Diminished Value Appraisal Cost: Is It Worth It?

Insurance companies have a simple goal: pay out as little as possible. After an accident, their initial offer for your car’s lost value will likely be disappointingly low, based on a formula that benefits them, not you. So, how do you fight back? You come prepared with undeniable proof. A professional diminished value appraisal is your single most powerful tool in this negotiation. It replaces their biased calculation with a fact-based assessment from an independent expert. Before you can leverage this tool, you need to understand the diminished value appraisal cost and see it as the price of leveling the playing field.

Key Takeaways

- Prove your car’s lost value with a professional report: An independent appraisal provides the concrete evidence needed to counter an insurance company’s lowball offer and formally document your financial loss.

- A quality appraisal is a smart investment: While costs typically range from $300 to $600, a detailed report from a certified appraiser can help you recover thousands more in your settlement, making it a worthwhile expense.

- Prepare for the process and know when to get help: Organize your repair bills and accident reports for your appraiser, and remember that if the insurer still won’t negotiate fairly, it’s time to seek legal advice.

What Is a Diminished Value Appraisal?

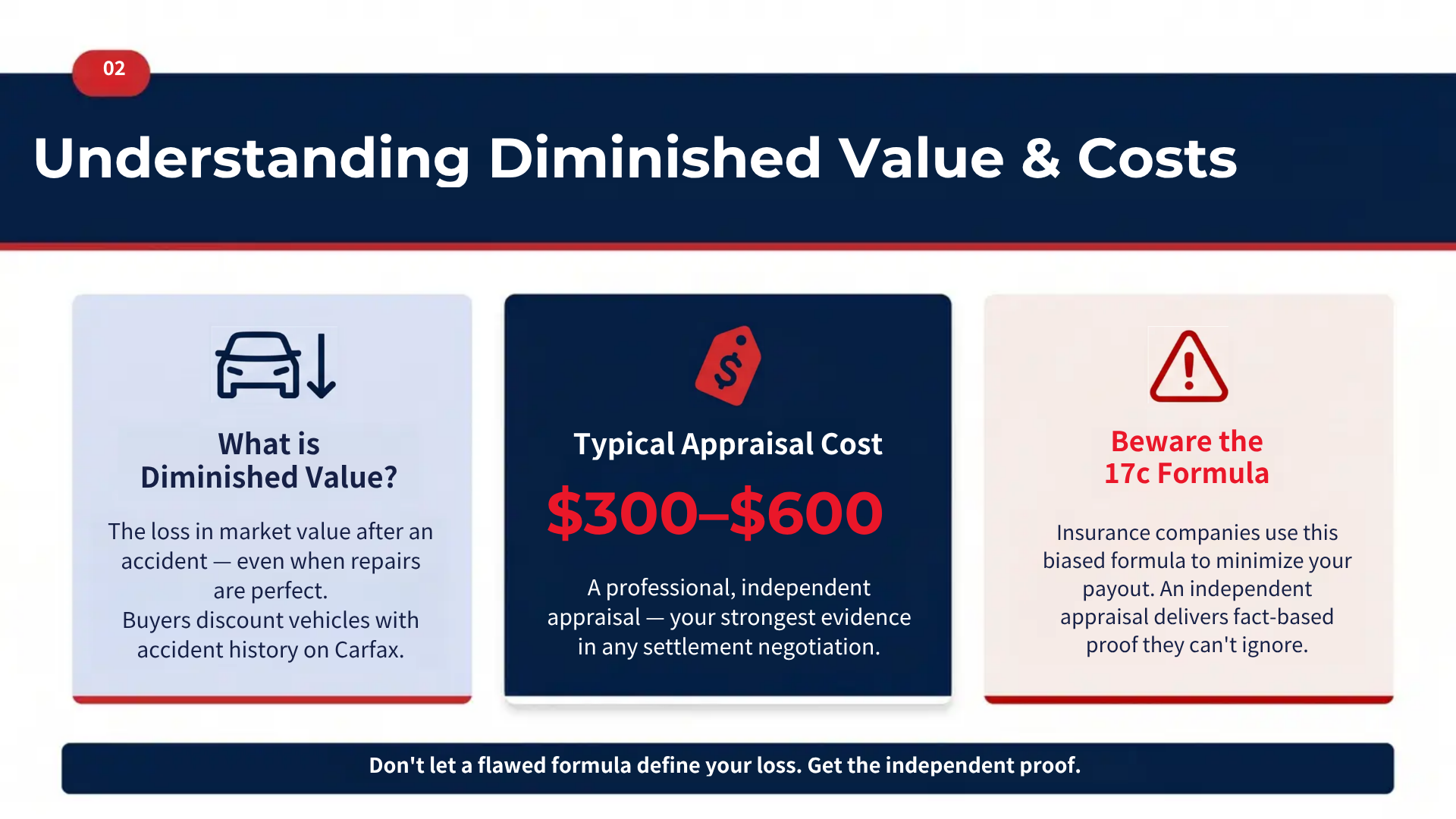

After a car accident, your first priority is getting your vehicle repaired and back on the road. But even with the best bodywork, your car’s value has likely taken a hit. An accident history can significantly lower its resale price, and that loss is real money out of your pocket. This is where a diminished value appraisal comes in. It’s a professional assessment that calculates exactly how much value your car has lost because of the accident.

Think of it as an expert report that proves your financial loss. Instead of just accepting the insurance company’s lowball offer (or worse, their claim that there’s no loss at all), an appraisal gives you solid evidence to support your claim. It’s a critical tool for recovering the money you’re rightfully owed. This report becomes the foundation of your diminished value claim, ensuring you have the documentation needed to argue your case effectively.

What is diminished value?

