How to Reopen an Insurance Claim: A 5-Step Guide

Your car is finally in the shop, and you think the worst is over. Then you get the call from your mechanic. They’ve found more damage, hidden deep beneath the surface, that the initial adjuster missed entirely. Suddenly, that settlement check from the insurance company doesn’t look like it will cover the costs. This scenario is incredibly common, and it’s a perfect reason to reopen an insurance claim. Don’t pay for these unexpected repairs out of your own pocket. This guide explains how to present new evidence to your insurer and fight for the additional funds you need.

Key Takeaways

- A “Closed” Claim Isn’t Always Final: Understand that you can often reopen a property damage claim unless you signed a final release form. New evidence, like hidden damage discovered by your mechanic or an unaddressed diminished value loss, gives you a valid reason to request more compensation.

- Build Your Case with Timely Evidence: Your power comes from your proof. Act quickly to gather essential documents like updated repair invoices, photos of the new damage, and expert appraisals. This organized evidence makes your request to reopen the claim much harder for an insurer to ignore.

- Follow a Clear Plan for Escalation: Start by submitting a formal written request with your new proof. If the insurer denies your request or is unresponsive, don’t give up. Be prepared to escalate the issue to a supervisor or consult with an attorney to fight for the full amount you are owed.

Can You Reopen a Closed Insurance Claim?

After an accident, getting that final check from the insurance company can feel like the end of a long, stressful chapter. But what happens when you realize the settlement wasn’t enough? Maybe your mechanic found more damage, or the repairs cost more than expected. You might be wondering if it’s too late to do anything about it. The good news is that “closed” doesn’t always mean locked forever. In many situations, you can reopen a property damage claim to get the full compensation you deserve.

It’s a common misconception that once an insurance company closes your file, the case is permanently finished. While insurers would certainly like you to believe that, it’s not always true. Understanding the difference between a closed claim and a truly finalized one, and knowing when you have grounds to ask for more, are the first steps toward getting what you’re owed.

Closed vs. Reopened: What’s the Difference?

The key difference often comes down to one piece of paper: a release form. If you signed a “release of all claims” document, you’ve legally agreed that the settlement is final and you won’t pursue any more money for that incident. Reopening a claim after signing a release is very difficult. However, if you simply cashed a check for the initial repairs and never signed a final release, your claim is likely just considered administratively closed by the insurer. This leaves the door open for you to submit new evidence and request additional payment for newly discovered issues or costs.

When Is It Possible to Reopen a Claim?

You can’t reopen a claim just because you changed your mind, but you absolutely can if new facts come to light. For example, if your mechanic discovers hidden frame damage after starting repairs based on the initial, superficial estimate, that’s a valid reason. You can also reopen a claim if you find out the insurance company made a mistake in their assessment or if you realize your settlement didn’t include compensation for your car’s diminished value. If you have new information that proves the original settlement was incomplete or inaccurate, you have a strong case for reopening your claim.

Good Reasons to Reopen Your Insurance Claim

Just because your insurance claim is marked “closed” doesn’t always mean it’s the end of the road. It’s a frustrating feeling to think you’ve put an accident behind you, only to find out the settlement didn’t truly cover your losses. The good news is that you might have a valid reason to revisit the claim. Insurance companies are businesses, and their goal is often to close claims as quickly and inexpensively as possible. They might hope you’ll accept their first offer and move on without asking questions, leaving money on the table that is rightfully yours.

But if new information comes to light or you realize the outcome wasn’t fair, you have rights. Understanding when you can push back is the first step toward getting the compensation you actually deserve. Whether it’s hidden damage that your mechanic just found or the slow realization that the check they sent won’t cover the final bill, these situations are more common than you think. You are your own best advocate, and being informed gives you the power to challenge an inadequate settlement. Let’s walk through some of the most common and legitimate reasons why you might need to reopen your property damage claim.

Discovering New or Hidden Vehicle Damage

It’s very common for the full extent of accident damage to be invisible at first glance. A mechanic might start repairs and find a bent frame, complex electrical issues, or other problems that weren’t included in the initial inspection. If you settle a claim and then discover additional damage that wasn’t seen before, you can and should request more compensation to cover these new losses. An insurer’s initial estimate is based only on what they can see, not the hidden problems that often appear once a vehicle is taken apart. Our firm provides specialized legal representation to handle these exact situations and ensure nothing is overlooked.

