, you also need to show you’ve done your homework. This means you should have already selected a qualified, independent appraiser before you even send the letter. A frequent error is sending a demand without including your appraiser’s details. Your letter should name your chosen appraiser and provide their complete contact information. Including this upfront does two things: it shows the insurer you are prepared and serious, and it prevents unnecessary delays. The insurance company’s appraiser needs to be able to contact yours, so giving them the information from the start streamlines the entire process and gets you closer to a resolution.

Not Sending via Certified Mail for Proof

If you send your demand letter with a standard stamp and drop it in a mailbox, you have no official proof the insurance company ever received it. This is a critical mistake. Always send your appraisal demand letter via certified mail with a return receipt requested. This method gives you a paper trail proving exactly when you sent the letter and when the insurance company signed for it. This documentation is your evidence. If the insurer later claims they never got your demand or tries to argue you missed a deadline, your certified mail receipt is your defense. It’s a small, inexpensive step that provides invaluable protection for your claim. If you need help ensuring every step of your claim is properly documented, don’t hesitate to contact us.

What Happens After You Send the Letter?

Once you’ve sent your appraisal demand letter by certified mail, you’ve officially started a formal process to resolve the dispute with your insurer. It can feel a little intimidating, but think of it as a structured path forward when negotiations have stalled. This process is outlined in your policy for a reason: to provide a fair, evidence-based way to determine the true value of your claim without having to go to court. Here’s a step-by-step look at what you can expect next.

Step 1: Each Side Picks an Appraiser

The first thing that happens is both you and the insurance company choose your own appraiser. This person should be a competent and impartial expert who will advocate for a fair valuation on your behalf. It’s crucial to select someone with experience in vehicle damage and valuation, especially if you are fighting for a fair diminished value settlement. Your appraiser will act as your representative in this process, so take your time to find a qualified professional who understands the specifics of your case and is prepared to argue for the amount you are rightfully owed.

Step 2: Appraisers Evaluate the Damage

After both sides have selected their experts, the two appraisers get to work. Their job is to independently review all the evidence, including repair estimates, damage photos, and your vehicle’s condition, to determine the amount of loss. They will then communicate with each other and attempt to reach an agreement. In many situations, two competent professionals can look at the same set of facts and come to a reasonable consensus on the value. This is the ideal outcome, as it resolves the dispute quickly and efficiently without needing to involve anyone else.

Step 3: A Neutral Umpire Breaks Any Tie

If your appraiser and the insurance company’s appraiser can’t agree on a final number, they will bring in a third person to break the deadlock. This individual is called an umpire, and they must be a neutral and competent expert. Both appraisers must agree on who to select as the umpire. If they can’t agree, a court may be asked to appoint one. The umpire reviews the evidence and arguments from both sides and makes an independent judgment. Our firm’s legal representation can be invaluable at this stage, ensuring a truly impartial umpire is chosen to oversee the process.

Step 4: A Final, Binding Decision Is Made

The appraisal process concludes when a final decision on the value is reached. An agreement by any two of the three parties (for example, your appraiser and the umpire) sets the final amount of the loss. This decision is legally binding, which means both you and the insurance company must accept it. You will be paid the agreed-upon amount, and the dispute over the value is officially closed. Because this outcome is final, it’s important to have a strong case and a skilled appraiser from the very beginning. If you have questions about what a binding decision means for your claim, feel free to contact us for guidance.

Pros and Cons of the Appraisal Process

Deciding to invoke your policy’s appraisal clause is a big step, and it’s smart to weigh the potential benefits against the drawbacks. While the appraisal process can be a powerful tool for getting a fair payout from your insurance company, it isn’t the right path for every situation. Understanding the pros and cons helps you make an informed decision about how to proceed with your property damage claim and fight for the compensation you deserve. This process is all about resolving disagreements over the value of your loss, so it’s most effective when you and the insurer agree that the damage is covered but are far apart on the repair costs or the vehicle’s diminished value.

