How to File an Allstate Diminished Value Claim

Going up against a massive insurance company like Allstate can feel incredibly intimidating. They have teams of adjusters and lawyers whose job is to protect the company’s bottom line, which often means paying you as little as possible. But when your car loses value after an accident that wasn’t your fault, you have a right to be compensated for that loss. It’s not a favor; it’s what you’re legally owed. Filing a diminished value claim in Allstate is your tool to hold them accountable, but you need a solid strategy. This article breaks down their playbook and gives you the steps to build a strong case and negotiate effectively.

Key Takeaways

- Get a professional appraisal to prove your loss: Don’t rely on the insurance company’s lowball calculation. An independent appraisal provides objective, data-driven proof of your car’s lost market value, giving you the essential leverage to demand a fair settlement.

- Understand Georgia’s rules and act quickly: In Georgia, you can file a claim against the at-fault driver’s insurance, but you must act within the four-year statute of limitations. Start the process as soon as repairs are done to preserve evidence and build a strong case.

- Don’t accept the first offer: A low offer or an initial denial is a standard negotiation tactic, not the final word. If the insurer refuses to negotiate fairly, it’s a clear sign that involving an attorney can strengthen your position and help you recover the full amount you are owed.

What Is a Diminished Value Claim?

Let’s start with the basics. A diminished value claim is a way to recover the loss in your car’s market value after it’s been in an accident. Even if your car is repaired perfectly and looks brand new, its value has likely dropped. Why? Because it now has an accident history. When you decide to sell or trade in your vehicle, potential buyers (especially dealerships) will see the accident on the vehicle history report and won’t be willing to pay top dollar for it. That difference between your car’s pre-accident value and its post-repair value is the “

Think of it this way: if you were choosing between two identical used cars, but one had a clean record and the other had been in a collision, you would almost certainly pay more for the one with no accident history. That stigma is real, and it directly impacts your wallet. A diminished value claim is your tool to get compensation for that financial loss from the insurance company. It’s not about fixing the physical damage; it’s about making you whole for the value your car has permanently lost. Insurance companies are responsible for restoring your vehicle to its pre-accident condition, and that includes its market value. Filing a claim is how you ensure they cover the full extent of your damages, not just the repair bill.

How Diminished Value Works After a Car Accident

After an accident, your primary focus is usually on getting your car repaired. But once the body shop is done, another type of loss remains: inherent diminished value. This is the automatic drop in value that happens simply because the accident is now part of your car’s permanent record. Even with the highest quality repairs using original manufacturer parts, the vehicle is now branded as “in an accident,” and that history follows it forever.

This isn’t just a theoretical loss. It becomes very real when you try to sell your car. Buyers can easily pull up a vehicle history report and will use the accident to negotiate a lower price. The insurance company’s responsibility is to restore your vehicle to its pre-accident condition, and that includes its value. Filing one of these property damage claims is how you hold them accountable for the full scope of your loss, not just the cost of new parts and labor.

The Different Types of Diminished Value

It’s helpful to know that “diminished value” can be broken down into three distinct categories. Understanding which one applies to your situation is key to building a strong claim.

Inherent Diminished Value: This is the most common type and the one we’ve been focusing on. It’s the loss of market value that exists simply because your vehicle now has an accident history, even if the repairs were flawless. This is the core of most claims filed by vehicle owners.

Repair-Related Diminished Value: This type of loss occurs when the repairs themselves are subpar. Think mismatched paint, aftermarket parts that don’t fit right, or lingering mechanical issues. This value loss is in addition to the inherent diminished value and is based on the poor quality of the repair work.

Immediate Diminished Value: This refers to the loss in value immediately after an accident but before any repairs have been made. It’s essentially the difference between the car’s pre-accident value and its value in a damaged state. This type is less commonly claimed since the cost of repairs is typically covered separately by the insurance policy.

Will Allstate Pay a Diminished Value Claim?

