Total Loss Settlement: A Step-by-Step Guide

When an insurance company tells you your car is a total loss, they are starting a negotiation, not ending a conversation. Their first offer is just that: a starting point. Unfortunately, it’s often a lowball figure that won’t be enough to get you back on the road in a comparable vehicle. They have a team of professionals working to protect their bottom line, so why shouldn’t you have a plan to protect yours? This article will equip you with the knowledge you need to confidently handle your total loss settlement, from understanding how they value your car to gathering the evidence needed to challenge their offer and fight for more.

Key Takeaways

- Treat the first offer as a starting point: An insurer’s initial settlement is based on their calculation of your car’s Actual Cash Value (ACV), but it’s a number you can and should negotiate, not a final decision.

- Build your case with solid evidence: To successfully argue for a higher amount, you need proof. Gather maintenance records, receipts for recent upgrades, and local listings for comparable cars to show the adjuster your vehicle’s true market worth.

- Don’t hesitate to get professional help: Georgia law protects your right to a fair settlement, including taxes and fees. If an insurer uses delay tactics or refuses to negotiate in good faith, an attorney can step in to manage the process and protect your interests.

What Is a Total Loss Settlement?

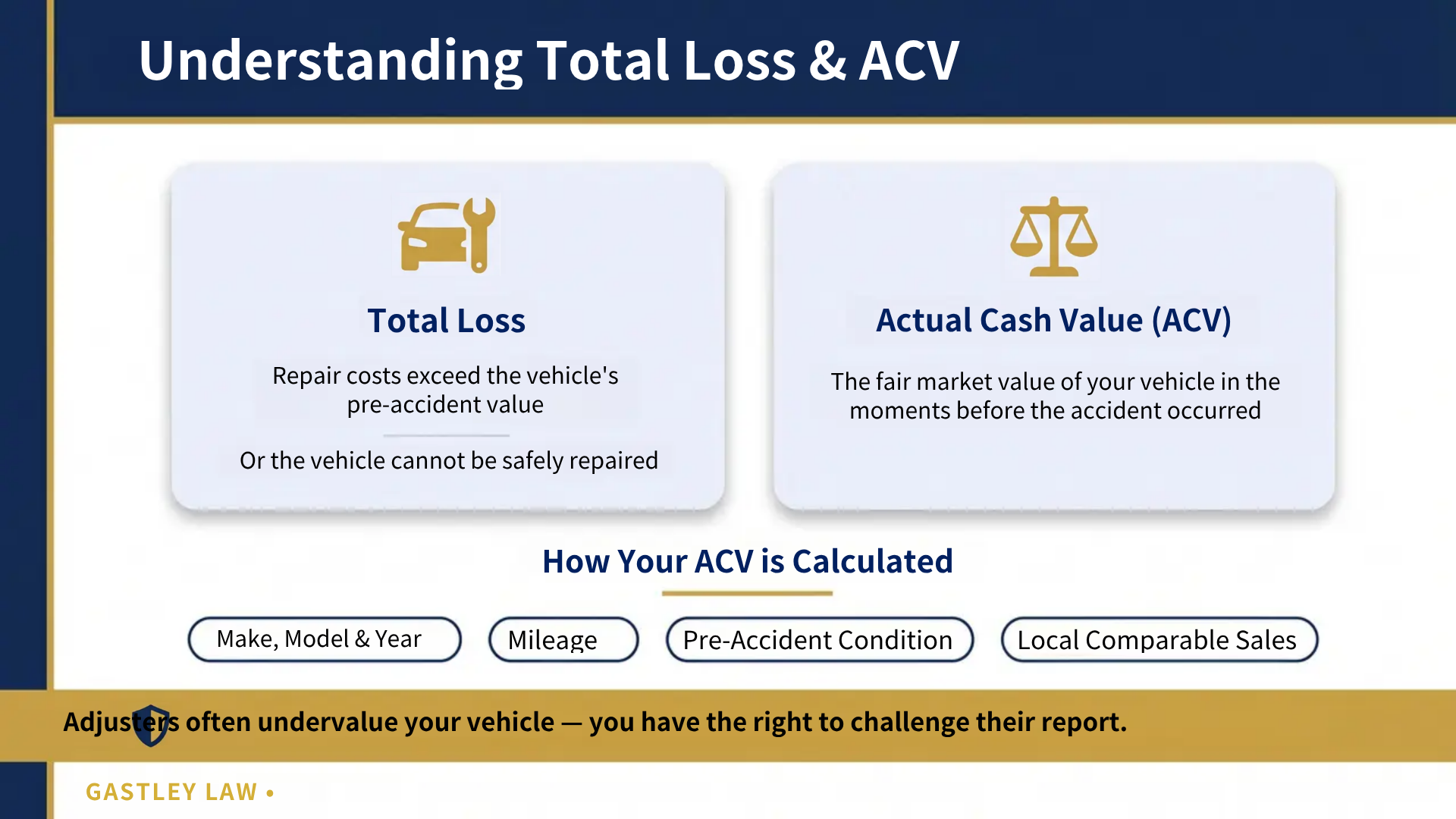

After a serious car accident, hearing the insurance company declare your car a “total loss” can feel like another blow. But what does that term actually mean for you and your wallet? A total loss settlement is the payment an insurance company provides when your vehicle is damaged so badly that the cost of repairs is more than its value right before the accident. Instead of cutting a check for repairs, the insurer pays you the car’s pre-accident market value, which is also known as its Actual Cash Value (ACV). This value is meant to reflect what your car was worth just moments before the crash, taking into account its make, model, year, mileage, and overall condition.

Once you accept the settlement, the insurance company typically takes ownership of your damaged car. The process might sound straightforward, but it’s often where challenges begin. The insurer’s calculation of your car’s value is a critical point of negotiation. They might use valuation reports that pull from sources that undervalue your vehicle, leaving you with a settlement that isn’t enough to buy a comparable replacement. This is why understanding the process is so important. If you believe the offer is too low, you have the right to challenge it. Getting fair compensation is essential, and our firm specializes in handling these types of property damage claims to ensure you get what you’re owed.

