GEICO Diminished Value Claim in Georgia

Let’s talk about the money you’re owed. A car accident costs you more than just your deductible and a few headaches. It directly impacts your vehicle’s asset value, potentially costing you thousands of dollars in lost equity. This financial hit is known as diminished value, and recovering it is your legal right. Insurance companies often hope you’ll overlook this part of your claim, but leaving that money on the table is a costly mistake. We’ll show you how to calculate your car’s loss and present a rock-solid case. Follow this guide to confidently manage your GEICO diminished value claim and secure the full compensation you deserve.

Quick Answer: Can You File a GEICO Diminished Value Claim in Georgia?

Yes. Georgia drivers can file a GEICO diminished value claim when an accident leaves their repaired vehicle worth less than it was before the crash. The strongest claims include completed repair records, proof of pre-accident value, comparable market data, and an independent appraisal that shows the remaining loss.

If GEICO has made a low offer, delayed your claim, or asked for more proof than you know how to provide, call Gastley Law at 770-557-2838 or request a case evaluation. Gastley Law focuses on Georgia diminished value and property damage claims, works on contingency when a case is accepted, and fronts claim costs where appropriate.

Key Takeaways

- Georgia diminished value claims require proof: Even after repairs, your car’s accident history can lower resale value. A GEICO diminished value claim should show the vehicle’s pre-accident value, completed repairs, accident history, and remaining market loss.

- Evidence is your strongest tool: Gather the final repair invoice, photos, police report if available, vehicle history report, pre-accident maintenance records, comparable sales, appraisal, GEICO correspondence, and any offer or valuation documents before you negotiate.

- Low offers should be challenged with data: GEICO may rely on unclear valuation methods or quick-settlement pressure. Ask for the calculation, compare it with your independent appraisal, and respond in writing with market evidence.

- Legal help can make sense when the claim stalls: If GEICO denies the claim, delays, disputes documentation, or makes a low offer, call Gastley Law at 770-557-2838 or request a case evaluation.

What Is a Diminished Value Claim?

Let’s start with the basics. A diminished value claim is your right to seek compensation for the loss in your car’s market value after an accident. Think of it this way: even if your car is repaired to look and drive like new, it now has an accident history. When you decide to sell or trade it in, that history will make it worth less than an identical car that’s never been in a wreck. Most buyers are wary of a vehicle that’s been in a collision, and they’ll expect a steep discount for it.

This drop in value is a real, tangible loss, and it’s not your fault. The at-fault driver’s insurance company, in this case, GEICO, is responsible for making you whole again. That doesn’t just mean paying for the repairs; it means compensating you for the permanent hit your car’s resale value has taken.

Many people don’t even know they can file this type of claim, and insurance companies certainly aren’t in a hurry to volunteer the information. They might pay for the bodywork and paint job, but they often hope you’ll overlook the thousands of dollars your car has lost in market value. Securing that compensation is where having expert legal representation can make all the difference.

How an Accident Impacts Your Car’s Resale Value

The biggest reason an accident hurts your car’s value is the vehicle history report. Services like CarFax and AutoCheck track a car’s history, and any reported accident becomes a permanent part of its record. When a potential buyer sees that red flag, they immediately become hesitant. They might worry about hidden structural damage or wonder if the repairs were done correctly.

Insurance adjusters may argue that if the car was repaired properly, there should be minimal diminished value. While quality repairs are essential, they don’t erase the stigma of an accident. The simple fact that the car was in a collision is enough to drive its price down. A smart buyer will always choose the car without an accident history, forcing you to lower your price to compete. This difference in price is the resale value you’ve lost.

The Different Kinds of Diminished Value

It helps to know that “diminished value” isn’t just one single concept. It’s generally broken down into three categories, though you’ll mainly be focused on one for your claim.