After an accident, your biggest concern is getting your car repaired and back on the road. But what about its lost resale value? This is where a diminished value claim comes in. If you’re dealing with Allstate, you might be wondering if they’ll even consider paying for this loss. The short answer is yes, but it’s rarely a straightforward process. Like most insurance companies, Allstate isn’t going to offer a payout without a little push. You need to understand their process and build a strong case to get the compensation you deserve.

Understanding Allstate’s Official Policy

So, does Allstate actually pay for diminished value? Generally, yes. Allstate has an established process for handling these types of claims, but that doesn’t mean every claim gets a green light. Approval depends entirely on the specifics of your situation. Think of it less as a simple request and more as a case you need to prove. While they have a policy in place, the burden is on you to show that your vehicle lost value and provide clear evidence of how much. Understanding what diminished value is and how it applies to your car is the first step toward a successful claim.

When Allstate Is Likely to Consider Your Claim

To get Allstate to take your claim seriously, you need to come prepared. The single most important piece of evidence you can have is a professional, certified appraisal detailing your vehicle’s loss in value. Allstate will also look at several other factors, including your car’s age, mileage, previous accident history, and the extent of the recent damage. Typically, you can only file a diminished value claim if the other driver was at fault. Fortunately, Georgia’s laws are favorable to these claims, making it a better place to file than many other states. Having an expert handle your property damage claim can make all the difference in showing Allstate you mean business.

Are You Eligible to File with Allstate?

Before starting your claim, it’s crucial to know if you’re eligible to file with Allstate. Not every accident qualifies, and insurers have specific rules. Your eligibility usually depends on three things: your car’s age and mileage, who was at fault, and Georgia’s specific laws. Understanding these points is the first step toward a successful claim.

Vehicle Age and Mileage Rules

Allstate will review your car’s history to decide if it qualifies for a diminished value payment. They consider its age, mileage, prior accidents, and the severity of the recent damage. A newer car with low mileage and a clean record often has the strongest case. However, don’t rule out your vehicle if it’s older. Any car that has lost significant market value from an accident could be eligible. The goal is to prove the car is worth less now than it was before the crash, even with perfect repairs. A professional appraisal can establish this loss in value.

How Being At-Fault Affects Your Claim

Who caused the accident is a critical factor. In Georgia, you can only file a diminished value claim against the at-fault driver’s insurance, which is a third-party claim. You cannot file against your own Allstate policy if the accident was your fault. So, if an Allstate-insured driver hit you, you can and should pursue a claim with them. A clear police report makes this process much simpler. If fault is disputed, an expert review of your property damage claim can be essential to getting the compensation you deserve.

Georgia’s Laws and Filing Deadlines

Fortunately, Georgia is one of the best states for these claims. Our laws recognize that a vehicle loses value after an accident, giving you a strong legal foundation. You don’t have to argue that diminished value is real, just that your car suffered from it. However, you must act promptly. Georgia has a four-year statute of limitations for property damage from the accident date. While that seems like a long time, it’s wise to begin as soon as repairs are done. Evidence can disappear and memories fade, so don’t wait. If you’re ready, you can contact an attorney to review your case.

How to File a Diminished Value Claim with Allstate

Filing a claim with a major insurance provider like Allstate can feel intimidating, but it’s entirely manageable when you follow a clear process. The key is to be organized, persistent, and prepared. Think of it as building a case, where every piece of evidence you gather strengthens your position. By following these steps, you can confidently present your claim and work toward getting the compensation you deserve for your vehicle’s lost value.

Step 1: Confirm Your Eligibility and Gather Documents

First things first, you need to confirm that your situation qualifies for a diminished value claim. In Georgia, you can typically file if the accident wasn’t your fault. Once you’ve confirmed your eligibility, it’s time to gather your proof. This isn’t just about having the repair bill; it’s about creating a complete picture of your car’s value before and after the accident. Collect everything you can: photos of the damage, the final repair invoice, and records of your vehicle’s condition and history. This initial legwork is crucial because it lays the foundation for your entire claim and shows the insurer that you are serious and well-prepared from the start.