Facing Repair Costs Higher Than the Original Estimate

Did the check from your insurance company fail to cover the final repair bill? This happens all the time. The initial payment from an insurer is often just an estimate, and the actual cost of parts and labor can end up being much higher. You are not obligated to pay the difference out of your own pocket. If the first payment was too low to cover the full cost of restoring your vehicle to its pre-accident condition, you have a strong case for reopening your claim. Keep every invoice and receipt from the repair shop, as this documentation is crucial for proving the shortfall to the insurance company.

Finding Errors or Mistakes in the Initial Claim

Paperwork is complicated, and mistakes happen. Sometimes, a claim can be reopened if you find a significant error in the settlement agreement you signed. This could be something as simple as a typo in your vehicle’s VIN or policy number, or it could be a more serious misrepresentation of the facts of the accident. If you can prove there was a factual or clerical error that influenced the settlement amount, you may be able to challenge the agreement. It’s always a good idea to have a professional review these documents, because a small mistake can have a big financial impact on your final payout.

Realizing Your Settlement Offer Was Too Low

Many people accept the first offer from an insurance company because they want to resolve the issue quickly. However, cashing that check doesn’t always mean your claim is permanently closed. If you later realize the payment wasn’t nearly enough to cover your losses, you can still fight for more. Insurers are known for making lowball offers, banking on the hope that you won’t push back. If you feel you were pressured into an unfair settlement or didn’t understand the full scope of your damages at the time, it’s worth challenging the amount. If you believe you were short-changed, don’t hesitate to contact us for a case evaluation.

Pursuing Unclaimed Diminished Value

Even after your car is perfectly repaired, its resale value has likely dropped simply because it now has an accident history. This loss in market value is called diminished value, and you are entitled to compensation for it. Most insurance companies won’t volunteer to pay for this and often leave it out of the initial settlement entirely. If your original claim didn’t include a payment for this loss, you have a very compelling reason to reopen it. Understanding what diminished value is and how to prove it is key to getting the full amount you are legally owed after an accident.

Are There Time Limits for Reopening a Claim?

Yes, time is a critical factor when you’re thinking about reopening an insurance claim. You’re working against two different clocks: the legal deadline set by the state and the specific deadlines written into your insurance policy. Missing either one can unfortunately close the door on getting the money you deserve.

It’s easy to feel overwhelmed by these timelines, especially when you’re already dealing with the stress of a car accident and repairs. But understanding these deadlines is the first step to taking back control. Think of it this way: knowing the rules of the game gives you a much better chance of winning. Let’s break down exactly what these time limits are and why moving quickly is your best strategy.