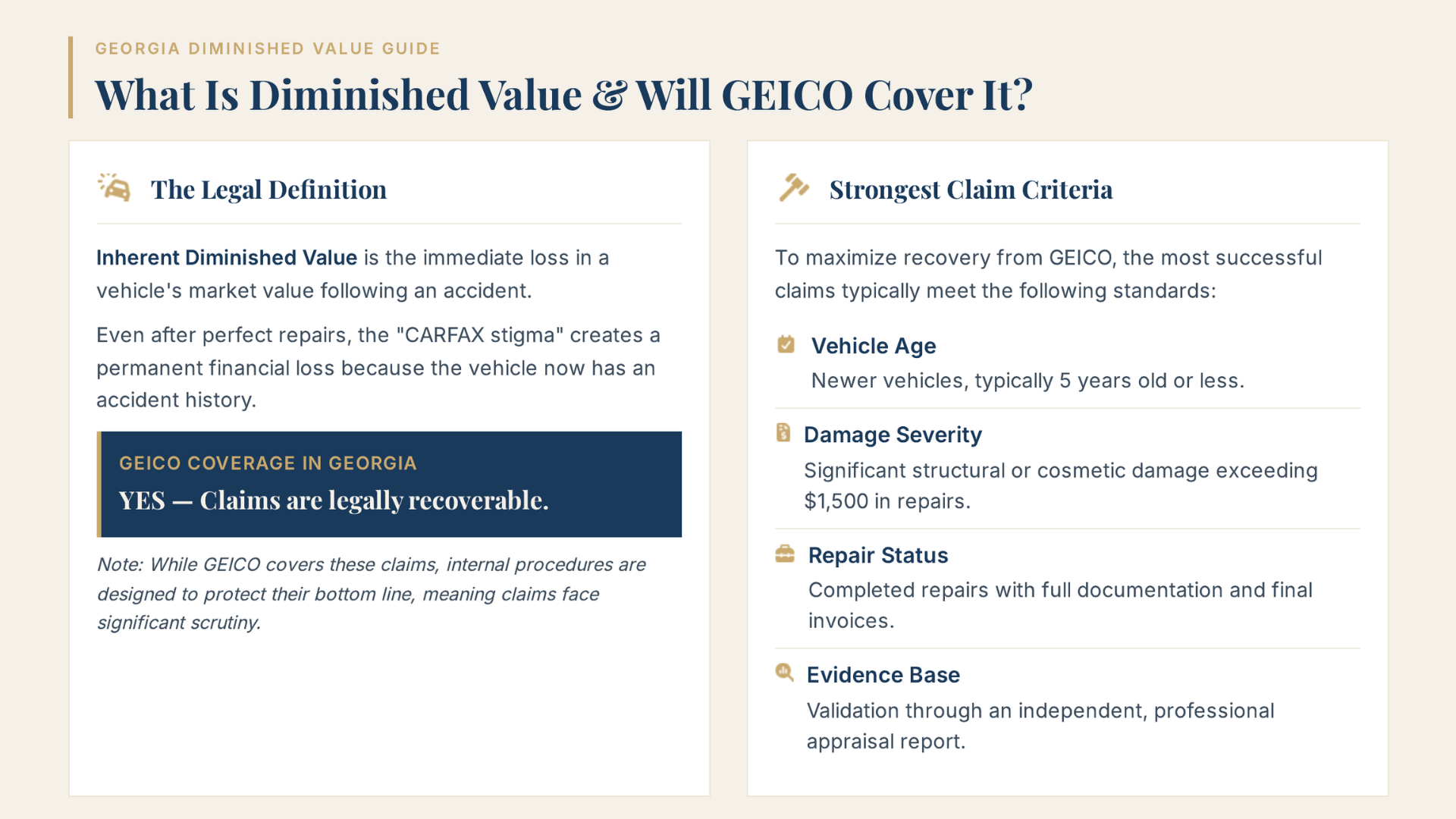

First is Immediate Diminished Value, which is the difference in the car’s value right after the accident and before any repairs are made. More importantly, there’s Inherent Diminished Value. This is the loss that remains even after your car has been fully and perfectly restored. It’s the value lost simply because the vehicle now has an accident history, and this is the basis for most claims.

Finally, there’s Repair-Related Diminished Value, which applies if the repairs were done poorly, using subpar parts or techniques. This results in an additional loss of value on top of the inherent loss. For most GEICO claims, your focus will be on proving and recovering the inherent diminished value.

Will GEICO Cover a Diminished Value Claim?