What Makes a Car a “Total Loss”?

An insurance company will consider your car a “total loss” for a few key reasons. The most common one is when the estimated cost to fix the vehicle exceeds its Actual Cash Value. It’s a simple cost-benefit analysis for the insurer. They also declare a car totaled if it can’t be repaired safely, meaning it would still be dangerous to drive even after being fixed. Finally, each state has its own regulations. Your car could be deemed a total loss if the damage meets the specific threshold set by Georgia law, which determines when the cost of repairs is officially too high.

Total Loss vs. Repairable Damage: What’s the Difference?

The line between repairable damage and a total loss isn’t always about whether the car can be fixed. It’s about whether it’s financially practical to do so. A car is declared a total loss when the repair costs are higher than a certain percentage of its pre-accident value, a rule known as the total loss threshold. For example, if a car is worth $10,000 and the state’s threshold is 75%, it will be totaled if repairs cost $7,500 or more. If you’re facing this situation and have questions about your vehicle’s valuation, don’t hesitate to contact us for guidance.

How Do Insurance Companies Calculate Your Settlement?

After an accident, the insurance company doesn’t just pick a number out of thin air. They use a specific formula to decide what your car was worth right before the crash. Their goal is to pay out the lowest amount possible, so understanding their process is the first step toward making sure you get a fair deal. The entire settlement is built around one key concept: your car’s Actual Cash Value.

Understanding “Actual Cash Value” (ACV)

If your car is declared a total loss, the insurance company is required to pay you its “Actual Cash Value,” or ACV. This isn’t what you paid for the car or what a new one would cost. ACV is the market value of your vehicle the moment before the accident happened. Think of it as the price a willing buyer would have paid for your car in its pre-accident condition. This calculation considers its age, mileage, and overall wear and tear. It’s similar to the concept of diminished value, which is the loss in a car’s market value after it has been in an accident and repaired.

