Filing a Vehicle Damage Claim: A Step-by-Step Guide

Let’s be honest: when you file a vehicle damage claim, you’re not just asking for help. You’re entering a negotiation with a massive company whose primary goal is to pay out as little as possible. Insurance adjusters are trained professionals, and they know all the tactics to minimize your settlement. But you don’t have to be at a disadvantage. Understanding their playbook is the first step to building your own. This guide will walk you through the entire process, showing you where the insurance company might try to cut corners and how you can fight back to get the full compensation you deserve for your property.

Key Takeaways

- Document everything from the start: Your claim’s strength relies on the evidence you gather immediately. Take detailed photos of the damage, secure a copy of the police report, and keep a log of all communications to create a solid record for your case.

- Claim your car’s lost value: A complete settlement includes more than just repair costs. Your car is now worth less due to its accident history, and you are entitled to compensation for this diminished value. You must specifically demand it, as insurers rarely offer it willingly.

- Challenge the first settlement offer: An insurer’s initial offer is almost always a lowball tactic, not their final number. Always be prepared to negotiate by presenting your own evidence, like independent repair estimates, to fight for the full amount you are actually owed.

What Is a Vehicle Damage Claim?

After an accident, the path to getting your car fixed involves a formal process with an insurance company. A vehicle damage claim is simply your official request for the insurer to cover the costs of repairing your car. Whether you’re dealing with your own insurance provider or the at-fault driver’s, this claim kicks off an investigation. The insurance company will evaluate the damage, check the policy details, and decide how much they are willing to pay. This is often where challenges begin, as their initial offer may not cover the full extent of your losses.

When Should You File a Claim?

It’s wise to start your claim as soon as possible after an accident. In Georgia, you generally have four years to file a claim for property damage, but waiting can complicate things. Evidence disappears, memories fade, and delays can give the insurance company reasons to question the severity of the damage. Filing promptly ensures that all the details are fresh and that you can provide a clear, accurate account of what happened. Acting quickly puts you in a stronger position from the start and helps move the repair process along without unnecessary hold-ups.