Step 2: Get a Professional Diminished Value Appraisal

This is arguably the most important step in the process. While you know your car has lost value, you need an expert to prove exactly how much. A professional, independent appraisal transforms your claim from a personal opinion into a factual, data-driven argument. An appraiser will analyze your vehicle’s specific damage, repair quality, and local market data to produce a credible report. This document becomes the centerpiece of your claim, giving you a specific dollar amount to demand from Allstate. Without it, you’re just guessing, and the insurance adjuster has all the leverage. Investing in a quality appraisal gives you the evidence needed to stand your ground.

Step 3: Send a Formal Demand Letter

Once you have your appraisal report and supporting documents, it’s time to formally submit your claim. You’ll do this by sending a demand letter to the Allstate adjuster handling your case. This letter should be clear, professional, and straight to the point. State that you are seeking compensation for your vehicle’s diminished value and include the specific amount from your appraisal report. Be sure to attach copies of all your evidence: the appraisal, the final repair bill, and any other relevant documents. This letter officially puts Allstate on notice and kicks off the negotiation process. If you’re unsure how to draft this, it’s a good time to get in touch with an attorney.

Step 4: Prepare to Negotiate

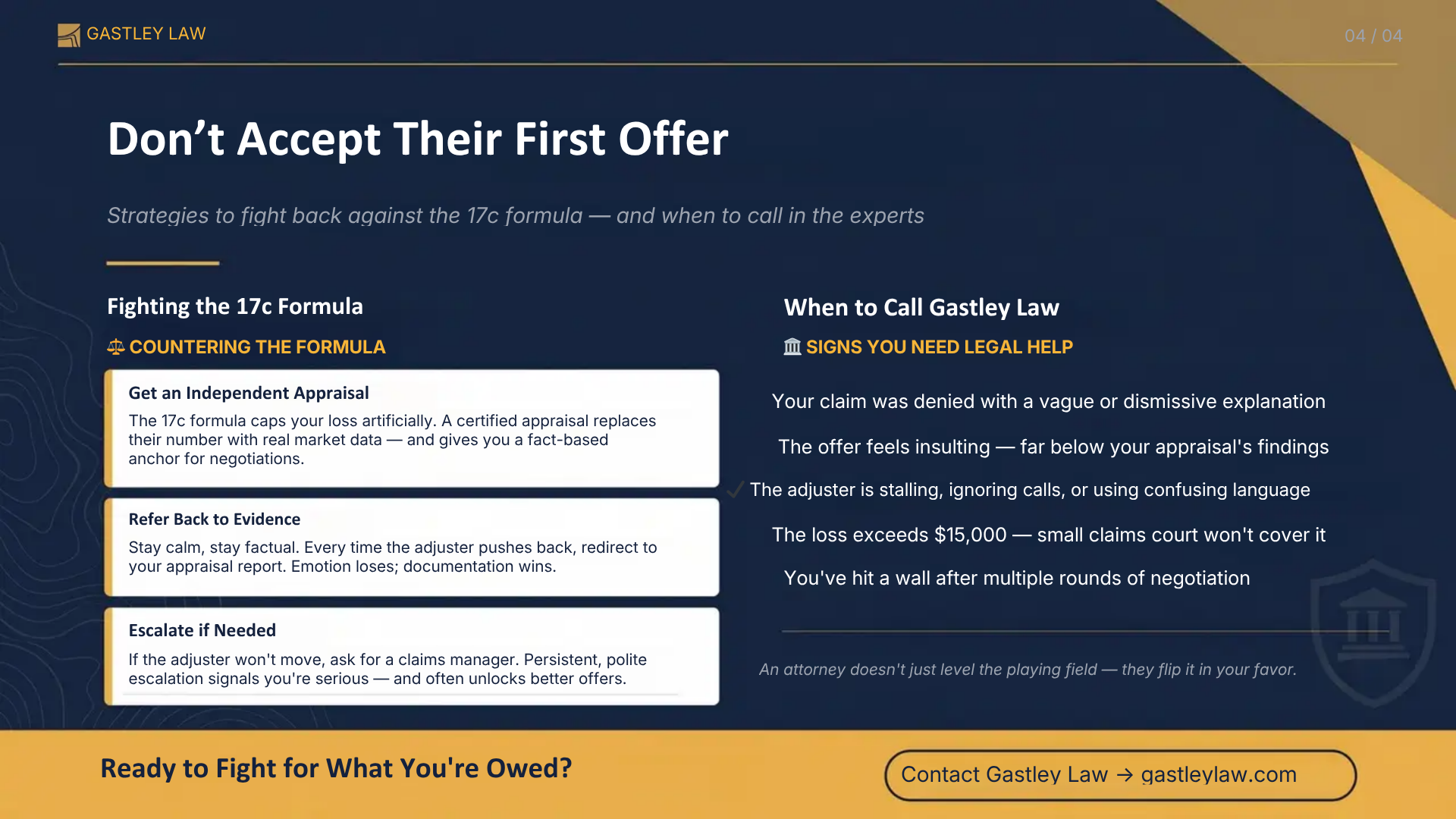

It’s rare for an insurance company to accept the initial demand without some pushback. Be prepared for Allstate to respond with a low offer or even an initial denial. Don’t get discouraged; this is a standard part of the process. When you negotiate, stay calm and stick to the facts. Your appraisal report is your best tool, so refer back to it consistently. If the adjuster isn’t willing to offer a fair amount, don’t be afraid to ask to speak with a supervisor. Firm, polite persistence is key. Remember, you have the evidence on your side. The goal is to have a productive conversation that leads to a fair settlement based on the proof you’ve provided.

How Does Allstate Calculate Diminished Value?