Finding Your Car’s True Market Value

To determine the ACV, the adjuster will look at several factors. They’ll pull data on your car’s mileage, features, and any special add-ons you had. They also look for any damage the car had before the accident, like old dents or scratches. The most important piece of their puzzle is the selling price of similar cars in your local area. They will find a few “comparable” vehicles that recently sold and use those prices to justify their offer. This is often where disagreements start, as the vehicles they choose might not be a fair match for yours. You can get a head start by researching your car’s value on a site like Kelley Blue Book.

How Depreciation and Prior Damage Affect Your Offer

Insurance companies will always deduct for depreciation, which is the natural loss of value your car experiences over time. An older car with high mileage will be worth less than a newer one, and that will be reflected in the offer. The adjuster will also carefully inspect your vehicle’s history and condition report. Any pre-existing, unrepaired damage will be noted and subtracted from the settlement amount. It’s crucial to review their valuation report carefully to ensure these deductions are fair and accurate. If you feel the insurer is undervaluing your claim, our team can step in to handle the negotiations and fight for what you’re owed. You can learn more about our services and how we help clients with property damage claims.

Your Next Steps After a Total Loss Declaration

Hearing that your car is a “total loss” can feel like a gut punch. It’s a stressful situation, but knowing what to do next can give you a sense of control. Think of this as your action plan. By taking these steps, you can make sure the process goes as smoothly as possible and protect your right to fair compensation for your property damage claim. Let’s walk through what you need to do, one step at a time.

Gather Your Paperwork

Before you can move forward, you need to get your documents in order. Having everything ready makes your conversations with the insurance adjuster much more efficient. Collect any notes from the accident scene, the police report, photos of the damage, and the other driver’s information. You’ll also need your car’s title, which proves you own it. If you’re still paying off a loan or leasing the vehicle, find the contact information for your finance company, as they will need to be involved.

Clear Out Your Car and Address Your Loan

This is a simple but important step: remove all personal belongings from your car. Check the glove box, trunk, and under the seats. Once the insurance company takes the vehicle, it can be difficult to get your things back. Next, consider your car loan. If you own the car outright, the insurance company sends the settlement check to you. However, if you have an outstanding loan, the insurer is required to pay your lender first. Any remaining amount will then be paid to you.

Start Your Claim and the Settlement Process

To get the ball rolling, you need to officially file a claim with your insurance provider or the at-fault driver’s insurer. The company will assign an adjuster to inspect your vehicle and confirm the damage. While they will take their own photos, you should take plenty of pictures and videos for your records. The adjuster will then determine your car’s Actual Cash Value (ACV) to calculate a settlement offer. They often use resources like Kelley Blue Book and local sales listings to find this value.

How Long Does a Total Loss Settlement Take?

After your car is declared a total loss, one of the first questions you’ll have is, “How long will this take?” It’s a completely valid question. You need a check to buy a new car and get your life back to normal. The honest answer is: it depends. The total loss settlement process can take anywhere from a few days to several weeks, or even longer. The timeline really hinges on the complexity of your accident and how your insurance company handles the claim.

A straightforward case, where liability is clear and the paperwork is in order, will naturally move faster. But when things get complicated, like when there are serious injuries or disputes over who was at fault, the process slows down. Insurance companies also have their own internal procedures that can add time. They need to inspect the vehicle, review your policy, and calculate the car’s value before making an offer. While everyone wants a quick resolution, it’s more important to get a fair one. Rushing the process could mean accepting a lowball offer that doesn’t cover what you truly lost. If you feel the insurance company is dragging its feet or not giving your claim the attention it deserves, it might be time to seek legal representation.