Let’s break it down. Diminished value is the difference between your car’s market value right before the accident and its value after it has been fully repaired. Even if your car looks and drives like new, its accident history will show up on vehicle reports like CarFax. A smart buyer will always choose a similar car with a clean history or demand a steep discount for one that’s been in a wreck.

This loss in resale value is what’s known as inherent diminished value, and it’s the most common type of claim. You are legally entitled to be compensated for this loss, but insurance companies won’t pay it unless you can prove it. That’s why getting a professional appraisal is so important.

When should you get an appraisal?

Timing is key. You should get an appraisal after your vehicle has been repaired, or at least once the repairs have started. This allows the appraiser to see the full extent of the damage and the quality of the repair work, which are both crucial factors in their assessment. If you get an appraisal too early, it will be based on estimates, not the final outcome.

Typically, you can file a diminished value claim against the at-fault driver’s insurance company. An appraisal provides the official documentation you need to support your claim, which is a key part of our legal services. Having a detailed, professional report shows the insurer that you’re serious and have a well-supported case for the compensation you deserve.

How Much Does a Diminished Value Appraisal Cost?

Thinking about getting a diminished value appraisal is a smart move, but it’s natural to wonder about the cost. After all, you’re already dealing with repair bills and insurance headaches. The good news is that an appraisal is an investment, not just another expense. It’s a tool that provides the proof you need to claim the money you’re rightfully owed. Let’s break down what you can expect to pay and why it’s often one of the best financial decisions you can make after an accident.

What’s the typical price range?

A professional diminished value appraisal usually costs between $300 and $600. The exact price can depend on a few things, like the type of vehicle you have, how complex the damage is, and the appraiser’s experience. Think of it like paying for any other expert service. You’re hiring a professional to conduct a detailed analysis and create a report that holds up against the insurance company’s arguments. This report is the key to proving your car’s diminished value and is much more credible than a simple estimate you might find online. While the upfront cost is a factor, it’s important to weigh it against the potential return.

Is the cost worth the potential payout?