When you file a diminished value claim, you’re asking for compensation for the loss in your car’s market value. But how does an insurance company like Allstate actually put a number on that loss? It’s not a simple process, and their goal is often to pay as little as possible. They rely on specific formulas and factors that tend to favor them, not you.

Allstate, like many other insurers, has a standard method for calculating this loss. They often use an internal formula known as “17c,” which has a reputation for producing lowball offers. This formula doesn’t always account for the real-world perception of a vehicle with an accident history. Understanding how they arrive at their number is the first step in building a case for what you’re truly owed. Knowing their playbook helps you prepare a stronger counter-argument and fight for the full compensation your vehicle has lost. If you’re just getting started, learning more about what diminished value is can give you a solid foundation.

A Look at the 17c Formula

The 17c formula is a calculation that many insurance companies in Georgia use to determine diminished value, and it almost always results in a low offer. The formula starts by capping the maximum diminished value at 10% of your car’s pre-accident value (often based on NADA guides). From there, it applies two “modifiers” to reduce that amount even further. The first is a damage modifier, which reduces the payout based on the severity of the damage. The second is a mileage modifier, which reduces it again based on how many miles are on your car. This multi-step reduction process is why the final offer rarely reflects the true market loss.

Factors That Reduce Your Vehicle’s Payout

Beyond the 17c formula, Allstate looks at several specific details about your vehicle to justify a lower payout. They will closely examine your car’s age and mileage, as older vehicles with more miles are typically assigned a lower starting value. They will also investigate its accident history; if your car has been in a previous collision, they will use that to argue for a smaller diminished value amount this time around. Finally, the severity and type of the recent damage play a huge role. Cosmetic damage might receive a lower consideration than structural damage, even if both significantly impact resale value. Each of these factors is a lever Allstate can pull to minimize what they have to pay you, which is why having an expert evaluate your property damage claim is so important.