Let’s get straight to the point: Yes, GEICO does cover diminished value claims in Georgia. That’s the good news. The reality, however, is that getting a fair payment from them, or any insurer, requires a solid strategy. Insurance companies are businesses, and their goal is often to pay out as little as possible. So, while you absolutely have the right to file a claim, you should expect them to offer less than what your car has actually lost in value.

Don’t let this discourage you. It just means you need to be prepared. Successfully filing a diminished value claim with GEICO isn’t about luck; it’s about building a strong, evidence-based case that clearly shows how much your car’s market value has dropped because of the accident. With the right documentation and a clear understanding of the process, you can confidently pursue the full compensation you deserve.

For Georgia claimants, the practical issue is not whether diminished value exists. It is whether you can prove the amount with enough detail to overcome the insurer’s internal valuation. Document when repairs were completed, what the vehicle was worth before the accident, how the accident history affects resale value in the Georgia market, and whether your policy or claim path gives you appraisal-clause options if the value is disputed.

What GEICO’s Policy Says

While GEICO’s official policies acknowledge that they cover diminished value, they don’t exactly advertise it or make the process easy. You won’t find a simple “Click Here to Get Your Diminished Value Check” button on their website. Their internal procedures are designed to protect their bottom line, which means they will scrutinize your claim and look for reasons to pay less.

Think of it this way: they will cover your claim, but they expect you to prove it. The responsibility falls on you to demonstrate that your vehicle is worth less after repairs than it was before the accident. Simply submitting the repair bill isn’t enough. You have to be proactive and present a compelling argument backed by professional appraisals and market data.

When GEICO Is Likely to Pay

GEICO is more likely to take a diminished value claim seriously under specific circumstances. Generally, they are more willing to pay when the vehicle is newer, typically five years old or less, and has sustained significant damage, usually over $1,500 in repair costs. Why? Because the loss in value is much more obvious and substantial on a newer car with major repairs than on an older vehicle with a few dings.

Even if your car fits this description, don’t be surprised if their first offer is disappointingly low. It’s a common tactic. Your best move is to reject the initial offer and counter with your own evidence. If your situation involves a newer car and serious damage, it’s a good sign you have a strong case, but you’ll still need to fight for it. If you feel you’re not being heard, it may be time to get in touch with an expert who can advocate on your behalf.

What to Do Before You File Your Claim

Before you pick up the phone to call GEICO, it’s important to get your ducks in a row. Filing a diminished value claim isn’t just about telling the insurance company your car is worth less; it’s about proving it with clear, undeniable evidence. Georgia claimants should be ready to show repair completion, pre-accident condition, accident history, comparable market loss, and the specific valuation documents GEICO used. Rushing into the process without the right preparation can unfortunately lead to a quick denial or a lowball offer that doesn’t come close to what you’re owed. By taking a few key steps first, you build a much stronger foundation for your claim and show the adjuster you mean business. Let’s walk through exactly what you need to do.

Finish Your Car Repairs First

It might feel counterintuitive, but you must get your car fully repaired before you file for diminished value. GEICO and other insurers simply won’t consider a claim until the vehicle is restored to its post-accident, repaired condition. Think of it this way: the final repair bill is a key piece of evidence. It officially documents the extent of the damages, from structural issues to cosmetic fixes. Without that final invoice, your claim is based on hypotheticals. So, focus on getting the repairs done right by a reputable shop. Once you have that final bill in hand, you have the first official document you need to begin building your case for the value your car has lost.

Collect Your Car’s Pre-Accident Info

To prove your car has lost value, you first need to establish what it was worth right before the accident. This is a step many people miss, but it’s absolutely essential. Your goal is to paint a clear picture of a well-maintained, valuable vehicle. Start gathering documents like maintenance records, receipts for new tires or upgrades, and any pre-accident photos you have. You should also get a vehicle history report to show it was accident-free. This information helps define the car’s pre-loss condition and value, making it much harder for an adjuster to downplay what you’ve lost. The more evidence you have of your car’s excellent condition, the stronger your argument for a higher diminished value settlement will be.