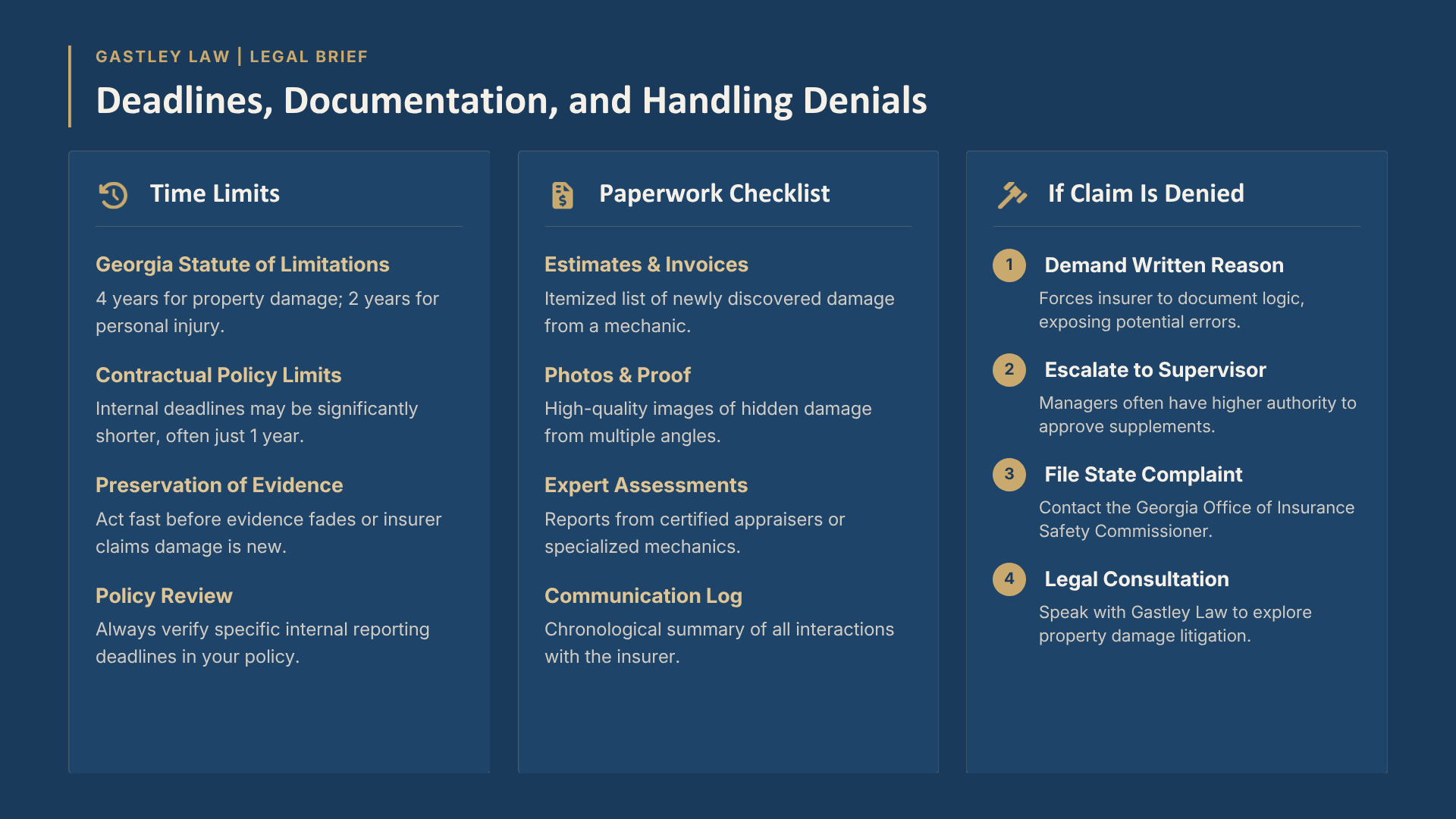

Understanding Georgia’s Statute of Limitations

In Georgia, a “statute of limitations” is a law that sets the maximum amount of time you have to file a lawsuit after an incident. For property damage to your vehicle, you generally have four years from the date of the accident to take legal action. If you were also injured, the timeline for a personal injury claim is shorter, typically two years.

These deadlines are set by the Georgia Code and act as a final cutoff. While you’ll likely resolve your reopened claim directly with the insurer, knowing this legal backstop is important. It’s your ultimate leverage if the insurance company refuses to cooperate. Keeping these dates in mind ensures you preserve your right to pursue full compensation through the legal system if necessary.

Checking the Deadlines in Your Insurance Policy

Separate from the state’s legal deadline, your insurance policy has its own set of rules. Your policy is a contract, and it almost certainly contains clauses that detail the time limit for reopening a claim. This period is often much shorter than the statute of limitations, sometimes as little as one year after the claim was initially closed.

Pull out your policy documents and look for sections on “claims,” “reopening claims,” or “policy conditions.” It can feel like searching for a needle in a haystack, but this step is crucial. If you can’t find it, don’t hesitate to ask your insurance agent or a representative to point you to the exact clause. Understanding your insurance policy is essential, as these contractual deadlines are binding.

Why Acting Quickly Is Key

The moment you discover new damage or realize your settlement was too low, the clock starts ticking. Acting with urgency is vital for a few key reasons. First, evidence doesn’t last forever. Fresh photos of hidden damage, recent mechanic invoices, and clear memories of conversations carry more weight than old, questionable information. Waiting too long can make it harder to prove your case.

Second, prompt action shows the insurance company you are serious and organized. Delays can lead to complications in the claims process, and insurers may argue that new damage could have occurred after the original incident if too much time has passed. By gathering your documents and contacting your adjuster right away, you present a stronger, more credible request that is much harder for them to dismiss.

What Paperwork Do You Need to Reopen a Claim?

Think of reopening your claim like building a case for a project you believe in. You wouldn’t show up to a meeting empty-handed, and the same goes for dealing with your insurer. The more organized and thorough your paperwork is, the harder it will be for them to ignore your request. Having the right documents ready not only strengthens your position but also shows the insurance company that you mean business. It transforms your request from a simple question into a well-supported demand. Let’s walk through exactly what you’ll need to gather to present a compelling argument for reopening your claim.