What to Expect from the Allstate Claims Process

Dealing with an insurance claim can feel like a full-time job, but knowing what to expect can make the process a little smoother. Allstate, like any major insurer, has a specific system for handling claims. It’s designed to be efficient for them, but it might not always feel straightforward for you. The key is to be prepared, persistent, and to understand your rights. From the initial filing to the final negotiation, you’ll likely interact with an adjuster whose goal is to resolve the claim based on the company’s internal guidelines. This process can involve a lot of back-and-forth, so keeping detailed records of every conversation and document is one of the best things you can do for yourself. Let’s walk through what you can anticipate when you file a diminished value claim with Allstate.

How Long Will Your Claim Take?

The timeline for a diminished value claim can vary quite a bit. Some are settled in a few weeks, while others can take several months, especially if you have to negotiate or escalate the issue. While the claim process itself has a flexible timeline, there’s a firm legal deadline you can’t miss. In Georgia, the statute of limitations for filing a claim for damage to personal property is typically four years from the date of the accident. This might sound like a lot of time, but it’s best to start the process as soon as your vehicle repairs are complete. Gathering evidence and building a strong case takes time, so don’t wait until the last minute to get started.

Common Reasons Allstate Denies Claims

It’s frustrating, but initial denials are a common part of the claims process. Insurance companies are businesses, and they often look for reasons to deny claims or pay out less. One common reason you might hear is that your car was in a previous accident, so its value was already diminished. They might argue the most recent accident didn’t cause any additional loss in value, which is often not the case. Another tactic is to simply make the process difficult, hoping you’ll get tired and give up. If your claim is denied, don’t be discouraged. It’s often just the first step in the negotiation, and having an expert handle the legal representation can make all the difference.

What to Do If You Get a Lowball Offer

If Allstate doesn’t deny your claim outright, they will likely come back with a low settlement offer. Insurers often use a standard calculation known as the “17c formula” to determine diminished value. This formula has been widely criticized because it tends to produce a much lower figure than the actual market value your car has lost. It doesn’t fully account for how real buyers perceive a vehicle with an accident history. If you receive an offer that seems too low, don’t accept it. Your first step is to present your independent appraisal and negotiate for a fair amount. If the adjuster won’t budge, you can ask to speak with a claims manager. Understanding what diminished value truly is will give you the confidence to push back.

How to Get the Most from Your Diminished Value Claim

Getting the full amount you’re owed from an insurance company requires a solid strategy. Allstate won’t just hand over a check for the true value your car has lost; you have to prove it. This means being prepared, organized, and persistent. By taking a few key steps, you can build a powerful case that stands up to the adjuster’s arguments and helps you secure a fair payout. It’s about arming yourself with the right information and knowing how to use it effectively during negotiations.

Why You Need an Independent Appraisal

The single most important step you can take is to get a professional, independent diminished value appraisal. The insurance adjuster will have their own calculation, often based on a formula like 17c, which almost always results in a lowball offer. An independent appraisal from a certified expert provides an unbiased, detailed report on your vehicle’s specific loss in value. This document becomes your strongest piece of evidence. It’s not just an opinion; it’s a professional assessment that gives you a credible, fact-based number to anchor your negotiations and counter the insurer’s low offer.

How to Build a Strong Case with Evidence

Your appraisal is the star of the show, but you need a strong supporting cast of documents to back it up. Think of it as building a file for your claim. Start gathering everything related to the accident and repairs. This includes the official police report, which helps establish fault, and the final, itemized repair bill from the body shop. If you have photos of your car before the accident, great. If not, be sure to take clear photos of the repaired areas. This collection of evidence creates a complete picture of the incident and proves the extent of the damage and subsequent loss in value.

Negotiation Strategies That Actually Work

When you talk to the claims adjuster, stay calm and stick to the facts. Your independent appraisal is your most powerful tool, so refer back to it constantly. Adjusters are trained to use common arguments, like saying the repairs made your car “whole again.” Use your appraisal to calmly explain why that isn’t true from a market value perspective. If the adjuster won’t budge, don’t be afraid to ask to speak with a claims manager. If you still hit a wall, know that you have options. Sometimes, having an experienced attorney handle the negotiations is the best way to show the insurance company you’re serious about your claim.