Absolutely. Spending a few hundred dollars on a solid appraisal can help you recover thousands in your settlement. Without an independent report, you’re left with the insurance adjuster’s low offer, which rarely reflects your car’s true loss in value. An appraisal gives you the leverage and documentation needed to negotiate effectively. Many drivers who invest in an appraisal see payouts that are significantly higher than their initial offers, sometimes by $6,000 or more. When you look at it that way, the appraisal fee is a small price to pay for a much fairer outcome. If you’re ready to challenge the insurer’s offer, we can help you get started.

What Affects the Price of an Appraisal?

When you start looking for a diminished value appraisal, you’ll quickly notice that prices can vary quite a bit. There isn’t a single flat rate, because the cost depends on several key factors. Think of it like hiring any other expert; you’re paying for their time, knowledge, and the specific work your situation requires. Understanding what goes into the pricing will help you choose a qualified appraiser and know what to expect. From the type of car you drive to the appraiser’s credentials, each element plays a role in the final cost. Let’s break down exactly what influences the price of a professional appraisal.

Your vehicle type and the extent of the damage

Not all cars are created equal, and the same goes for appraisals. The cost often reflects the complexity of the job. Appraising a standard, popular sedan with minor fender damage is typically more straightforward than assessing a classic car, a luxury vehicle, or a heavily customized truck. These unique vehicles require specialized knowledge of their market value, parts, and repair processes, which can increase the appraisal fee. Similarly, the severity of the damage matters. A vehicle with extensive structural damage requires a much more detailed inspection and analysis than one with a few cosmetic scrapes, which will be reflected in the price.

The appraiser’s experience and credentials

When you hire an appraiser, you’re paying for their expertise. An appraiser with years of experience, industry certifications, and a strong reputation for successfully challenging insurance companies will likely charge more than a newcomer. This experience is valuable because their reports carry more weight and are harder for insurers to dismiss. A seasoned professional knows exactly what evidence to look for and how to present it in a compelling way. While it might be tempting to go with the cheapest option, a low-cost appraisal from an inexperienced individual could end up costing you more if it fails to get you the compensation you deserve.

Your location and any travel fees

Geography can also play a part in the cost of an appraisal. If an appraiser needs to travel a significant distance to physically inspect your vehicle, you can expect to see travel time and mileage fees added to your bill. Some appraisers work within a specific service area, while others are willing to travel further for an additional charge. To keep costs down, you might look for a qualified appraiser in your local area. However, don’t sacrifice quality for convenience. It’s often worth paying a bit more in travel fees for a highly respected appraiser who has a proven track record.

The quality and detail of the report

The single biggest factor affecting the price is the quality of the appraisal report itself. You may come across cheap, automated online reports that promise a diminished value figure for a low price. These are often generated by a simple algorithm and lack the detailed analysis needed to stand up to an insurance adjuster’s scrutiny. A professional, comprehensive report is a different story. It includes a thorough vehicle inspection, an analysis of the current market, comparisons to similar vehicle sales, and detailed documentation. This level of detail is what convinces an insurance company to increase their offer, making it a worthwhile investment in your claim.

What Does a Professional Appraisal Include?

When you get a professional diminished value appraisal, you’re not just getting a number on a piece of paper. You’re investing in a comprehensive, evidence-based report that builds the foundation of your claim. Think of it as the expert testimony you need to prove your car’s loss in value after an accident. Insurance companies often rely on their own internal formulas or quick online calculators, which are designed to minimize their payout. A professional appraisal is your most effective tool to counter their lowball offer with objective facts and a credible assessment from an unbiased expert.

This detailed evaluation is a multi-step process. It starts with a hands-on inspection of your vehicle, moves into a deep dive of local market data, and ends with a formal report that you can submit to the insurer. The appraiser’s job is to document exactly how the accident has impacted your car’s market worth, giving you the leverage you need for a fair negotiation. It transforms your claim from a simple request into a well-supported demand for the compensation you deserve. A proper appraisal considers the quality of the repairs, the severity of the damage, and your vehicle’s specific history, creating a complete picture that an insurer’s algorithm simply can’t replicate.