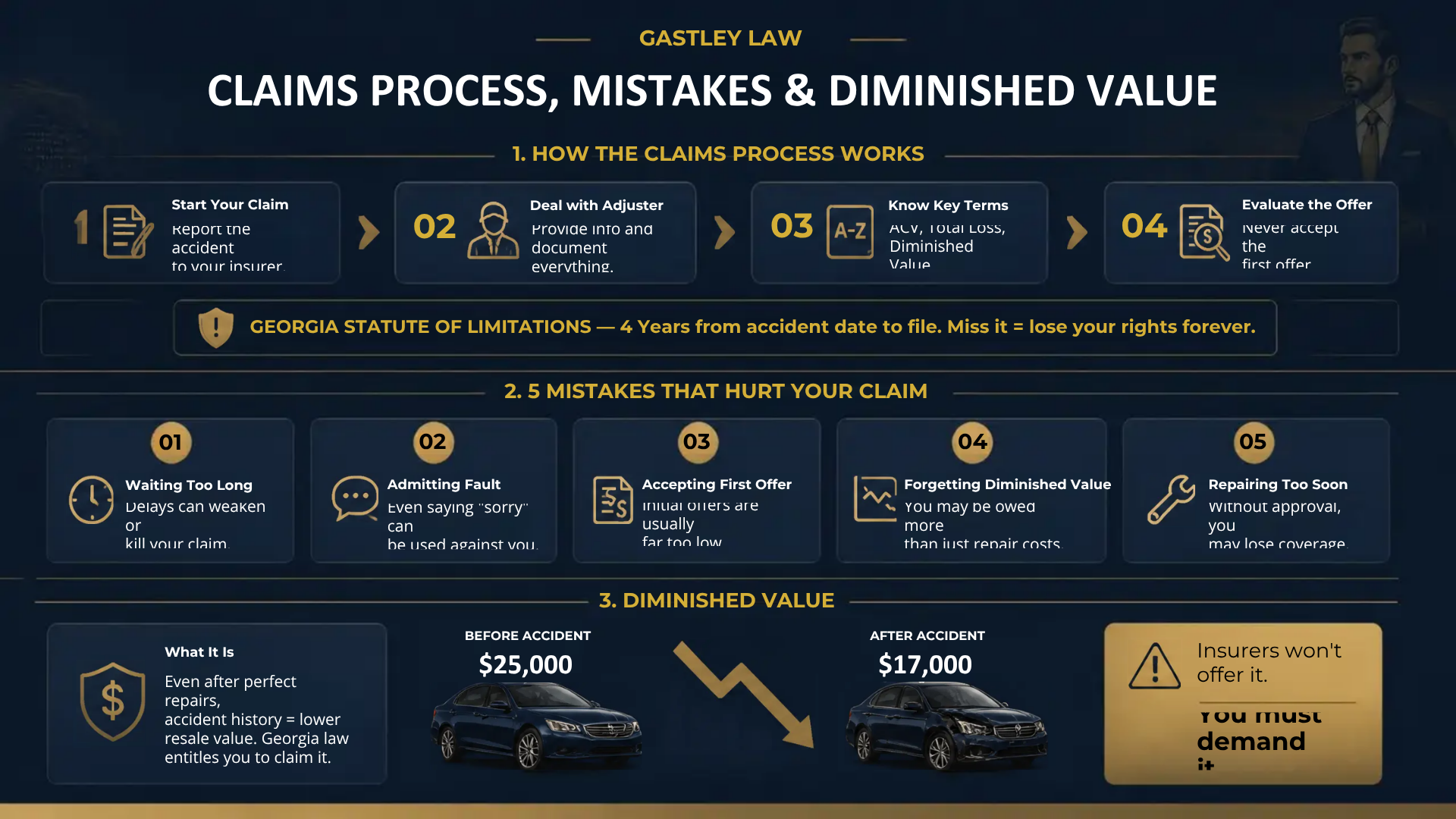

Know Your Rights as a Claimant

As a claimant, you have rights that insurance companies may not advertise. You have the right to have your vehicle repaired to its pre-accident condition, and you can choose the repair shop you trust to do the work. Most importantly, you have the right to be compensated for your car’s loss of value. Even with perfect repairs, a vehicle with an accident on its record is worth less than one without. This loss is called diminished value, and you are entitled to claim it. Understanding these rights is the first step toward ensuring you receive a fair and complete settlement.

Will Filing a Claim Affect My Premiums?

This is a common worry, and the answer depends on who was at fault. If the other driver caused the accident, their insurance is responsible for the damages, and your premiums should not be affected. However, if you were at fault and file a claim with your own insurer, your rates could increase at your next renewal. Don’t let this fear prevent you from seeking the compensation you deserve for major repairs. The cost of fixing your vehicle often far exceeds any potential rate hike. If you’re unsure what to do, we can review your case for free and help you understand the best path forward.

Your First Steps After a Car Accident

Car accidents are jarring, and it’s easy to feel overwhelmed in the moments that follow. Your mind is likely racing, but taking a few specific, intentional steps right at the scene can make a huge difference in protecting your rights and setting up a successful vehicle damage claim. Think of this as your immediate to-do list. By staying calm and focusing on these four actions, you can gather the essential information needed to ensure you’re treated fairly by the insurance companies. These steps help build the foundation for getting the compensation you deserve for your property damage.

1. Prioritize Safety and Call for Help

Before you do anything else, take a deep breath and check on yourself and your passengers. If anyone is injured, call 911 immediately. Your health and safety are the top priority. If your car is in a dangerous spot, like the middle of a busy intersection, move it to the shoulder if you can do so safely. However, if it’s safe to leave the vehicles where they are, it’s best not to move them. The final positions of the cars can be important evidence for the police report and your insurance claim.

2. Document Everything at the Scene

Your phone is your most powerful tool right now. Start taking photos and videos of everything. Get wide shots of the entire scene, including traffic signs, road conditions, and the weather. Then, move closer and capture detailed pictures of the damage to all vehicles involved from every angle. Don’t forget close-ups of broken parts, dents, and scratches. This visual evidence is incredibly powerful and difficult for insurance adjusters to dispute. This documentation is the bedrock of the legal services that ensure you receive full compensation for your damages.

3. Exchange Key Information

If another driver was involved, you’ll need to exchange some key pieces of information. Politely ask for their full name, contact information, insurance company, and policy number. It’s also a great idea to snap a quick photo of their driver’s license, insurance card, and license plate for your records. If there were any witnesses who saw the accident happen, ask for their names and phone numbers. Their objective account can be a huge help if the other driver’s story changes later on.