A Typical Settlement Timeline

In a best-case scenario, the settlement process can be relatively quick. For a simple claim, you might be looking at a timeline of about a week and a half from start to finish. Typically, the insurance company will schedule an inspection within a day or two of you filing the claim. After the inspection, it usually takes them about three business days to finalize the settlement offer. Once you agree to the terms and sign the paperwork, you can often expect to receive payment within another business day. Keep in mind, this is an ideal timeline. Any hiccup along the way can add days or even weeks to the process.

Why Your Settlement Might Be Delayed

Unfortunately, delays are common in total loss claims. If your accident was particularly severe, the insurance company might need more time to investigate and review your policy, which can push the timeline past 30 days. Sometimes, these claims can take 10 weeks or more to resolve. The biggest reason for a delay is often a disagreement over your car’s value. If you believe the insurer’s offer is too low, you have the right to challenge it by providing maintenance records or proof of recent upgrades. This back-and-forth negotiation takes time. If you’re stuck in a lengthy dispute, don’t hesitate to contact us for help.

Don’t Like the Offer? Here’s What to Do

Getting a lowball offer from the insurance company can feel defeating, but it’s important to remember that their first number is rarely their final one. You don’t have to accept an offer that you feel is unfair. With the right approach and solid evidence, you can push back and negotiate for the compensation you truly deserve. It’s all about knowing your options and being prepared to make your case. Challenging the insurer’s valuation is a critical step toward getting the full amount you’re owed for your vehicle.