A thorough vehicle inspection

A credible appraisal always starts with a detailed, in-person inspection of your vehicle. While online calculators can give you a rough estimate, they can’t see the subtle signs of a post-accident vehicle. A professional appraiser physically examines the quality of the repairs, checks for any remaining structural issues, and assesses the overall cosmetic finish. This hands-on approach, sometimes called a “field appraisal,” is far more accurate because it catches the details that automated systems miss. An expert can spot things like mismatched paint, uneven panel gaps, or signs of frame damage that an insurer’s quick review might overlook, all of which directly impact your car’s resale value.

Market analysis and sales comparisons

After the inspection, the appraiser does their homework. They don’t just pull a number out of thin air; they conduct a detailed market analysis specific to your area. This involves researching recent sales data for vehicles just like yours: same make, model, year, and pre-accident condition. By establishing a clear pre-accident value, they can then accurately calculate the loss. This report proves how much value your car lost, and it’s the key to getting the insurance company to pay you what you’re owed. Because these professional reports use real market data, they are much harder for insurers to ignore or dispute.

A detailed report and official documentation

The final piece of the puzzle is the official report. This is a formal document that outlines the appraiser’s entire process and findings. It includes photos from the inspection, a summary of the damages and repairs, the market data used for comparison, and a clear explanation of how the final diminished value figure was determined. This report becomes your primary piece of evidence when negotiating with the insurance company. It shows you’ve done your due diligence and have a professional backing your claim. While there is an upfront cost, many people find the appraisal fee is reimbursed as part of their final insurance settlement, making it a smart investment in your claim.

Watch Out for These Hidden Fees

When you get a quote for a diminished value appraisal, it’s smart to ask if the price is all-inclusive. The initial number you hear might not cover everything, and surprise fees can pop up when you least expect them. Being aware of these potential extra costs from the start helps you budget properly and choose an appraiser who is transparent about their pricing. Think of it like getting a quote from a contractor; you want to know exactly what’s included. Before you agree to anything, make sure you’ve discussed these common add-ons.

Travel and mileage costs

If an appraiser needs to travel a significant distance to inspect your vehicle, you’ll likely have to cover their costs. This can include a per-mile charge or a flat travel fee. This is especially common if you live in a more rural area of Georgia and your appraiser is based in a major city like Atlanta. Always ask about travel fees upfront, particularly if the appraiser isn’t local. Getting this in writing can prevent a surprise charge on your final bill. If you’re unsure about finding a local expert, you can always contact us to discuss your specific situation.

Fees for rush service

Patience is a virtue, but sometimes you just don’t have time to spare. If you need an appraisal completed faster than the standard turnaround time, be prepared to pay a premium for it. Appraisers often charge a rush fee to prioritize your report over their other work. While this can be helpful if you’re up against a deadline with the insurance company, it’s an expense you can often avoid with a little planning. As soon as you think you might file a claim, start researching appraisers so you don’t have to pay extra for a last-minute request.

Charges for extra paperwork

The standard appraisal report is usually covered in the base fee, but what happens if your claim gets more complicated? If the insurance company disputes your claim and your case goes to court, you may need the appraiser to provide expert testimony. This service is almost never included in the initial cost. You could face additional charges for court preparation, depositions, or simply appearing in person, with fees often starting around $250 for the first couple of hours. This is a point where having expert legal representation becomes critical to manage these complexities.

How to Prepare for Your Appraisal

An appraisal is a detailed process, but you can set yourself up for success with a little preparation. Taking these steps beforehand not only helps the appraiser do their job more effectively but also strengthens your position when negotiating with the insurance company. Think of it as doing your homework to ensure you get the best possible grade, which in this case, is fair compensation for your vehicle’s loss in value. A bit of effort now can make a significant difference in the final outcome of your claim.

