What Is an Appraisal Clause in Insurance? A Guide

It’s one of the most frustrating parts of a property damage claim: the insurance company agrees the damage is covered, but their offer to fix it is far too low. You have estimates from reputable body shops, but the adjuster won’t budge. This is precisely the scenario the appraisal clause insurance policies contain was designed to solve. This clause isn’t about fighting over coverage; it’s about settling a disagreement over money. It creates a formal process where neutral experts are brought in to determine the true cost of your damages. It’s a powerful right you have as a policyholder, but using it effectively requires knowing the rules, the costs, and the potential outcomes. This guide will walk you through what you need to know.

Key Takeaways

- Settle value disputes, not coverage denials: The appraisal clause is your tool for challenging the dollar amount of an insurer’s offer, like for repair costs or diminished value. It cannot, however, force an insurer to cover a claim they have already denied.

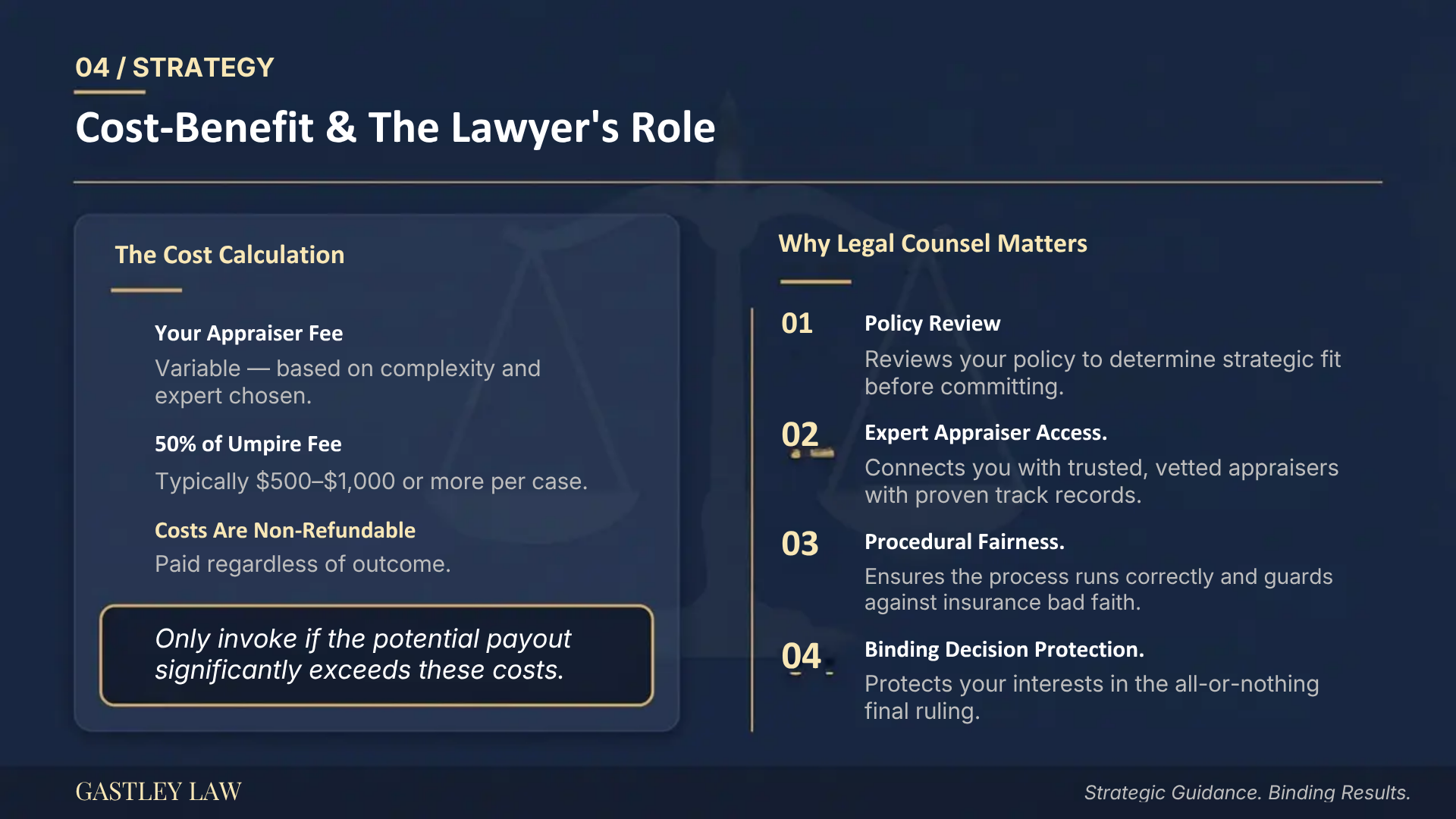

- Weigh the costs against the potential gain: Invoking the appraisal clause isn’t free; you pay for your appraiser and half of the umpire’s fee. Make sure the difference between the insurer’s offer and what you’re owed is significant enough to justify these upfront expenses.

- Get legal advice before you start: The appraisal process is binding and has specific rules. Consulting with an attorney first helps you determine if it’s the right strategy, connect with a qualified appraiser, and build the strongest possible case for your claim.

What Is an Appraisal Clause in an Insurance Policy?