Get a Professional Appraisal

While your own research is helpful, a professional opinion is what gives your claim real weight. You’ll need to hire an independent, certified appraiser to conduct a diminished value appraisal. This isn’t the same as the estimate you got from the body shop. A specialized appraiser will inspect the quality of the repairs and calculate the specific loss in resale value your car has suffered due to its new accident history. This formal report is your most powerful piece of evidence. It provides a documented, expert assessment that substantiates your claim and gives you a concrete number to present to GEICO. Having an expert in your corner is a critical part of our legal services for getting clients what they deserve.

How to File Your Diminished Value Claim with GEICO

Filing a diminished value claim with a major insurer like GEICO can feel like a big undertaking, but it doesn’t have to be. When you break it down into clear, manageable steps, you can approach the process with confidence. The key is to be prepared, organized, and persistent. Think of it as building a case for the compensation you deserve. You’ll need to gather the right evidence, present it clearly, and be ready to stand your ground. Let’s walk through exactly what you need to do to file your claim and get the full value you’re owed.

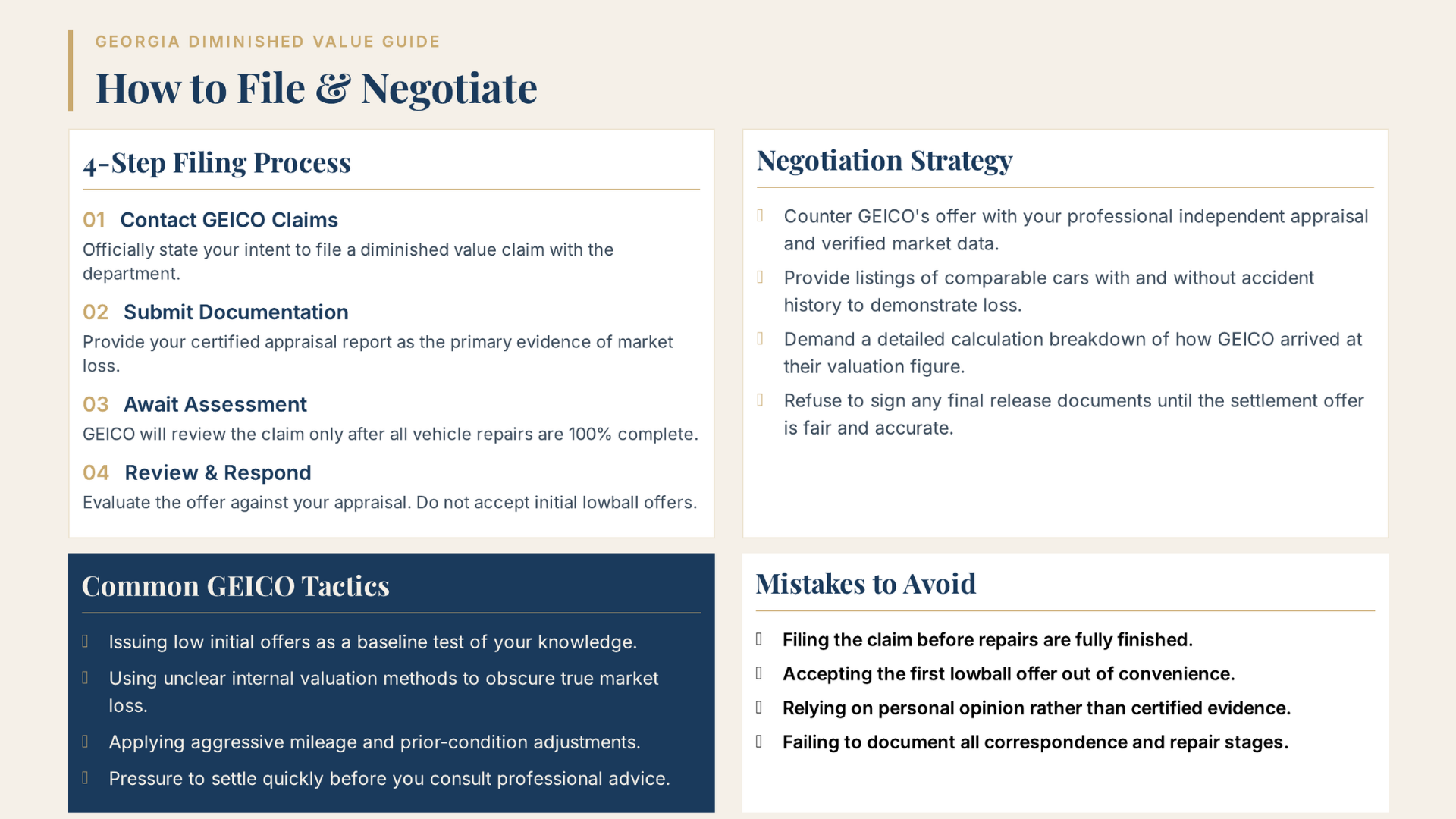

Step 1: Contact the GEICO Claims Department

Your first move is to officially start the process by getting in touch with the GEICO Claims Center. You can do this online or over the phone to report a new claim or follow up on an existing one related to your accident. Before you call, have your policy number and any other relevant information about the accident handy. This will make the initial conversation much smoother. Clearly state that you intend to file a diminished value claim in addition to your property damage claim. This puts them on notice and gets the ball rolling on your specific request.

Step 2: Submit Your Documents

This is where your preparation really pays off. GEICO will need documentation to support your claim, and the most important piece of evidence is a certified diminished value appraisal. This report, prepared by an independent expert, calculates exactly how much resale value your car has lost because of the accident. It’s the foundation of your entire claim. Simply telling GEICO your car is worth less isn’t enough; you need a professional report to prove it. This document is your primary tool for showing them the true financial impact of the damage.

Step 3: Await GEICO’s Assessment

Once you’ve submitted your appraisal and other documents, GEICO will begin its own assessment. It’s important to know that they won’t consider your diminished value claim until your vehicle’s repairs are 100% complete. This is a standard practice, as they need to evaluate the quality of the repairs before determining the remaining loss in value. While waiting can be frustrating, it’s a necessary part of the process. Use this time to make sure you have all your paperwork in order for the next step, which is when the real negotiation begins.