Pro: It’s Faster and Cheaper Than Court

One of the biggest draws of the appraisal process is its efficiency. If you’re staring down a lowball offer and negotiations have stalled, the thought of a lengthy and expensive court battle can be daunting. The appraisal process offers a more direct alternative. For many policyholders, this is a significant advantage because the process is often quicker and costs less than a lawsuit. You can get a resolution without getting bogged down in the legal system for months or even years, allowing you to get your vehicle repaired and move on with your life sooner.

Pro: You Get an Expert Opinion on Value

When you invoke appraisal, you aren’t just rolling the dice. You get to select an appraiser who is an expert in the specific type of damage your vehicle sustained. This is especially critical for complex issues like diminished value, where a standard insurance adjuster may lack the specialized knowledge to assess your car’s loss in market value accurately. Having a true expert on your side can make all the difference. A knowledgeable appraiser understands the nuances of your claim and can build a strong, evidence-based case to help you secure the highest possible payment for your damages.

Con: The Decision Is Usually Final

The finality of the appraisal process is both a strength and a weakness. While it provides a clear end to the dispute, it also means the outcome is typically binding. Once the appraisal panel reaches a decision on the value of your claim, that number is set in stone. It is very difficult to challenge or change the amount later unless you can prove there was fraud or the insurer acted unfairly. This makes your initial strategy and choice of appraiser incredibly important. You have one shot to present your case, so you need to make sure it’s as strong as possible from the very beginning.

Con: It Only Solves Value, Not Coverage Disputes

It’s crucial to understand what the appraisal process can and cannot do. This process is designed exclusively to resolve disagreements about the amount of loss, not whether the loss is covered in the first place. If the insurance company denies your claim outright, arguing that the damage isn’t covered by your policy, appraisal won’t help. As legal experts point out, questions of coverage “must be decided by a judge or jury.” For example, appraisal can resolve a dispute over whether a repair should cost $2,000 or $5,000, but it can’t force an insurer to pay for a repair they claim isn’t covered at all.

Con: Appraisal Costs Can Add Up

While appraisal is generally less expensive than a lawsuit, it isn’t free. Under the terms of most policies, you are responsible for paying for your own appraiser. Additionally, you and the insurance company must split the cost of the neutral umpire, who is brought in if your appraisers cannot agree. These costs can accumulate, especially if the dispute is complex. Before starting the process, you should weigh the potential costs against the amount of money in dispute. This is where getting professional advice on your property damage claim can be invaluable for determining if appraisal is the most financially sound choice for your specific claim.

Is the Appraisal Process Right for Your Claim?

The appraisal process can be a fantastic tool for breaking a stalemate with your insurance company, but it isn’t the right solution for every situation. Before you send that demand letter, it’s important to understand exactly what appraisal can and cannot do. Think of it as a specialized tool designed for a very specific job: settling disagreements over money. Deciding if it fits your claim is the first step toward getting the compensation you deserve.

When to Use Appraisal for Your Georgia Claim

You should consider invoking the appraisal clause when the disagreement with your insurer is strictly about the dollar amount of your loss. This is the perfect path forward if both you and the insurance company agree on what was damaged, but you can’t agree on how much it will cost to repair or replace it. For example, if your insurer’s estimate for repairs is $3,000 but every body shop you’ve visited quotes you $6,000, appraisal is designed to resolve that exact conflict. The same goes for a diminished value dispute where the insurer offers a low amount for your car’s lost resale value. If the argument is about the “how much,” appraisal is your most direct route to a resolution.

When to Consider Other Legal Options

Appraisal is not the right tool if your disagreement is about coverage or liability. If the insurance company is denying your claim entirely, arguing that your policy doesn’t cover the incident, or claiming the damage isn’t their responsibility, appraisal won’t help. This process can only determine the amount of loss; it cannot force an insurer to pay for a claim they have denied. For instance, if the insurer says the damage to your car was pre-existing and therefore not covered, that’s a coverage dispute. In these more complex situations, you’ll need to explore other legal options. If you’re facing a claim denial, it’s a good idea to contact an attorney to discuss your next steps.