4. Give Your Insurer a Heads-Up

You should notify your insurance company about the accident as soon as you can. Most policies require you to report an incident promptly, and waiting too long can complicate your claim. You can usually find a 24/7 claims hotline on your insurance card or their website. When you call, stick to the facts of what happened without admitting fault or speculating. Just let them know an accident occurred. While you’re handling these initial calls, it’s also a wise time to contact us for a free case review to understand your rights from the start.

What Paperwork Do You Need to File a Claim?

After an accident, it’s easy to feel overwhelmed by the thought of paperwork. But getting organized from the start is one of the most powerful things you can do to support your claim. Think of it as building a case file. Every document, photo, and note you collect serves as a piece of evidence to show the insurance company exactly what happened and what you’re owed. Having this information ready makes the process smoother and shows the insurer that you mean business. It helps you build a strong foundation for all the steps that follow, from negotiating with an adjuster to fighting for the full value of your repairs.

Photos and Videos

Your phone is your best tool in the moments after an accident. Use it to take as many photos and videos as you can, since this visual evidence is hard for an insurance company to dispute. Capture the scene from multiple angles, getting wide shots of the cars and their positions on the road. Then, move in closer to document the specific damage to every vehicle involved. Take pictures of dents, scratches, shattered glass, and any parts that are broken or leaking fluid. Don’t forget to photograph the surrounding area, including traffic signs, skid marks, and road conditions. This creates a clear, undeniable record of the accident’s aftermath.

The Police Report

If the police responded to your accident, the report they file is a crucial piece of paperwork. This official document provides a neutral, third-party summary of the incident. It typically includes the date, time, and location of the crash, contact and insurance information for all drivers, and statements from witnesses. The officer may also include a diagram of the accident and their initial thoughts on what happened. Insurance adjusters rely heavily on this report when they begin their investigation, so obtaining a copy for your own records is a must. You can usually request it from the responding police department a few days after the accident.

Repair Estimates and Invoices

To get your car fixed, you’ll need to show the insurance company how much it will cost. Don’t just go with the first quote you get or the one from the insurer’s “preferred” shop. Instead, get at least two or three independent repair estimates from body shops you trust. This helps establish a fair and accurate cost for the repairs, giving you leverage if the insurance company tries to offer a lower amount. If you’ve already paid for a tow or any minor repairs, keep every single invoice and receipt. These documents are essential for getting reimbursed for your out-of-pocket expenses as part of your property damage claim.

A Log of All Communications

From your first call to the insurance company, start keeping a detailed log of every conversation. In a notebook or a digital document, write down the date, time, and name of every person you speak with. Summarize what you discussed and note any promises or timelines they give you. Save all emails and letters you receive in a dedicated folder. This communication log creates a clear timeline and holds the adjuster accountable for what they’ve told you. It’s also invaluable if you run into disagreements or delays, as it provides a complete record of your interactions. This simple habit can prevent a lot of “he said, she said” confusion down the road.

How the Vehicle Damage Claim Process Works

Filing a vehicle damage claim can feel like a maze, but understanding the steps can make a huge difference. It’s a process, and knowing what to expect can help you feel more in control. Let’s walk through the typical journey of a claim, from the first call to the final settlement, so you can be prepared every step of the way.

Starting Your Claim

Your first move is to report the accident to the correct insurance company. If the other driver was at fault, you’ll file with their insurer. If you were at fault or the other driver is uninsured, you’ll file with your own. Regardless of who you call, it’s smart to get your own independent repair estimate from a trusted body shop. This gives you a realistic baseline for costs before the insurance company even gets involved. Having your own numbers is the first step in making sure you get a fair deal for the necessary repairs.

Dealing with the Insurance Adjuster

Soon after you file, the insurance company will assign an adjuster to your case. This person’s job is to inspect your vehicle’s damage and write a report on what it will cost to fix it. It’s important to remember that the adjuster works for the insurance company. Their main goal is to close the claim for the lowest possible cost. While they are usually professional, their estimate may not fully cover everything. You can be friendly and cooperative, but always keep in mind that their assessment is just one part of the process, not the final word.