If the dispute is with your own insurer and your policy includes an appraisal clause, that clause may offer a formal path for challenging the valuation. Do not assume it applies to every GEICO claim. Review the policy language, keep all valuation paperwork, and get advice before signing a broad release.

Step 4: Review and Respond to Their Offer

After completing its review, GEICO will present you with a settlement offer. Don’t be surprised or discouraged if it’s much lower than what your appraisal report suggested. Many initial offers are low. Do not accept it right away. You have every right to challenge their figure. This is when you’ll use your evidence, including your professional appraisal and research on what similar, accident-history vehicles are selling for. If you feel overwhelmed or that GEICO isn’t negotiating fairly, this is the perfect time to get in touch with an expert who can fight for you.

Your Essential Document Checklist

When you file a GEICO diminished value claim in Georgia, you are building a proof file. The goal is to show what the vehicle was worth before the accident, what happened during repairs, how the accident history affects resale value, and why GEICO’s number does not fully account for that loss. Use this checklist before you submit a demand or respond to an offer.

- Final repair invoice and estimates: Include the final body-shop invoice, initial estimate, supplements, receipts, and any notes showing structural, frame, paint, or part-replacement work.

- Photos of the damage and repaired vehicle: Save photos from the accident scene, tow yard, repair shop, and post-repair condition so the severity and completed repair status are clear.

- Police report, if available: A crash report can help establish the accident details, parties involved, and facts GEICO may later dispute.

- Vehicle history report: A CarFax, AutoCheck, or similar report can show whether the car had a clean pre-accident history and how the new accident record affects resale value.

- Pre-accident records: Keep maintenance records, service receipts, upgrade receipts, mileage records, and pre-accident photos that support the vehicle’s prior condition.

- Comparable sale listings: Save listings for similar vehicles in Georgia with comparable year, make, model, trim, mileage, and condition. Include examples with and without accident history when possible.

- Independent appraisal: A professional diminished value appraisal gives GEICO a specific, data-backed number instead of leaving valuation entirely to the insurer.

- GEICO correspondence: Keep claim numbers, adjuster emails, letters, call notes, document requests, and any explanations GEICO gives for its valuation.

- Offer and valuation documents: Save every settlement offer, worksheet, formula, inspection note, and valuation report GEICO provides before you counter or sign anything.