Do You Need a Lawyer for This?

On the surface, the appraisal process seems like a neat and tidy way to settle a dispute over your car’s value. You pick an appraiser, they pick one, and a neutral third party makes the final call. Simple, right? In reality, it’s rarely that straightforward. Insurance companies have teams of people who deal with these claims every day, and they know how to use the process to their advantage. This is where having a legal expert in your corner can make all the difference. While you aren’t technically required to have a lawyer for the appraisal process, going it alone can put you at a significant disadvantage.

How an Attorney Can Strengthen Your Position

An experienced attorney does more than just file paperwork. They start by helping you decide if invoking the appraisal clause is even the right move for your specific situation. Sometimes, negotiation or another legal path is better. If the insurance company refuses to pay the final appraisal award, a lawyer can guide you through the next steps, which may involve suing the at-fault driver. It’s also important to remember what the appraisal process can’t do. Appraisers only determine the amount of loss; they don’t decide who is at fault or if your policy covers the damage in the first place. If your dispute involves questions of liability or coverage, an attorney provides the comprehensive legal representation you need to address the entire problem, not just one piece of it.

Get Help with Your Georgia Claim from Gastley Law

The appraisal process can be surprisingly slow and complicated. It can take months just to get both sides to agree on appraisers and a truly neutral umpire. Finding an appraiser who will advocate effectively for you, the policyholder, can be a challenge in itself. This is where we come in. At Gastley Law, we handle these complexities for our Georgia clients every day. We have a network of trusted, independent appraisers and know how to keep the process moving forward. You don’t have to fight the insurance company on your own. If you’re dealing with a lowball offer or a denied diminished value claim, let us take the weight off your shoulders. We’ll manage the entire process and fight to get you the full amount you’re owed. Contact us today to see how we can help.

Related Articles

- How to Write an Insurance Claim Demand Letter

- The Ultimate Diminished Value Demand Letter Guide

- Disagree With a Car Damage Appraisal? 5 Steps

Frequently Asked Questions

What if the insurance company ignores my appraisal demand letter?

This is exactly why sending the letter via certified mail is so important. The return receipt is your legal proof that they received your demand. If they ignore it, they are likely violating the terms of your insurance policy. This failure to act is a serious issue and a clear signal that you need to get a legal professional involved to enforce your rights under the contract.

Is the final appraisal amount guaranteed to be more than the insurer’s original offer?

There is no guarantee, as the goal of the process is to determine a fair and accurate value, not just a higher one. However, if you’ve done your homework and have evidence that the insurer’s offer was unreasonably low, the appraisal process is designed to correct that. By presenting a strong case with a competent appraiser, you create the best possible opportunity to secure a final amount that is significantly better than the initial lowball number.

How much will I have to pay for the appraisal process?

While it’s less expensive than a lawsuit, the process isn’t free. You are responsible for paying for your own appraiser’s services. If your appraiser and the insurer’s appraiser cannot agree and need to hire a neutral umpire to break the tie, you will typically split the cost of the umpire’s fee with the insurance company. Think of these costs as an investment in getting the full, fair value for your claim.

Can I use the appraisal process if my insurer denied my diminished value claim entirely?

No, the appraisal process is not the right tool for a complete claim denial. Appraisal is only used to settle disagreements over the dollar amount of a loss when the insurance company has already agreed to pay something. A total denial is a coverage dispute, meaning the insurer is saying your policy doesn’t cover the loss at all. This situation requires a different legal strategy to challenge the denial itself.

How long does the appraisal process typically take from start to finish?

The timeline can vary quite a bit. In a straightforward case where both sides are cooperative, it might be resolved in a month or two. However, it can take longer if there are delays in selecting appraisers, if the two appraisers cannot agree and need to select an umpire, or if the case is particularly complex. While it requires patience, this process is still generally much faster than navigating the court system.