Gather these key documents

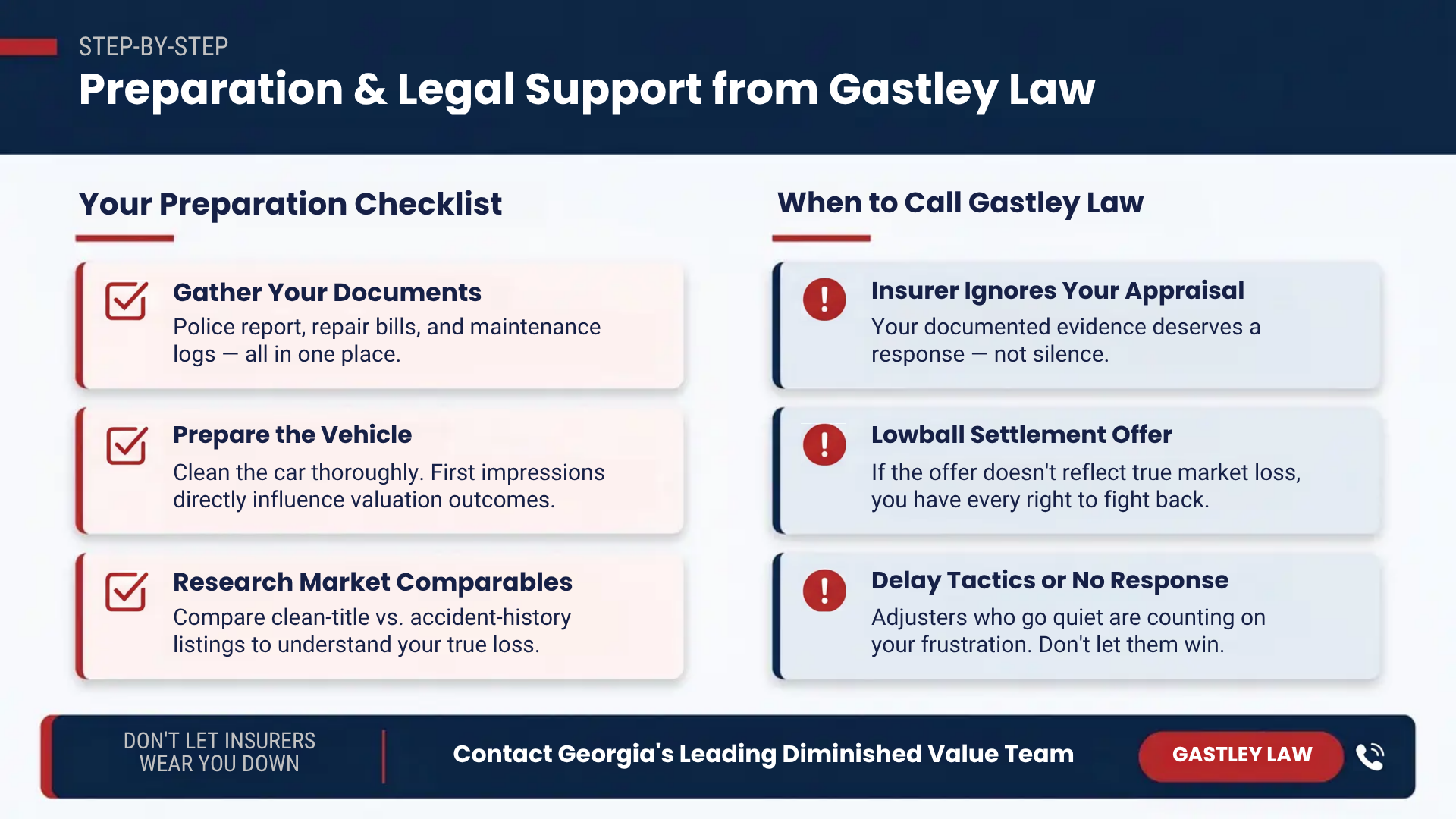

To build a strong case, you need a solid paper trail. Before the appraiser arrives, pull together all the important documents related to your vehicle and the accident. This includes the official police accident report, all repair bills and estimates, and any records that show your car’s value before the crash, like maintenance logs or the original bill of sale. Having this evidence organized provides a clear, factual basis for your diminished value claim and helps the appraiser create a comprehensive and accurate report. It shows you’re serious and prepared to fight for what you’re owed.