How to Challenge the Insurer’s Valuation

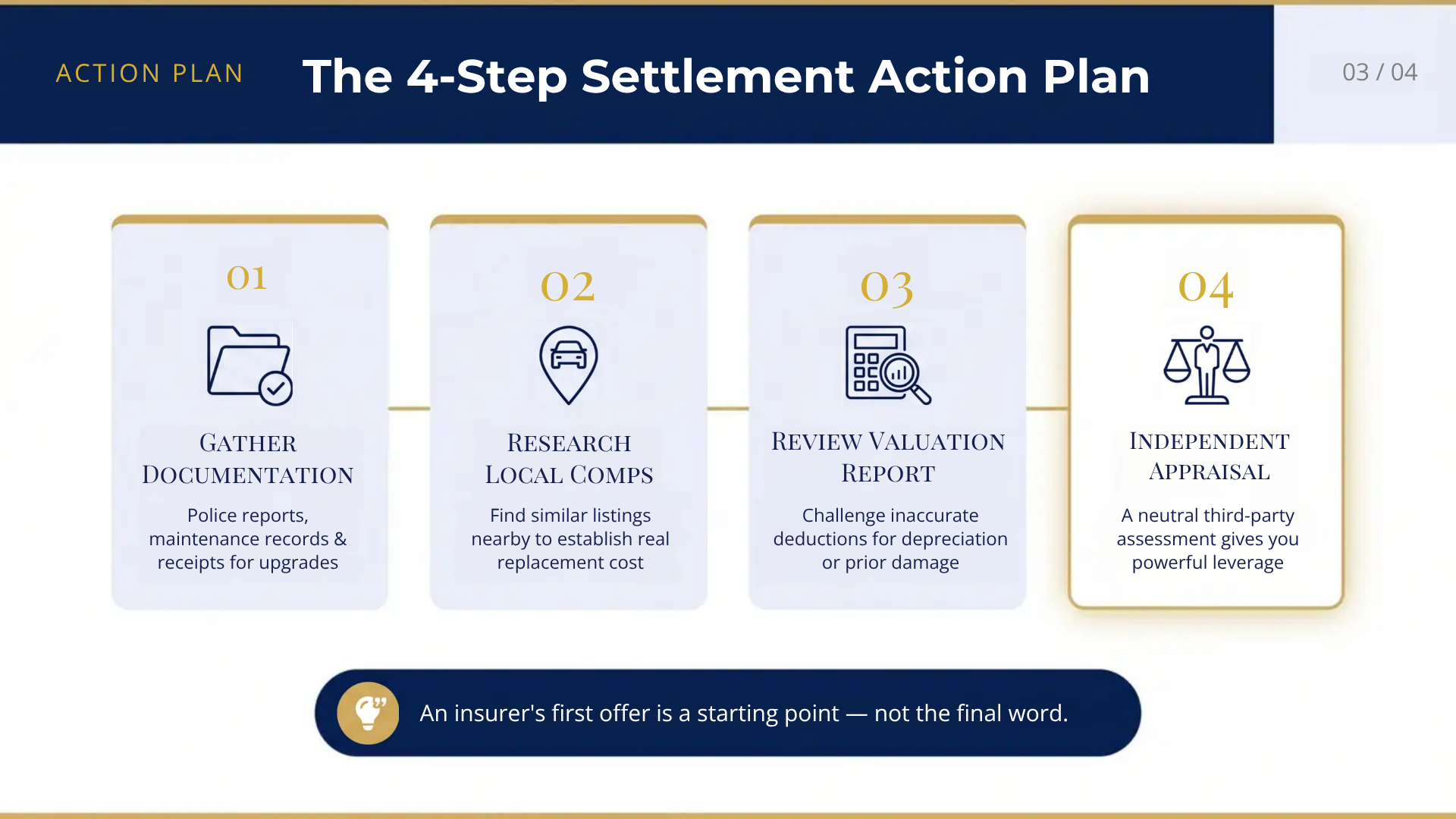

Your first step is to ask the insurance adjuster to walk you through their math. How exactly did they arrive at their offer? Request a copy of their valuation report so you can see the sources they used, like Kelley Blue Book, and the comparable vehicles they referenced. If you think their assessment is off, you can counter it. Gather documents that prove your car’s excellent condition, such as detailed maintenance records, receipts for recent repairs or new tires, or proof of any aftermarket upgrades you’ve made. This information can compel the insurer to re-evaluate your claim and, hopefully, adjust their offer in your favor.

Get an Independent Appraisal

If you and the insurer are miles apart on the car’s value, it might be time to bring in a neutral third party. Hiring a professional appraiser can provide an unbiased, expert opinion on what your car was worth right before the accident. This isn’t just your opinion versus theirs; it’s a documented assessment from a qualified professional that carries significant weight. An independent appraisal serves as powerful leverage in negotiations and shows the insurance company you’re serious about getting a fair settlement. Our team at Gastley Law frequently works with trusted appraisers as part of our property damage claim services.

Use Evidence to Argue for a Higher Value

A strong argument is built on strong evidence. Go online and find several listings for vehicles that are the same make, model, year, and trim as yours, with similar mileage and in similar condition. Use local dealership and private seller listings to show the true market cost to replace your car in your area. Present these “comps” to the adjuster. This shifts the conversation from their theoretical value to the real-world cost you’re facing. Understanding your car’s pre-accident value is also crucial when pursuing a diminished value claim for a repaired vehicle, as it establishes the baseline from which the value has dropped.

Common (and Costly) Settlement Mistakes to Avoid

Going through a total loss settlement can feel overwhelming, and it’s easy to make a misstep when you’re under pressure. Insurance companies are focused on their bottom line, not yours. Knowing what to watch out for can make a huge difference in your final payout. Let’s walk through a few common mistakes that can cost you money and how you can steer clear of them.

Accepting the First Offer Too Quickly

When the insurance adjuster calls with an offer, your first instinct might be relief. But it’s smart to pause before saying yes. The first offer is almost always a lowball figure designed to close your case quickly and cheaply. Remember, this is a negotiation. You have the right to push back and ask for a settlement that reflects your car’s true market value. Take time to research what similar cars are selling for in your area. Understanding your vehicle’s diminished value and actual worth is your best tool for getting the compensation you deserve. Don’t let the insurer rush you into a decision you’ll regret.