Common Mistakes That Can Hurt Your Allstate Claim

Filing a diminished value claim can feel like a maze, and a few wrong turns can unfortunately cost you. Knowing what to watch out for is the best way to protect your claim’s value and ensure you get the compensation you deserve.

Avoid These Paperwork and Documentation Errors

When you’re dealing with an insurance company, proof is everything. Allstate won’t just take your word for it; you need to build a strong case with solid evidence. A certified professional appraisal of your car’s lost value is the cornerstone of your claim and dramatically increases your chances of getting paid. You should also gather the official police report, the final detailed repair bill, and clear photos of your car both before the accident (if you have them) and after the repairs. Think of it as creating a complete story of your car’s diminished value that the adjuster can’t ignore.

Don’t Miss Important Deadlines

Timing is critical when it comes to property damage claims. Each state has a law called the “statute of limitations,” which sets a firm deadline for filing a lawsuit to recover your losses. In Georgia, you generally have four years from the date of the accident to file a claim for property damage. While that might sound like a lot of time, it can pass quickly when you’re dealing with repairs and negotiations. If you miss this deadline, you lose your right to pursue the claim forever. It’s always best to start the process as soon as possible to avoid any last-minute issues.

Why You Shouldn’t Accept the First Offer

It’s important to remember that Allstate’s first offer is often just a starting point for negotiations, not the final amount. Insurance adjusters are trained to settle claims for the lowest possible amount, so their initial offer may not reflect the true value of your loss. Don’t feel pressured to accept it right away. If the offer seems too low, you have the right to push back. You can present your evidence, explain why you deserve more, and even ask to speak with a claims manager. Standing firm shows you’re serious about getting fair compensation for your property damage claim.

When Should You Get a Lawyer for Your Claim?

While you can certainly file a diminished value claim on your own, there are moments when bringing in a legal professional is the best strategic move. Insurance companies like Allstate have entire departments filled with adjusters and lawyers whose main job is to minimize payouts. It’s an uneven playing field, and it’s easy to feel overwhelmed by their resources and experience. If you’ve presented a solid case but are getting nowhere, it might be time to get help.

Think of an attorney not as a last resort, but as a powerful tool to ensure you’re treated fairly. Working with an experienced Atlanta diminished value attorney can improve your negotiating position and help maximize the value of your claim. They understand the specific arguments and legal precedents that make insurers take a claim seriously. Getting legal advice can be particularly helpful if your claim is complex, involves significant value, or if the insurance company is simply refusing to negotiate in good faith. An experienced lawyer can manage the entire process, from negotiations to potential legal action, giving you peace of mind and a much better chance at recovering the full amount your vehicle has lost in value.

Signs It’s Time to Ask for Legal Help

You’ve submitted your professional appraisal and a clear demand letter, but Allstate is giving you the runaround. This is a classic sign that you might need legal backup. If your claim is outright denied with a vague explanation, or if you receive a lowball offer that feels insulting, it’s time to consider your options. Pay attention to the adjuster’s behavior. Are they delaying the process, ignoring your calls and emails, or using confusing jargon to make you second-guess your claim? These are common tactics used to frustrate you into giving up or accepting less than you deserve. When you feel like you’ve hit a wall, it’s a strong indicator that a lawyer’s intervention is needed to move forward.

How an Attorney Can Strengthen Your Case

Hiring an attorney does more than just show the insurance company you’re serious. A lawyer specializing in diminished value claims builds a robust, evidence-based case that is difficult for an insurer to ignore. They gather all the necessary proof, including your independent appraisal, repair records, and vehicle history, and present it in a formal legal context. They know how to counter the formulas and arguments adjusters use to undervalue your car. Most importantly, an attorney handles all the stressful negotiations for you. If Allstate still refuses to offer a fair settlement, your lawyer can file a lawsuit against the at-fault driver, which legally compels their insurer to pay the judgment. If you’re facing a tough fight, contact us to see how we can help.