This paperwork also helps if you need legal support. Gastley Law handles Georgia diminished value and property damage claims, and the firm can review the offer, documentation, and next steps if GEICO’s valuation does not match the evidence.

GEICO’s Offer Is Too Low. Now What?

It’s a frustrating moment. After going through the entire claims process, you get an offer from GEICO that feels like a slap in the face. It’s far less than what you know your car has lost in value. Don’t panic or accept it just to be done with the process. A low offer is often just the starting point of a negotiation. Insurance companies are businesses, and their initial offer is typically calculated to protect their bottom line, not to give you the full compensation you deserve.

The good news is that you don’t have to take their first offer. You have the right to challenge it, but you need to come prepared. This is where all the documentation you’ve gathered becomes your most powerful tool. By presenting a counteroffer backed by solid evidence, you shift the conversation from their assessment to the actual facts of your car’s lost value. Think of it less as an argument and more as a presentation of the facts. Your goal is to clearly and calmly show them why their number is incorrect and what the right number should be.

Counter Their Offer with Solid Data

When you receive a low offer, your first move is to respond with a counteroffer built on hard evidence. Don’t just say the offer is too low; show them why. The professional appraisal you secured is the cornerstone of your argument. This report, created by an unbiased expert, provides a detailed analysis of your vehicle’s specific diminished value and is much more credible than the formula GEICO likely used.

In your response, formally reject their initial offer in writing. Then, present your counteroffer, citing the valuation from your appraisal report. Attach a copy of the report for their review. This data-driven approach shows you’ve done your homework and are serious about receiving fair compensation. It moves the negotiation onto your terms, forcing them to address your expert’s findings rather than simply repeating their lowball number.

Show Them What Similar Cars Are Selling For

To strengthen your counteroffer, you need to provide real-world market evidence. Your professional appraisal is key, but supplementing it with current market data makes your case even more compelling. Research what cars comparable to yours (same make, model, year, and similar mileage) are selling for in your local area. Look at listings from dealerships and online marketplaces.

Crucially, find examples of similar cars that also have an accident history and compare their prices to those with a clean record. The price difference is a tangible demonstration of diminished value. Take screenshots of these listings and include them with your counteroffer. This proof shows the GEICO adjuster exactly how the accident has impacted your car’s marketability and provides a clear financial basis for your claim.

Negotiate with Confidence (and Proof)

Armed with your professional appraisal and market research, you can negotiate from a position of strength. Remember, the claims adjuster’s job is to settle the claim for the lowest amount possible. Your job is to advocate for the full amount you are owed. When you communicate with GEICO, be polite but firm. Clearly state your position and refer back to the evidence you’ve provided.

If they push back, ask them to provide a detailed breakdown of how they calculated their offer. Often, their methods won’t stand up to the specific, real-world data you’ve presented. Don’t be afraid to go back and forth a few times. However, if you feel like you’re hitting a wall or the process is becoming too stressful, it may be time to get professional help. An experienced attorney can take over the negotiation for you. If you need support, you can always contact us for guidance.

If GEICO will not explain its valuation or the offer still does not match your appraisal, do not sign a final release just to end the claim. Call Gastley Law at 770-557-2838 or request a case evaluation before you give up leverage.

Common GEICO Tactics Georgia Claimants Should Expect

Filing a diminished value claim should be straightforward, but insurance companies do not always make it easy. When dealing with GEICO, Georgia claimants may encounter tactics that reduce, delay, or dispute the payout. Recognizing those tactics helps you respond with documents instead of frustration.

Low Initial Offers

A first offer may be far below the vehicle’s actual market loss. Treat it as a starting point, not the final word. Compare the offer with your appraisal, repair severity, mileage, prior condition, and local comparable sales before responding.

Unclear Valuation Methods

GEICO may provide a number without a clear explanation of the math behind it. Ask for the valuation method, inspection notes, comparable vehicles, deductions, and any formula used. If the explanation is vague, counter with your independent appraisal and market evidence.

Pressure to Settle Quickly

Quick payment can feel helpful after an accident, but a fast settlement may require you to release claims before the diminished value has been fully documented. Review any release carefully and avoid signing away rights before you understand whether the offer accounts for the car’s post-repair loss.