Forgetting Key Documents

A strong claim is built on solid evidence. Before you even speak with an adjuster, get your paperwork in order. This includes the police report, photos of the accident scene and vehicle damage, and any repair estimates you’ve received. Don’t forget maintenance records, which can prove your car was well-cared-for and worth more than the insurer’s initial estimate. Having these documents ready shows the insurance company you’re serious and prepared. It helps streamline the process and provides the proof you need to argue for a fair settlement. If you’re feeling overwhelmed, our team can help you gather and organize the necessary evidence as part of our services.

Ignoring Salvage Title Rules

If your car is declared a total loss, you might have the option to keep it and take a lower settlement. If you go this route, your car will be issued a “salvage title.” This permanently brands the vehicle as having been totaled, which can make it difficult to insure and significantly lowers its resale value. Every state has specific rules for salvage titles, including what repairs are needed before it can be legally driven again. Before you decide to keep your car, make sure you understand Georgia’s laws and the long-term financial implications. If you have questions about how this works, don’t hesitate to contact us for guidance.

Know Your Legal Rights in Georgia

When your car is declared a total loss, it can feel like the insurance company holds all the cards. But Georgia law provides specific protections for vehicle owners to ensure you’re treated fairly. Understanding these rights is the first step toward getting the settlement you deserve. It’s not just about what the insurance company offers; it’s about what you are legally owed. Knowing the rules empowers you to challenge a low offer and advocate for yourself effectively.

Your Rights Under Georgia Insurance Law

Under Georgia law, if your car is a total loss, the insurance company has two main obligations: replace your vehicle with a comparable one or pay you its “actual cash value” (ACV). This isn’t just the sticker price; the ACV payment must be enough to buy a similar vehicle in your local market. Crucially, this amount should also cover all applicable taxes, title, and transfer fees. You shouldn’t have to pay these costs out of pocket. The goal of the law is to make you whole again, and that includes covering the necessary administrative costs. Understanding the full scope of your claim is key to ensuring you receive a fair settlement.

What You Still Owe After an Accident

It’s important to know that the insurer’s payment for taxes and fees is tied to the value of your totaled vehicle, not necessarily the new car you buy. If you replace your totaled sedan with a more expensive SUV, the insurer is only required to cover the taxes and fees that would have applied to a vehicle of similar value to your old one. The insurance company can either provide a replacement vehicle or pay you the amount it would have cost them to do so. This distinction matters because it sets a clear limit on the insurer’s financial responsibility for your replacement choice.

What to Do If the Insurer Acts in Bad Faith

Insurance companies are legally required to handle your claim fairly. When they don’t, it’s known as “bad faith.” This can look like intentionally offering a settlement far below your car’s value, refusing to explain their valuation, or creating unreasonable delays. If you feel the adjuster is pressuring you, ignoring your evidence, or not being straight with you, don’t just accept it. These are red flags that they may not be honoring their legal obligations. If you suspect bad faith, it’s time to get professional legal advice. You can contact our team to have an expert evaluate your situation and protect your rights.

Common Roadblocks in the Settlement Process

Getting a fair settlement for your totaled car should be straightforward, but it rarely is. Insurance companies have a process designed to protect their bottom line, which can leave you feeling confused and shortchanged. Knowing what to expect can make a huge difference. You might run into confusing financial situations with your car loan, get lost in a sea of insurance jargon, or just feel completely overwhelmed by the stress of it all. Let’s walk through some of the most common hurdles you might face and how you can prepare to handle them.

Dealing with Car Loans and GAP Coverage

If your car is declared a total loss and you still have a loan, things can get complicated. The insurance company won’t write you a check directly. Instead, they will pay your lender first. The problem is that the settlement amount, or the car’s actual cash value, might be less than what you still owe on your loan. If that happens, you are responsible for paying off the remaining balance out of your own pocket, even though you no longer have the car.