What If Allstate Denies Your Claim?

Receiving a denial letter from Allstate can feel like hitting a brick wall. It’s frustrating, especially when you know your car has lost value. But a denial is not the final word on your claim. It’s simply the insurance company’s first move, and you have several strong countermoves available. Instead of giving up, you can re-evaluate your strategy and explore other avenues to get the compensation you deserve.

An initial rejection often happens because the insurer is banking on you not pushing back. They might use internal formulas or cite policy exclusions, hoping you’ll accept their decision without question. This is where understanding your rights becomes critical. You don’t have to take their assessment at face value. Whether the other driver was at fault or you’re dealing with your own policy, there are clear, actionable steps you can take. The key is to shift your approach from simply requesting payment to building a case that legally obligates them to pay.

Your Option to File with the Other Driver’s Insurance

If Allstate is your insurance provider and they deny your first-party diminished value claim, your best option is often to pursue the at-fault driver’s insurance company instead. In Georgia, the responsible party’s insurer is legally obligated to cover your vehicle’s loss in value. It’s generally much easier to get a payout from the other driver’s policy than from your own, as most personal auto policies don’t explicitly cover diminished value for the policyholder.

This shifts the entire dynamic. You are now a third-party claimant, and you have a strong legal standing to demand compensation for your car’s reduced market price. This is a core part of our property damage claim services, and it’s often the most effective path forward after a denial from your own insurer.

Deciding Between Small Claims Court and a Lawsuit

If the at-fault driver’s insurance company also refuses to pay, your next step is legal action. It’s important to know that you typically sue the at-fault driver directly, not their insurance company. However, their insurer is still responsible for paying the judgment if you win. For smaller claims, you can file in Magistrate Court, also known as small claims court in Georgia, for losses up to $15,000. This process is less formal and doesn’t always require an attorney.

For losses exceeding that amount, you’ll need to file a lawsuit in a higher court. This is a more complex process where having experienced legal representation is crucial to building a strong case and handling the formal procedures. If you find yourself in this situation, it’s time to get in touch with an attorney to discuss your options.

Related Articles

- Georgia Diminished Value Requirements Explained

- How to Negotiate a Diminished Value Claim: A Guide

- Diminished Value Claims in Georgia | Gastley Law

- How to Negotiate a Diminished Value Settlement

Frequently Asked Questions

Can I file a diminished value claim if the accident was my fault?

In Georgia, you can only file a diminished value claim against the at-fault driver’s insurance company. You cannot file this type of claim against your own Allstate policy if you were the one who caused the accident. The claim is meant to hold the responsible party accountable for the full scope of the damage they caused, which includes your car’s loss in market value.

Is it worth filing a claim if my car isn’t brand new?

Yes, it can absolutely be worth it. While newer cars with low mileage often have the strongest cases, any vehicle that has lost significant market value because of an accident could be eligible. The focus is on proving that the car is worth less now than it was before the crash, even after perfect repairs. A professional appraisal can establish this loss regardless of your car’s age.

What is the single most important thing I need for a successful claim?

Without a doubt, you need a professional, independent diminished value appraisal. This report, prepared by a certified expert, provides a credible and data-driven assessment of your vehicle’s loss in value. It transforms your claim from a personal opinion into a factual argument and gives you the leverage needed to counter the insurer’s inevitable low offer.

Why was Allstate’s settlement offer so low?

Allstate, like most insurers, often uses a standard calculation known as the 17c formula to determine a payout. This formula is designed to minimize what they have to pay by capping the potential loss and then applying additional reductions for damage severity and mileage. The final number rarely reflects the true loss in your car’s resale value in the real world.

Do I really need to hire a lawyer for this?

You don’t always need one, but it’s a very strategic move if Allstate denies your claim, makes an insulting offer, or starts using delay tactics. An attorney signals to the insurance company that you are serious about getting fair compensation. They can handle the stressful negotiations and, if necessary, take legal action to get you the money you are owed.