Get your vehicle ready

First impressions matter, even for a car appraisal. While the appraiser is focused on the accident damage, the overall condition of your vehicle plays a role in its valuation. Take some time to clean your car inside and out. A clean, well-maintained vehicle suggests that you took good care of it before the accident, which can positively influence the appraiser’s assessment of its pre-loss value. They will be looking at everything: the year, make, model, mileage, and any special features. Presenting your car in the best possible light helps them see its true worth.

Find comparable vehicle sales

Doing a little market research can go a long way. Before your appraisal, look up sales listings for vehicles that are the same make, model, year, and have similar mileage as yours. The key is to find two sets of examples: cars with a clean accident history and cars that have a reported accident in their past. The price difference between these two groups is a real-world example of diminished value. This information helps you understand what a fair outcome looks like and gives your appraiser solid market data to support their valuation. If you need guidance on this, don’t hesitate to reach out to us.

Common Myths About Diminished Value Appraisals

When you’re trying to get fair compensation for your car’s lost value, it’s easy to get tripped up by bad advice. A lot of misinformation floats around about diminished value claims and appraisals, and believing it can cost you money. Let’s clear up a few of the most common myths so you can approach your claim with confidence. Understanding the truth behind these misconceptions is the first step toward getting the full amount you’re owed.

Myth: You can do it yourself

While the DIY spirit is great for many things, a diminished value claim isn’t one of them. You might be tempted to pull some numbers from online car sites to save money, but insurance companies won’t take that seriously. A professional appraisal is a detailed, evidence-based report that proves exactly what diminished value is in your specific case. An expert appraiser provides an objective, credible document that carries weight in negotiations. Think of it as bringing an expert witness to the table; their report is the testimony that validates your claim and forces the insurer to listen.

Myth: The insurance company’s offer is fair

It’s important to remember that insurance companies are for-profit businesses, and their goal is to pay out as little as possible. Their first offer is almost never their best. Insurers in Georgia often use a standard calculation called the “17c formula,” which is notorious for producing a very low number that doesn’t reflect your car’s actual loss in market value. You should always treat their initial offer as a starting point for negotiation, not the final word. Our legal services are designed to challenge these lowball offers and fight for a fair settlement.

Myth: An appraisal guarantees a bigger check

An appraisal is a powerful tool, but it isn’t a golden ticket. Having a professional report significantly strengthens your position, but it doesn’t automatically guarantee a higher payout. The insurance company can still push back. The appraisal provides the solid evidence you need to argue your case effectively. Even if your car is repaired perfectly, its accident history will likely show up on a Carfax report, which can scare off future buyers and lower its resale value. An appraisal documents this loss, but securing the compensation still requires skillful negotiation.

Is an Appraisal Worth the Investment?

Deciding whether to pay for a diminished value appraisal can feel like a gamble. You’re already dealing with repair costs and insurance headaches, so is another expense really necessary? The short answer is: it depends. An appraisal isn’t always the right move for every situation, but when it is, it can be the single most important tool you have for getting a fair payout from the insurance company.

Think of it this way: you know your car is worth less after an accident, but the insurance adjuster’s job is to minimize how much they pay you. A professional appraisal is a detailed report that proves exactly how much value your car lost. It transforms your claim from a simple opinion into a fact-based demand. The key is to weigh the cost of the report against the potential return. For many drivers, especially those with newer cars or significant damage, the investment pays for itself several times over. We’ll walk through the main factors to help you make a smart decision.