This is where GAP (Guaranteed Asset Protection) insurance becomes so important. GAP coverage is designed to pay the difference between the insurance payout and your remaining loan balance. If you don’t have it, you could be stuck making payments on a car that’s already in a salvage yard. Navigating these financial details is a critical part of handling property damage claims.

Making Sense of Insurance Jargon

Insurance policies and settlement offers are filled with technical terms that can feel like another language. The most important one to understand is “Actual Cash Value” or ACV. This is what the insurance company decides your car was worth the second before the accident. It is not the same as what you paid for it or what you see similar cars listed for online. Insurers use their own formulas to calculate ACV, which often results in a lowball offer.

You don’t have to accept their first number. You have the right to negotiate and ask the adjuster to show you exactly how they arrived at their valuation. Understanding the true diminished value of your vehicle and how ACV is calculated gives you the power to push back effectively.

Handling the Stress of a Total Loss

Dealing with a totaled car is incredibly stressful. You’re suddenly without transportation, facing a mountain of paperwork, and trying to communicate with an insurance adjuster who may not have your best interests at heart. The entire process can take a month or even longer, adding to the anxiety. It’s easy to feel pressured into accepting a bad offer just to get it over with.

To manage the stress, focus on what you can control. Keep detailed records of everything, from the accident report to every conversation with the insurer. Gather proof of your car’s value, like maintenance records or receipts for new tires and upgrades. This evidence can help you argue for a higher settlement. If you feel overwhelmed, remember you don’t have to go through this alone. Sometimes, the best way to reduce stress is to have an expert step in and help.

How to Negotiate a Better Settlement

Receiving a settlement offer from the insurance company is a major step, but it’s not the final one. It’s important to remember that the first offer is just that: a starting point. Insurance companies often offer less than your car is truly worth, but you have the right to negotiate for a fair amount. With the right preparation and a clear strategy, you can confidently counter a lowball offer and work toward a settlement that truly covers your loss.

Do Your Homework on Your Car’s Value

Before you can negotiate, you need to know what your car was actually worth right before the accident. Don’t just take the insurer’s word for it. Start by doing your own research using online tools like Kelley Blue Book and Edmunds to get a clear picture of your car’s market value. Be sure to input accurate details about its make, model, year, mileage, and overall condition. Understanding the true value of your vehicle, including its potential diminished value after an accident, is the foundation of a strong negotiation. This knowledge gives you the data you need to challenge an inadequate offer.

Build Your Case with Solid Evidence

A strong argument needs strong proof. To get a higher payout, you need to collect evidence that supports your car’s value. This is your chance to show the adjuster anything that made your car worth more than a standard model. Gather documents like detailed maintenance records, receipts for recent repairs or new tires, and proof of any upgrades you made, such as a new stereo system or custom wheels. This documentation demonstrates that your car was well-maintained and may have been in better-than-average condition, justifying a higher settlement. Providing this proof makes it much harder for the insurance company to stick to its initial low valuation.

How to Talk to the Insurance Adjuster

When you speak with the insurance adjuster, your goal is to be firm, professional, and prepared. Keep your emotions in check and focus on the facts you’ve gathered. Start by asking the adjuster to provide a detailed breakdown of how they calculated their offer. This forces them to justify their numbers and may reveal areas where their valuation is weak. Present your own research and evidence calmly and clearly. If you feel overwhelmed or believe the insurer isn’t negotiating in good faith, it might be time to get help. You can always contact a lawyer to handle the negotiations for you.

Why a Lawyer Can Help You Get More

Going up against an insurance company can feel like an unfair fight. They have teams of adjusters and lawyers whose main job is to protect the company’s bottom line, which often means paying you as little as possible. While you can handle a total loss claim on your own, having an experienced attorney in your corner levels the playing field. We understand the tactics insurers use and know how to counter them effectively.