Deductibles, Coverage, and Total Loss Explained

As you go through the process, you’ll hear a few key terms. Your “deductible” is the amount you pay out of pocket before your own insurance coverage kicks in. The insurance company determines your car’s worth using its “Actual Cash Value” (ACV), which is what it was worth right before the accident. If the repair costs are more than the car’s ACV, the insurer will declare it a “total loss.” In that case, they will offer you a settlement check for the ACV. This is also where you need to understand what is diminished value, as your car’s worth has permanently dropped even after perfect repairs.

Evaluating the Settlement Offer

The insurance company will eventually make a settlement offer. Do not feel pressured to accept the first one, especially if it seems low. You have the right to negotiate. If their offer doesn’t cover the repair estimate from your preferred shop, you can push back. Present your own evidence, including your repair estimates, photos of the damage, and any other documentation you have. A strong, well-supported counteroffer shows the insurer you’ve done your homework. If you feel like you’re being ignored or unfairly treated, it might be time to contact us for help.

Georgia’s Deadline: Don’t Miss Your Window to File

This is incredibly important: in Georgia, you have a limited time to act. The statute of limitations for filing a property damage claim is typically four years from the date of the accident. If you miss this deadline, you lose your right to pursue compensation for your vehicle’s damages forever. Insurance companies know this, and delaying can seriously hurt your case. It’s best to start the process as soon as possible after an accident to protect your rights and ensure you have plenty of time to build a strong claim.

Common Mistakes That Can Hurt Your Claim

After a car accident, it’s easy to make a misstep. You’re dealing with stress, potential injuries, and the disruption to your daily life. Unfortunately, insurance companies can use small mistakes to reduce or deny your claim, costing you hundreds or even thousands of dollars. Knowing what to avoid is just as important as knowing what to do.

Navigating the claims process is tricky, but you can protect your right to fair compensation by steering clear of these common pitfalls. From saying the wrong thing at the scene to accepting a bad deal, these errors can significantly impact the outcome of your vehicle damage claim. Let’s walk through the five biggest mistakes we see people make and how you can avoid them.

Waiting Too Long to File

In Georgia, you generally have four years from the date of the accident to file a lawsuit for property damage. While that might sound like a lot of time, waiting is never a good idea. Evidence disappears, witness memories fade, and the details of the incident become less clear over time. The sooner you start the process, the stronger your case will be. Acting quickly shows the insurance company you are serious about your claim. If you’re concerned about deadlines or just want to get the process started on the right foot, it’s wise to contact an attorney to understand your timeline and options.

Admitting Fault

Even if you think the accident was your fault, never admit it at the scene. It’s natural to want to say “I’m sorry,” but those words can be legally interpreted as an admission of guilt. Fault is a complex legal issue that is determined after a full investigation, not on the side of the road. When you speak to the other driver, the police, and insurance representatives, stick to the objective facts of what happened. Let the investigators and legal professionals determine liability. Admitting fault can give the insurance company a reason to deny your claim outright, even if the other driver was also partially responsible.

Taking the First Lowball Offer

Insurance adjusters are trained to settle claims for the lowest amount possible. Their first offer is almost never their best one; it’s a starting point for negotiation. They are counting on you to be tired, stressed, and ready to accept any amount of money just to be done with the process. Don’t fall for it. A quick settlement is often an unfair one. Before you accept any offer or sign any paperwork, you should have it reviewed to ensure it fully covers your repairs, rental car costs, and any other related expenses. Our legal services are designed to help you challenge these low offers and fight for what you truly deserve.

Forgetting About Diminished Value

This is one of the most overlooked parts of a vehicle damage claim. Even if your car is repaired perfectly, its resale value drops simply because it now has an accident history. This loss in market value is called diminished value, and you are entitled to compensation for it. Insurance companies rarely bring this up or offer to pay for it on their own. You have to demand it. Understanding what diminished value is and how to prove it is critical to getting the full amount you are owed after an accident. Don’t leave this money on the table.

Repairing Your Car Too Soon

It’s tempting to take your car straight to the shop to get it fixed, but you need to pause. Your insurance company (and the other driver’s) has the right to inspect the damage before any repairs begin. If you fix the car too soon, you destroy the evidence of the damage. The adjuster might dispute the extent of the necessary repairs or even deny coverage because they couldn’t perform their own assessment. Always notify your insurer, let them inspect the vehicle, and get their approval before authorizing a body shop to start work. This simple step prevents major headaches down the road.