Consider your car’s value

The first thing to look at is your car itself. A newer, high-value, or luxury vehicle will almost always have a larger diminished value than an older car with a lot of miles. If you drive a two-year-old SUV that was in a moderate collision, the loss in resale value could easily be thousands of dollars. In that case, spending a few hundred on an appraisal is a no-brainer.

However, if you have an older car with pre-existing wear and tear, the diminished value might be minimal. The goal is to make sure the potential payout is significantly more than the appraisal fee. A credible diminished value report gives you the concrete evidence needed to show the insurance company what you’re owed.

How severe is the damage?

The extent of the damage plays a huge role in your car’s loss of value. A minor fender bender with a few scratches might not be enough to warrant an appraisal. But if your vehicle had structural damage, frame repairs, or airbag deployment, its value has taken a serious hit. Even if the repairs make the car look perfect, the accident is now part of its permanent vehicle history report.

The biggest hurdle in a diminished value claim is proving that the accident truly caused your car to lose money. An independent appraisal from a certified expert does exactly that. It documents the severity of the damage and calculates the specific impact on your car’s market value, giving you the leverage you need to counter a lowball offer from the insurer.

Know Georgia’s laws and deadlines

Every state has its own rules for handling these claims, and Georgia is no exception. In Georgia, you have four years from the date of the accident to file a property damage claim, which includes diminished value. While that might sound like a lot of time, it’s easy to let deadlines slip by when you’re juggling repairs and other responsibilities. Missing that window means you lose your right to recover any compensation.

Understanding the legal timeline is critical. Insurance companies are well aware of these deadlines and sometimes use delay tactics, hoping you’ll run out of time. This is where getting professional guidance can make all the difference. If you’re feeling overwhelmed or unsure about the process, it’s a good idea to contact an attorney who can manage your claim and ensure everything is filed correctly and on time.

How to Choose the Right Appraiser

Finding the right appraiser can feel like a big task, but it’s one of the most important steps in your diminished value claim. The quality of your appraisal report can make or break your case with the insurance company. A thorough, well-researched report from a credible professional carries a lot of weight. Think of it as choosing the right expert witness for your case. To help you find a qualified appraiser who will give your claim the best chance of success, here are a few key things to look for and some red flags to avoid.

Check for proper certifications

When you start your search, the first thing to check is an appraiser’s credentials. A certified appraiser with a valid state license isn’t just a nice-to-have; it’s a necessity. These certifications show that the appraiser has met specific industry standards and has the training to accurately assess your vehicle’s diminished value. An uncertified opinion is just that, an opinion, and it’s easy for an insurance adjuster to dismiss. Don’t be shy about asking potential appraisers about their qualifications. A true professional will be happy to share their credentials with you.

Verify their experience and read reviews

Credentials tell part of the story, but experience tells the rest. You want an appraiser who has a solid track record, especially with vehicles like yours. If you drive a luxury car, a classic, or an electric vehicle, find someone who specializes in that area. The best way to gauge experience is to read online reviews and ask for references. See what past clients have to say about their professionalism, the quality of their reports, and their success rate with insurance companies. A little bit of research upfront can save you a lot of headaches later. If you’re unsure where to start, you can always contact us for guidance.

Red flags to watch out for

As you compare your options, keep an eye out for a few common red flags. Be cautious of any appraiser who promises an unusually high payout before they’ve even seen your vehicle. This is often a tactic to get you to buy their report, which may not hold up under scrutiny. On the flip side, be wary of extremely cheap, automated reports. These are often generated by software without a physical inspection and lack the detail and authority needed to challenge an insurance company. A credible appraisal takes time and expertise, and the price should reflect that. Choosing the right expert is a key part of our legal services.