Our role is to take the stress off your shoulders and manage the entire process for you. From the moment you hire us, we handle the paperwork, the phone calls, and the tough negotiations. We know what your car is truly worth and what you’re entitled to under Georgia law, including compensation for diminished value. Instead of you having to become an expert overnight, you can rely on our experience to build a strong case and fight for the full and fair settlement you deserve. Think of us as your dedicated advocate, ensuring your rights are protected every step of the way.

We Evaluate Your Case and Gather Evidence

The foundation of a successful claim is solid evidence. When you work with us, one of the first things we do is conduct a thorough case evaluation. We dig into the details of your car’s history to prove its true value before the accident. This means gathering all the necessary documentation, like maintenance records, receipts for recent repairs, and proof of any upgrades you’ve made. This evidence helps us build a powerful argument that counters the insurer’s low initial valuation and demonstrates what your vehicle was actually worth.

We Aggressively Negotiate With Insurers

Insurance adjusters are trained negotiators, and their first offer is almost never their best one. We know this, so we never advise a client to accept it. Our team takes over all communication and aggressively negotiates on your behalf. We present the evidence we’ve gathered and make a clear, data-backed case for a higher payout. If the insurance company still won’t offer a fair value, we can bring in an independent appraiser to provide an unbiased estimate. We handle the back-and-forth so you don’t have to, pushing back until we secure a settlement that truly reflects your loss.

We Protect Your Rights Every Step of the Way

It’s easy to feel powerless when an insurance company gives you a lowball offer, but you have the right to push back for a fair amount. We’re here to make sure your voice is heard and your rights are protected. We understand the complexities of Georgia’s insurance laws and can identify when an insurer is not treating you fairly. Having a lawyer sends a clear message that you are serious about your claim. If you’re ready to get help, contact us for a consultation to discuss your case.

Related Articles

- Car Accident Settlement Negotiations in Georgia

- What to Do If You Don’t Agree With a Total Loss Adjuster

- How to Negotiate a Higher Total Loss Settlement Online

Frequently Asked Questions

What if I owe more on my car loan than the insurance company is offering?

This is a tough situation, and it happens more often than you’d think. If the settlement offer (your car’s Actual Cash Value) is less than your remaining loan balance, you are responsible for paying the difference. This is where GAP insurance can be a lifesaver, as it’s designed to cover that exact “gap.” If you don’t have GAP coverage, you will need to work out a payment plan with your lender to settle the remaining debt, even though you no longer have the car.

Can I keep my car even if it’s declared a total loss?

In most cases, yes, you have the option to keep your vehicle. This is often called “owner retention.” If you choose this path, the insurance company will pay you the settlement amount minus the car’s salvage value (what they would have gotten for it at auction). However, your car will be issued a salvage title, which can make it difficult to insure and significantly reduces its future resale value. You’ll also need to handle the necessary repairs to make it roadworthy again.

Does recent work, like new tires or repairs, increase my car’s settlement value?

Absolutely. If you recently invested in your car, that can increase its pre-accident value. Be sure to gather receipts for any significant work done shortly before the crash, such as new tires, a new battery, or major mechanical repairs. Presenting this documentation to the adjuster provides concrete proof that your car was in excellent condition and worth more than their initial valuation might suggest.

How long do I have to accept or reject a settlement offer?

There isn’t a strict, universal deadline, but insurance companies definitely want to close claims as quickly as possible. It’s important not to let them rush you into a decision. You have a right to take a reasonable amount of time to review their offer, do your own research on your car’s value, and gather evidence to support a counteroffer. Don’t feel pressured to give an immediate answer on the phone; it’s perfectly fine to ask for the offer in writing and tell them you will get back to them.

When is the right time to contact a lawyer about my total loss claim?

You should consider contacting a lawyer if you feel the insurance company isn’t treating you fairly. Good indicators include receiving an offer that is obviously far too low, if the adjuster is unresponsive or using delay tactics, or if you simply feel overwhelmed and pressured by the process. An attorney can step in to handle all negotiations and ensure your rights are protected, especially if the insurer seems unwilling to negotiate in good faith.