This preparation is a key part of the legal services we provide, as solid evidence is the backbone of any successful claim. Insurance companies handle thousands of claims, and they often move quickly to close files. Your job is to give them a reason to pause and take a second look. By compiling a neat, professional, and evidence-backed package, you make it easy for the adjuster to understand your position and justify their decision to approve additional funds. Before you even pick up the phone, make sure you have these documents in hand. It will make the entire process smoother and significantly increase your chances of a positive outcome.

Updated Repair Estimates and Invoices

If your mechanic discovered more issues once they started working, those new costs are the foundation of your request. Your first step is to get an updated, itemized estimate from the repair shop. This document should clearly outline the newly discovered damage and the associated costs. Make sure you also have all the invoices and receipts for any work that has already been completed. As one law firm puts it, you need to “collect everything that proves why your claim should be reopened, like repair costs or new damage reports.” This paper trail proves why the initial settlement wasn’t enough to cover the full extent of the repairs.

Photos and Proof of New or Hidden Damage

A picture is worth a thousand words, especially to an insurance adjuster. Go back to your car and take clear, well-lit photos of any new or hidden damage that wasn’t included in the original claim. If you have photos from right after the accident, pull those out too. As one person on Reddit wisely noted, original photos “can help show exactly what the damage was at the time.” Comparing the initial damage with what was discovered later creates a powerful visual timeline that’s hard to dispute. Make sure your new photos are high-quality and clearly show the problem areas from multiple angles.

Expert Assessments and Appraisals

Sometimes, the damage is more than just cosmetic; it affects your car’s value. An expert assessment from a certified mechanic or a specialized appraiser can be your strongest piece of evidence. Ask them for a formal, written report that details the hidden structural damage and explains why it wasn’t caught during the first inspection. This is also where you can address what diminished value is and get an appraisal to prove your car is now worth less, even after repairs. This kind of documentation shows the insurer that you have a professional backing your claim for more compensation.

A Record of All Communication With Your Insurer

Your history with the insurer is part of your story. Create a simple log of every phone call, email, and letter you’ve exchanged with the insurance company. Note the date, time, the name of the person you spoke with, and a quick summary of the conversation. This record demonstrates your efforts to resolve the issue and prevents the insurer from claiming they were never informed. When you’re ready to make the call to reopen, you’ll have a clear timeline of events to reference. If you decide you need help, you can contact us and share this log so we can get up to speed quickly.

Your Step-by-Step Guide to Reopening an Insurance Claim

Feeling like your insurance settlement didn’t quite cover everything can be incredibly frustrating. You went through the whole process, only to realize the check they sent won’t actually fix your car, or you’ve found new problems the adjuster missed. The good news is that a closed claim isn’t always the end of the story. In many cases, you can reopen a claim, especially if you have new information to present. It takes some organization and persistence, but it’s often worth the effort. Following a clear process can make all the difference when you’re dealing with a resistant insurance company. Think of it as building a new case, one that’s stronger and more detailed than your first. You’re not just asking for more money; you’re proving why you’re entitled to it. This guide will give you an actionable plan to follow, from gathering your evidence to making your formal request. We’ll cover how to approach your insurer, what to say, and how to document everything properly. Let’s walk through the exact steps you can take to challenge their initial decision and fight for the full compensation you deserve.