Mileage and Prior-Condition Adjustments

Insurers may reduce a diminished value claim by pointing to mileage, older damage, wear, or prior ownership history. That is why pre-accident maintenance records, photos, and a clean vehicle history report matter. They help separate legitimate deductions from unsupported discounting.

Documentation Disputes

GEICO may ask for more proof, challenge your appraisal, or claim the repair paperwork is not enough. Respond in writing, keep a complete claim file, and provide the strongest documents from the checklist above. If the requests become repetitive or unreasonable, legal help can keep the claim moving.

Avoid These Common Claim-Killing Mistakes

Filing a diminished value claim can feel like walking through a minefield. Insurance companies have a process designed to minimize their payout, and it’s easy to make a misstep that costs you money. By being aware of the most common pitfalls, you can protect your claim and give yourself the best shot at fair compensation. Let’s walk through the mistakes you’ll want to avoid.

Filing Too Soon

It’s tempting to file your claim the second you get your car back from the shop, but moving too quickly can stop your claim before it even starts. GEICO will not accept a diminished value claim until your car is fully repaired. The final repair bill is a critical piece of evidence that shows the extent of the damage. Filing before all the work is complete means you don’t have the full picture of your car’s post-accident condition. Wait until every last dent is fixed and you have the final invoice in hand. This ensures your claim is based on the complete and final state of your vehicle.

Accepting the First Lowball Offer

After you submit your claim, you might get a settlement offer from GEICO surprisingly fast. Be careful. As one legal expert notes, “Geico might offer you money fast to get you to agree to a small amount and give up your right to more.” This initial offer is almost always lower than what you’re actually owed. They are counting on you wanting a quick resolution and accepting the first number they throw out. Don’t fall for it. Always take the time to review their offer carefully and compare it to your own professional appraisal. This is where having legal representation can make a significant difference.

Not Providing Enough Proof

Your opinion that your car has lost value isn’t enough to convince an insurance adjuster. You need to back it up with solid evidence. To successfully file your claim, you need strong proof that your car’s market value has dropped because of the accident. This includes a professional appraisal report, documentation of your car’s pre-accident condition, and examples of what similar cars are selling for. Without compelling evidence, GEICO can easily argue that the diminished value is minimal or nonexistent. The more proof you have, the harder it is for them to deny or lowball your claim.

Forgetting to Document Everything

From the moment the accident happens, you should be in documentation mode. As attorneys often advise, “Keep records: Write down every conversation and keep copies of all documents related to your claim.” This means noting the date, time, and name of every GEICO representative you speak with, along with a summary of your conversation. Save every email and letter you receive. Keep a dedicated folder for all your repair bills, estimates, and appraisal reports. This paper trail is your best defense if disputes arise. If you feel overwhelmed by the process, don’t hesitate to get in touch for help.

Is It Time to Call a Lawyer?

Handling a diminished value claim on your own can feel like an uphill battle, especially when the insurance company isn’t cooperating. While many people successfully file their own claims, there are moments when bringing in a professional is the smartest move you can make. Insurance companies have teams of adjusters and lawyers working to protect their bottom line, so it’s only fair that you have an expert on your side, too. Think of it as leveling the playing field so you can approach the negotiation with confidence.

If you’re feeling stuck, frustrated, or just plain ignored by GEICO, it might be time to consider legal help. An experienced attorney knows the tactics insurance companies use and can step in to manage the process for you. They can cut through the red tape, present your case effectively, and make sure your claim is taken seriously. This isn’t about starting a fight; it’s about ensuring you get the fair compensation you’re entitled to after an accident. A lawyer can take the emotional weight off your shoulders, allowing you to focus on other things while they handle the complex negotiations and paperwork. They are familiar with the specific requirements for a diminished value claim in Georgia and can prevent you from making small mistakes that could jeopardize your case.

Signs You Need Legal Help

You don’t need to wait for a complete denial to seek legal advice. If GEICO is making your claim difficult with constant delays, confusing requests for documents, or offers that are insultingly low, it’s a clear sign you could use support. Another major red flag is if they start blaming you for the accident or suggesting the damage isn’t as bad as the repair bills indicate. These are common strategies used to wear you down. If you feel like you’re being ignored or that your claim is being dismissed with vague excuses, it’s time to contact a professional who can advocate for your rights.