When to Get Legal Help With Your Claim

Getting a professional appraisal is a huge step toward getting the money you’re owed. But what happens when the insurance company ignores your report or comes back with another lowball offer? Sometimes, even with solid proof, insurers refuse to pay a fair amount. This is often when having a legal expert on your side becomes essential. An attorney who specializes in property damage can manage the difficult negotiations and fight for the compensation you deserve, especially when the insurance adjuster is unresponsive or dismissive. In these situations, an experienced Atlanta diminished value attorney can use your appraisal report to strengthen negotiations and pursue a fair resolution.

Dealing with an insurance company can feel like a full-time job, and it’s easy to feel overwhelmed. If you’ve presented a detailed appraisal and the insurer still won’t offer a fair settlement, it’s probably time to seek legal advice. An attorney can cut through the red tape and show the insurance company you’re serious about your claim.

Know when to call a lawyer

It’s frustrating when you’ve done everything right and still hit a wall. You should consider calling a lawyer if the insurance company’s offer doesn’t come close to your appraiser’s valuation, or if they’re using confusing tactics to delay your payment. If the adjuster dismisses your evidence without a clear explanation or simply stops responding to your calls and emails, that’s a major red flag. A lawyer can help you understand the true diminished value of your vehicle and determine if the insurer is acting in bad faith. Don’t let them wear you down; getting professional help can reset the conversation.

How a lawyer can strengthen your claim

Hiring an attorney does more than just show the insurance company you mean business; it levels the playing field. Insurance companies have teams of lawyers working for them, and you should have an expert in your corner, too. An experienced lawyer understands Georgia law and the specific language in insurance policies. They can review your appraisal and all communication to build a powerful case. Our team handles all the negotiations, paperwork, and legal hurdles, so you don’t have to. Our legal services are designed to make the process smoother and significantly increase your chances of receiving the full compensation you’re entitled to.

Related Articles

- Diminished Value – Gastley Law

- Diminished Value Appraisal: A Step-by-Step Guide

- Maximize Your Car Accident Diminished Value Settlement

Frequently Asked Questions

Can I just use a free online calculator for my diminished value?

While online calculators can give you a rough idea, they won’t hold up against an insurance company. These tools use simple algorithms and can’t account for the specifics of your vehicle, the quality of the repairs, or local market conditions. An insurance adjuster can easily dismiss a number from a website. A professional appraisal, on the other hand, is a detailed, evidence-based report created by a certified expert after a physical inspection, which gives your claim the credibility it needs.

My car looks and drives like new after the repairs. Do I still have a claim?

Yes, most likely. The core of a diminished value claim isn’t about how the car looks or performs post-repair; it’s about its permanent accident history. When you go to sell your car, its vehicle history report will show it has been in a wreck. This history makes it less attractive to potential buyers, forcing you to sell it at a lower price than a similar car with a clean record. That financial loss is what you are entitled to recover.

Is there a minimum amount of damage that makes an appraisal worthwhile?

There isn’t a strict rule, but it’s a matter of weighing the cost against the potential return. If your car only had minor cosmetic damage, like a few paint scratches, the loss in value might be less than the cost of the appraisal itself. However, if your vehicle sustained structural damage, had frame repairs, or required major component replacement, the diminished value is likely significant. In those cases, investing a few hundred dollars in an appraisal can help you recover thousands.

What if the at-fault driver’s insurance company offers to do their own appraisal?

You should be cautious. An appraiser hired by the insurance company works for them, and their goal is often to find the lowest possible value to minimize the payout. It’s always best to get an independent appraisal from an unbiased expert who is working for you. Your own appraisal provides a credible, third-party valuation that you can use as a powerful negotiation tool to counter the insurer’s low offer.

What’s my next step if the insurance company rejects my professional appraisal?

This is a common tactic insurers use to discourage claimants. If you’ve submitted a comprehensive report from a certified appraiser and the insurance company still refuses to offer a fair settlement, it’s time to consider legal help. An attorney who specializes in property damage claims can step in, manage all communication, and show the insurer you are serious about getting the compensation you are legally owed.