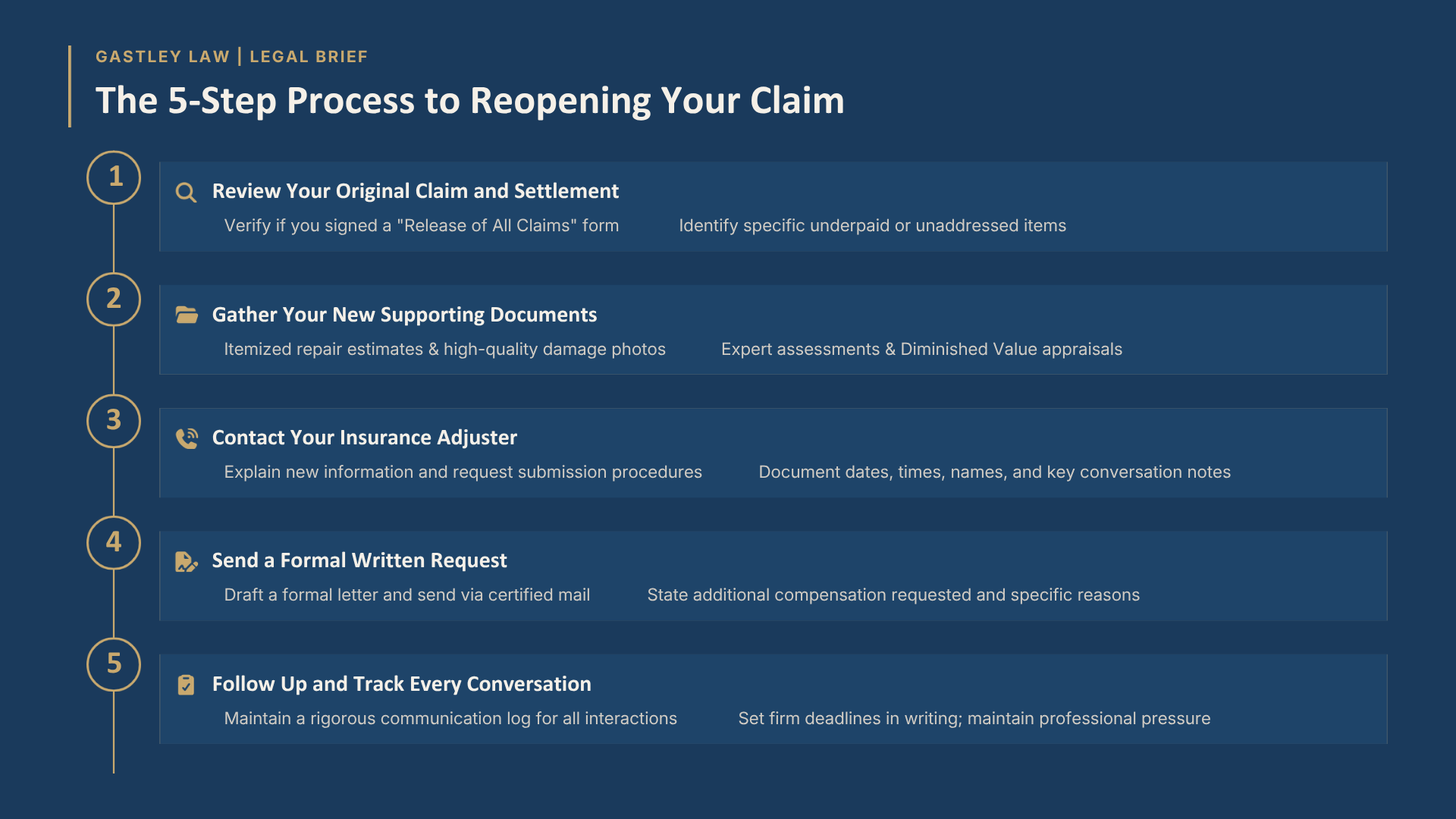

Step 1: Review Your Original Claim and Settlement

Before you do anything else, start by going back to the beginning. Pull out all the documents related to your original claim, including the police report, your policy, photos, repair estimates, and the final settlement agreement or release you signed. Carefully read through everything to understand exactly what was covered and what wasn’t. Did the settlement only cover specific repairs? Did you sign a release that waived your right to future claims? Understanding the details of your initial agreement helps you build a strong foundation for your request by identifying exactly where the original settlement fell short. This initial review is your first and most important piece of homework.

Step 2: Gather Your New Supporting Documents

Now it’s time to build your case. Your goal is to collect new, compelling evidence that proves the original settlement was insufficient. This isn’t about resubmitting old paperwork; it’s about presenting fresh information that justifies a second look. This could include updated repair estimates from a body shop that are higher than the first one, photos of hidden damage discovered during repairs, or a formal report from a mechanic. It might also include an expert appraisal showing your car’s loss of value, which is a key part of a diminished value claim. The more specific and well-documented your new evidence is, the harder it will be for the insurance company to ignore.

Step 3: Contact Your Insurance Adjuster

With your new documents organized, your next move is to get in touch with the insurance company. Start by contacting the same adjuster who handled your original claim, if possible. You can begin with a phone call to explain that you have new information and would like to reopen your claim. Stay calm, polite, and professional. Clearly state that you have new evidence to submit and ask about the specific process for doing so. Be prepared for them to be hesitant, but your goal here is simply to get the ball rolling and find out their official procedure. Take notes during the call, and get the name and title of the person you speak with.