How an Attorney Can Get You More Money

An attorney does more than just send letters on your behalf. They build an evidence-based case to document your car’s loss in value. They understand Georgia’s claim process and know what documentation is typically needed to challenge a low offer. By handling negotiations, a lawyer can shield you from the stress of dealing with adjusters and counter GEICO’s arguments with appraisal data, repair records, and market proof. Gastley Law focuses on Georgia diminished value and property damage claims and works on contingency when a case is accepted. To discuss your next step, call 770-557-2838 or request a case evaluation.

How Long Will This Whole Process Take?

It’s one of the first questions on everyone’s mind: “How long until this is over?” While there’s no single answer that fits every situation, understanding the general timeline and the factors that influence it can help you set realistic expectations. The process isn’t always quick, especially when you’re determined to get the full amount you’re owed. It involves several steps, from finishing your repairs to negotiating with the insurance adjuster, and each stage has its own pace.

What to Expect from the Timeline

The clock on your diminished value claim doesn’t start until your car is completely fixed. GEICO will not accept a claim until all repairs are done, so the first part of your timeline depends on your body shop’s schedule and the extent of the damage. Once you file, GEICO assigns an adjuster to your case. It’s important to remember that this adjuster’s primary goal is to minimize the payout. Their review process can add time as they assess the damage and calculate an offer, which often isn’t in your favor.

What Can Slow Down Your Claim

Several things can stretch out the timeline. GEICO has been known to deny valid claims using vague standards or demanding unreasonable levels of proof, which can cause significant delays while you gather more documents. Another common slowdown happens during negotiations. If GEICO makes a low offer, you’ll need to challenge it by providing your own evidence, like market prices for similar cars. This back-and-forth takes time. Accepting the first offer might seem faster, but fighting for fair compensation is worth the extra effort. If you hit these roadblocks, getting expert legal help can make all the difference in moving your diminished value claim forward.

Related Articles

Comparing carrier tactics can also help. If your accident involves another insurer, review our State Farm diminished value claim guide for a carrier-specific process overview.

- How to Negotiate a Diminished Value Claim: A Guide

- How to Negotiate a Diminished Value Settlement

- Maximize Your Car Accident Diminished Value Settlement

- Diminished Value Claims | Gastley Law

Frequently Asked Questions

Does GEICO pay diminished value claims in Georgia?

GEICO may pay a diminished value claim in Georgia when the evidence shows that a repaired vehicle is worth less because of its accident history. The challenge is proving the amount. Completed repair records, comparable sales, vehicle history, and an independent appraisal can make the claim stronger.

What evidence strengthens a GEICO diminished value claim?

Strong evidence includes the final repair invoice, photos, police report if available, vehicle history report, pre-accident maintenance records, comparable sale listings, a diminished value appraisal, GEICO correspondence, and any offer or valuation documents. Keep everything organized before you counter an offer.

What should I do if GEICO’s diminished value offer is too low?

Do not accept a low offer without reviewing the valuation. Ask GEICO for the calculation, compare it with your appraisal and local market evidence, then respond in writing with a documented counteroffer. Avoid signing a final release until you understand what claims you may be giving up.

When should I call a lawyer for a GEICO diminished value claim?

Consider calling a lawyer if GEICO denies the claim, delays, will not explain the valuation, disputes clear documentation, or pressures you to settle quickly. Gastley Law reviews Georgia diminished value and property damage claims and can be reached at 770-557-2838.

Can I still file a diminished value claim if the accident was my fault?

Fault and policy language matter. Many diminished value claims are made against the at-fault driver’s insurer, but Georgia insurance issues can be fact-specific. If you are unsure who should pay or what coverage applies, get advice before assuming the claim is unavailable.

Is there a time limit for filing a diminished value claim in Georgia?

Georgia property damage claims have time limits, and waiting can make evidence harder to gather. Start organizing the claim after repairs are complete so you have repair records, valuation proof, and correspondence ready well before any deadline becomes an issue.