How Gastley Law Helps You Get What You’re Owed

Navigating a vehicle damage claim on your own can feel like an uphill battle, especially when you’re already dealing with the stress of an accident. Insurance companies have teams of people working to protect their bottom line, but you don’t have to face them alone. Having an experienced attorney on your side ensures your rights are protected and that you’re fighting for every dollar you deserve. At Gastley Law, we specialize in property damage and diminished value claims, and we know exactly how to counter the insurance company’s tactics. We handle the legal fight so you can focus on getting back to your life.

Challenging Lowball Offers and Denials

It’s a frustratingly common scenario: you submit your claim, and the insurance company comes back with an offer that barely covers your repairs, or worse, denies your claim entirely. When you’re faced with a lowball offer, it’s essential to negotiate effectively. This means gathering your own evidence, like independent repair estimates and detailed photos, to build a stronger case. We take this burden off your shoulders. We meticulously review the insurer’s assessment, identify where they’ve undervalued your claim, and present a powerful counter-argument backed by evidence. Our goal is to make sure you have the funds for proper, quality repairs, not just the cheapest fix the insurer wants to pay for.

Uncovering Your Right to Diminished Value

Even after your car is perfectly repaired, its market value takes a hit. This loss in resale value is called diminished value, and in Georgia, you are entitled to be compensated for it. Insurance adjusters often conveniently forget to mention this or will tell you it doesn’t apply. An experienced Atlanta diminished value attorney can help document that loss and pursue the compensation you may be entitled to recover. You are typically entitled to compensation for more than just the immediate repairs; this includes costs like towing and a rental car. We help our clients understand and prove their right to this compensation. We perform a detailed analysis to calculate the exact amount of value your vehicle has lost and demand that the insurance company pays what you are rightfully owed.

Let’s Review Your Case for Free

You might be wondering if you even have a case or if it’s worth pursuing. The good news is that you don’t have to figure that out by yourself. Seeking assistance from a legal expert can provide valuable guidance and clarity on your options. We believe everyone deserves to know their rights without any financial risk. That’s why we offer a completely free, no-obligation case evaluation. We’ll listen to what happened, look over your documents, and give you an honest assessment of your claim’s potential. If you’re ready to stop feeling overwhelmed by the claims process, contact us for a free case review and let’s talk about how we can help you.

Related Articles

- Georgia Diminished Value Requirements Explained

- Diminished Value Claims in Georgia | Gastley Law

- What Is Vehicle Diminished Value? A GA Guide

- Maximize Your Car Accident Diminished Value Settlement

Frequently Asked Questions

Do I have to use the repair shop my insurance company recommends?

No, you do not. In Georgia, you have the right to choose which body shop repairs your vehicle. Insurance companies often have “preferred” shops because they have agreements for faster or cheaper work, but that doesn’t always mean it’s the best work. Choosing a shop you trust ensures the repairs are done to your standards, not just the insurer’s budget.

What if the other driver was uninsured or it was a hit-and-run?

This is a stressful situation, but you still have options. If you have uninsured or underinsured motorist (UM/UIM) coverage on your own policy, you can file a claim through that. If you don’t have UM coverage, you can use your collision coverage, if you have it, to pay for the repairs. The process can be a bit more complicated, which is why getting advice on your specific policy is a good first step.

Is a diminished value claim separate from my repair claim?

Think of them as two parts of the same whole. Your property damage claim covers all your losses, which includes both the cost of repairs and the loss of market value (diminished value) your car suffers after those repairs are complete. Insurance companies will gladly pay for repairs (though they may argue about the cost), but they rarely offer to pay for diminished value unless you specifically demand it and prove your loss.

The accident was my fault. Can I still get compensation for my car’s damage?

Yes, if you have collision coverage on your auto insurance policy. This coverage is designed to pay for repairs to your own vehicle, regardless of who caused the accident. You will have to pay your deductible, and filing an at-fault claim could cause your insurance rates to go up at renewal. However, for significant damage, using your coverage is often the only way to get your car back on the road without paying for everything yourself.

How much does it cost to hire an attorney for a property damage claim?

You should never have to pay money just to find out if you have a good case. That’s why we offer a free case review to discuss your situation and explain your options without any pressure or obligation. If you decide to hire us, we typically handle these cases on a contingency fee basis. This means we only get paid if we successfully recover money for you, so you don’t have to worry about any upfront costs.