Step 4: Send a Formal Written Request

A phone call is a good first touch, but you absolutely need to follow it up with a formal letter sent via certified mail. This creates a paper trail and shows the insurer you are serious. In your letter, clearly state that you are requesting to reopen your claim. Briefly explain why, referencing the new evidence you’ve gathered. Include copies (never the originals) of all your new supporting documents. End the letter by stating what you expect, whether it’s a specific additional payment or a full reassessment of the damages. Keep your letter concise, professional, and focused on the facts you have documented.

Step 5: Follow Up and Track Every Conversation

After you send your request, the waiting game begins, but you can’t afford to be passive. Keep a detailed log of every interaction you have with the insurance company. Write down the date, time, the name of the person you spoke with, and a summary of the conversation. If the insurer is slow to respond, follow up with polite but firm phone calls and emails. If you start getting the runaround or feel like they aren’t taking your request seriously, it might be time to consider getting professional help. An experienced attorney can handle the communication and show the insurer you mean business. If you’re hitting a wall, you can always contact us for a free case evaluation.

You’ve Submitted Your Request. Now What?

You’ve gathered your documents, written your request, and sent it off. Now comes the part that can feel the most difficult: waiting. While you can’t control the insurance company’s timeline, you can prepare for what comes next. Understanding their process will help you stay in control and know when to follow up. Let’s walk through what you can generally expect during this phase. The key is to remain patient but persistent as the insurance company reviews the new information you’ve provided.

What the Insurance Company Does Next

Once your request is received, an adjuster will review it along with the new evidence you provided. Their first step is to decide if your new information is compelling enough to reconsider the claim. If they see merit in your request, they will likely contact you for additional documentation or clarification. However, if they decide not to reopen the case, they should provide you with a reason for their denial. This is why having strong, clear evidence is so important; it makes it much harder for them to justify saying no. Your goal is to present a case for your property damage claims that is too convincing to ignore.

How Long the Process Might Take

Unfortunately, there isn’t a standard waiting period. The time it takes for an insurer to respond can range from a few days to several weeks, depending on the complexity of your new evidence and their internal procedures. Your specific insurance policy might even outline timelines for these kinds of reviews, so it’s worth checking the fine print again. This uncertainty is exactly why acting quickly is so crucial from the start. The sooner you submit your request, the sooner you can get a resolution, especially when you’re trying to recover the full diminished value of your vehicle after an accident.

What to Do If the Insurance Company Says No

Hearing “no” from the insurance company after you’ve presented new evidence can be incredibly frustrating. It might feel like you’ve hit a dead end, but don’t give up just yet. An initial denial isn’t always the final word, and you have several options for pushing back to get the compensation you deserve. Taking a strategic, step-by-step approach shows the insurer you’re serious about your claim. If they still refuse to cooperate, you can escalate the issue to higher authorities or bring in a legal professional to advocate on your behalf. Remember, you have rights in this process, and the first denial is often a test to see if you’ll simply walk away.

Ask for a Written Explanation of the Denial

If your request to reopen a claim is denied over the phone, your first move should be to ask for that denial in writing. A verbal “no” is informal and leaves no paper trail. A written explanation forces the insurance company to state its official reason for the denial, which is a crucial piece of documentation for your records. This letter can expose weak reasoning or show if the insurer is acting unfairly. If their explanation seems vague or doesn’t align with your policy, you have a solid starting point for an appeal. This document is the first piece of evidence you’ll need if you decide to escalate the issue.

Escalate Your Request to a Supervisor

The claims adjuster you’ve been dealing with doesn’t always have the final say. If they deny your request, politely ask to speak with their supervisor or a claims manager. Escalating your request can often connect you with someone who has more authority to review and approve claims. A supervisor may have a different perspective or more flexibility to reconsider the new evidence you’ve provided. When you speak with them, calmly and clearly restate your case, present your new documentation, and explain why you believe the claim should be reopened. Sometimes, simply moving up the chain of command is enough to get a different, more favorable outcome.

File a Complaint With the Georgia Insurance Commissioner

If you believe your insurance company is acting in bad faith or not following the law, you have the right to file a formal complaint. In Georgia, you can submit your case to the Office of Insurance and Safety Fire Commissioner. This government body oversees insurance companies and investigates consumer complaints. Filing a complaint can trigger an official investigation into the insurer’s practices and put external pressure on them to handle your claim fairly. You can file a complaint online, and it’s a powerful step to take when the insurance company refuses to listen to your valid concerns.

Explore Your Legal Options

When you’ve exhausted all other avenues and the insurance company still won’t budge, it may be time to get professional help. Consulting with an attorney who specializes in property damage and diminished value claims can completely change the game. A lawyer can review your case, your policy, and all communication with the insurer to determine if they are acting improperly. They can handle all further communication and negotiations for you, showing the insurer you are serious about getting what you’re owed. Exploring your legal options is the strongest move you can make when an insurer is unwilling to cooperate.

When Is It Time to Hire a Lawyer?

While you can certainly try to reopen an insurance claim on your own, there are times when bringing in a professional is the smartest move you can make. If you feel like you’re hitting a wall with the insurance company or the process just feels overwhelming, it might be time to get some legal backup. An experienced attorney can step in to manage the complexities of your case and advocate for your best interests, letting you get back to your life. This isn’t about giving up; it’s about gearing up for a real fight.

Signs You Need Professional Legal Help

You should always trust your gut. If your interactions with the insurance company feel off, they probably are. A major red flag is when an insurer acts in “bad faith,” which is a legal term for using unfair tactics to avoid paying what they owe. For example, if your insurance company is making it hard to reopen your claim, it’s a good idea to contact an attorney. Other signs include the adjuster ignoring your calls and emails, refusing to provide a written explanation for a denial, or pressuring you to accept a lowball offer. These aren’t just frustrating inconveniences; they are signals that the insurer may not be treating you fairly.

How a Diminished Value Attorney Strengthens Your Case

An attorney does more than just send strongly worded letters. They build a powerful, evidence-based case on your behalf. If you believe the initial settlement was insufficient to cover your losses, a lawyer can help you reopen the claim to request a higher amount. They understand exactly what diminished value is and how to calculate it accurately, ensuring you don’t leave money on the table. For vehicle owners seeking to reopen a claim, an experienced Atlanta diminished value attorney can also identify losses that may have been overlooked in the original settlement. An experienced attorney knows the arguments and tactics insurance companies use to minimize payouts and can counter them effectively. They will gather the necessary expert appraisals, organize your documentation, and handle all negotiations, strengthening your position and taking the stress off your shoulders.

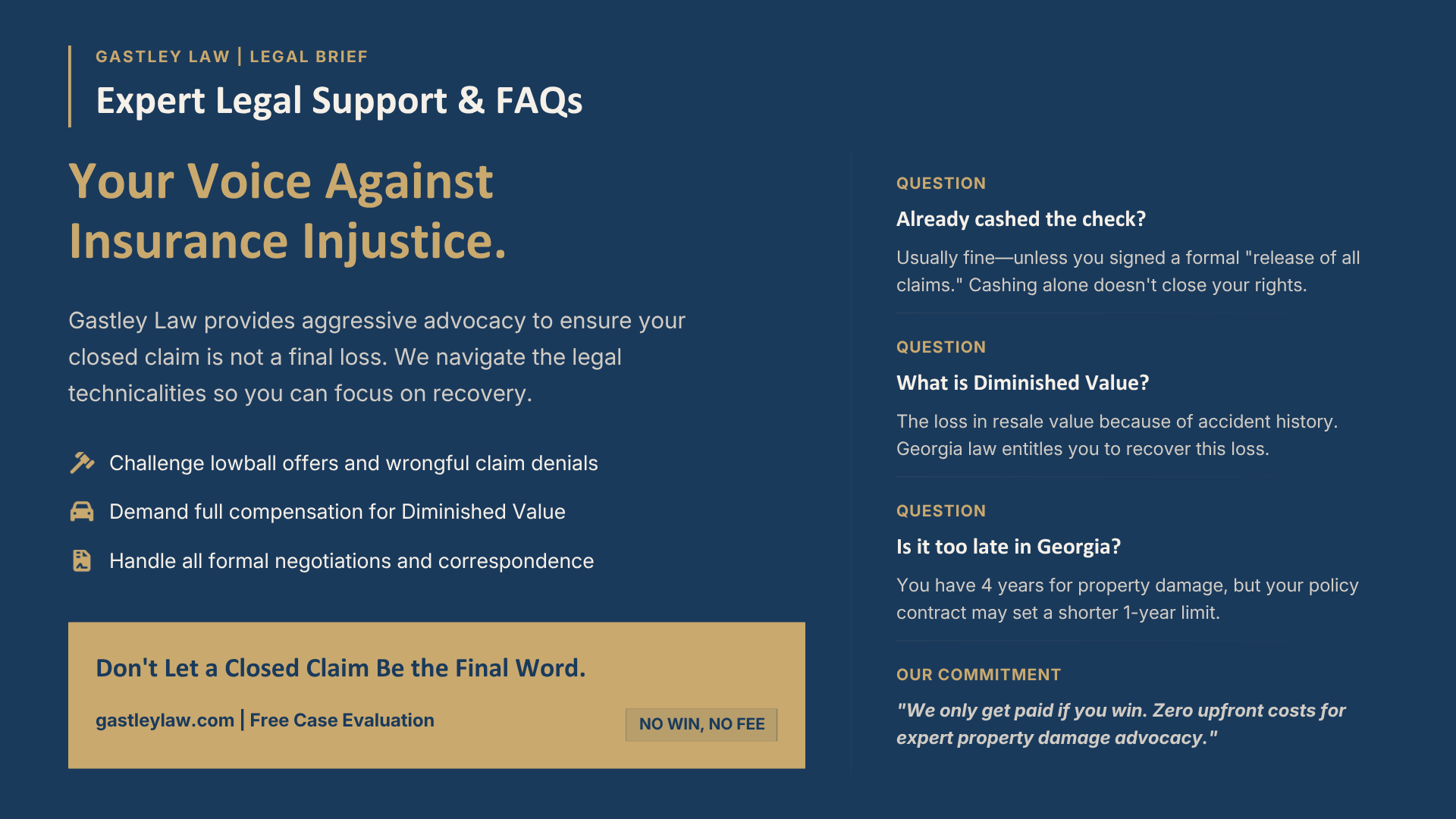

How Gastley Law Can Fight for You

At Gastley Law, we specialize in property damage and diminished value claims. It’s what we do every single day. We can review your closed claim and fight to get you the compensation you were really owed from the start. Unlike general practice firms, our team has deep expertise in this specific area of law and a track record of successfully challenging insurance companies. We take over the entire process for you, from filing the paperwork to aggressively negotiating with adjusters. Our goal is to handle the fight so you can focus on your life, all while we work to maximize your settlement. If you’re ready to see how our specialized legal representation can make a difference, we invite you to contact us for a straightforward evaluation of your case.

Related Articles

- How to File a Property Damage Claim in 5 Steps

- How to Dispute an Insurance Claim & Win Your Appeal

- Car Insurance Denies Your Claim? What to Do Next

Frequently Asked Questions

What if I already cashed the insurance check? Does that mean my claim is closed for good?

Not usually. Cashing a check for the initial repair estimate often just means the insurance company has administratively closed your file. The real point of no return is signing a “release of all claims” document. If you never signed a final release, you likely still have the right to submit new evidence, like a higher repair bill or a diminished value report, and request additional payment.

How long do I have to reopen a claim in Georgia?

You are working against two different timelines. Georgia law generally gives you four years from the date of the accident to file a lawsuit for property damage. However, your own insurance policy contract likely has a much shorter deadline for reopening a claim, sometimes as little as one year. It is very important to check your policy and act quickly once you discover a reason to reopen your claim.

My mechanic found more damage after starting repairs. Is it too late to ask for more money?

No, it is not too late, and this is one of the most common reasons to reopen a claim. The initial insurance estimate is often based only on visible damage. If your mechanic uncovers hidden structural or mechanical problems, you should immediately get an updated, itemized estimate and photos. This new evidence is exactly what you need to go back to the insurer and prove that the original settlement was not enough to cover the full cost of repairs.

What is “diminished value” and why wasn’t it in my first settlement?

Diminished value is the loss in your car’s resale price simply because it now has an accident on its record, even after it has been perfectly repaired. Most insurance companies will not volunteer to pay for this loss because their goal is to settle claims for the lowest amount possible. If your settlement did not include compensation for diminished value, you have a very strong reason to reopen your claim and demand the money you are owed.

I feel overwhelmed and the insurance company isn’t listening. What’s the first step to getting a lawyer’s help?

The first step is simple and doesn’t have to be intimidating. It usually starts with a straightforward conversation to review your situation. An experienced attorney can look at your original settlement and the new evidence you have to see if you have a strong case. If you feel like you are being ignored or given the runaround, reaching out for a case evaluation is a great way to understand your rights and get a professional on your side.