After a car accident, you expect your insurance company to make things right. But what happens when their offer for repairs or your car’s lost value feels completely unfair? It can feel like you have no choice but to accept their lowball number. Tucked away in your policy documents, however, is a powerful tool you might not even know you have: the appraisal clause.

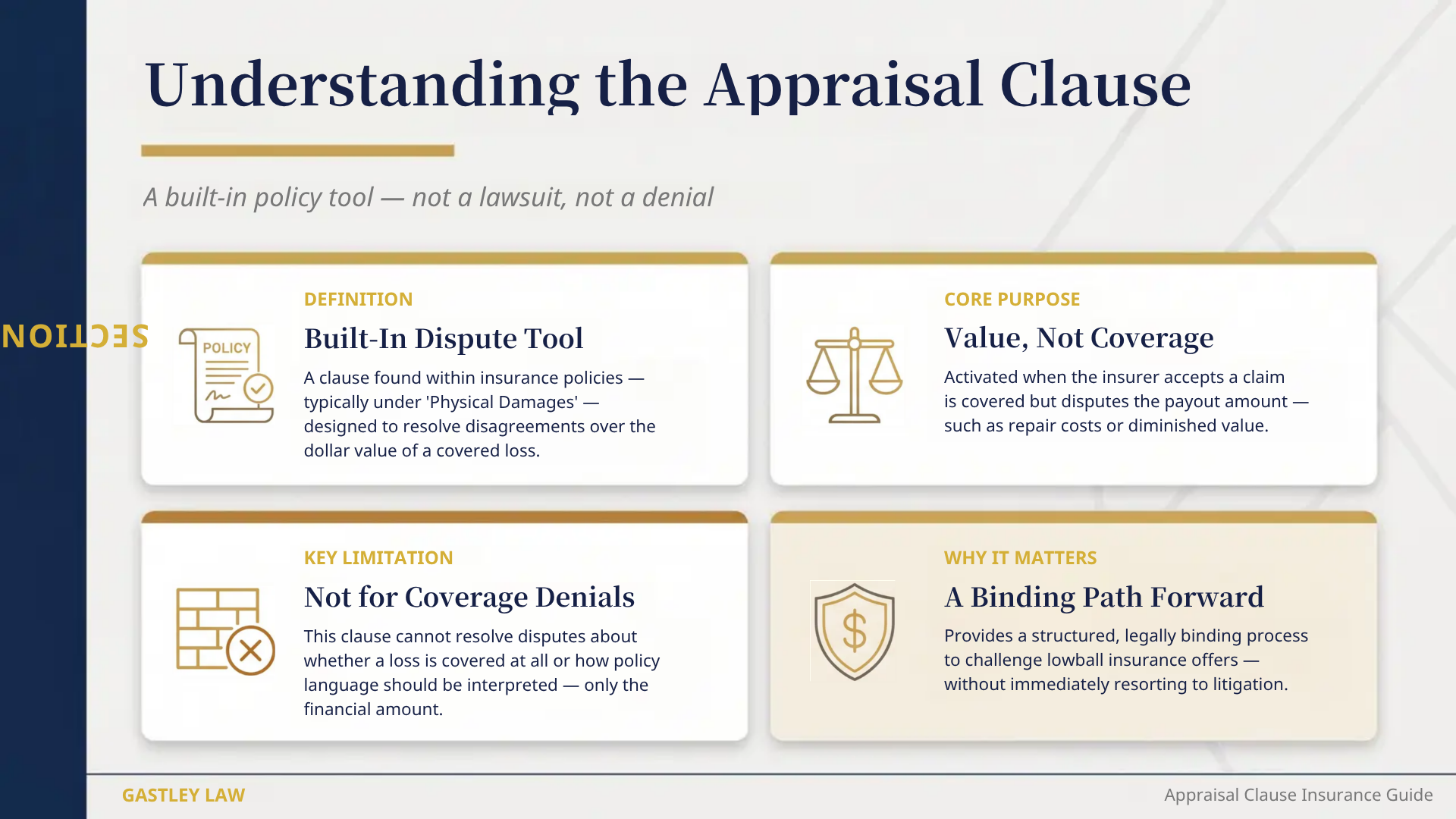

This clause outlines a formal process for resolving disagreements about the amount of your loss. It’s not for arguing about whether your policy covers the damage, but for settling disputes over the dollar amount. Invoking this clause can be a strategic way to challenge the insurance company’s valuation and get an independent assessment of what you’re truly owed. Understanding how it works is the first step toward ensuring you get a fair payout.

What It Is and Why It Matters

Think of the appraisal clause as a built-in dispute resolution tool. It’s a provision in your policy that you and your insurance company can use when you agree that a loss is covered but can’t agree on how much that loss is worth. This is especially important when you’re making a claim for your vehicle’s diminished value, which is the loss in market value your car suffers after being in an accident. The appraisal clause matters because it gives you a clear, structured path to challenge an insurer’s low offer without immediately resorting to a lawsuit. It levels the playing field by bringing in neutral experts to value the damage.

Where You’ll Find This Clause

Ready to find this clause in your own policy? You’ll typically find it in the “Physical Damages” section of your auto insurance documents. This is the part of your policy that details your Comprehensive and Collision coverage, which pays for damage to your own vehicle. The wording can vary slightly from one company to another, but it will lay out the specific steps for initiating the appraisal process. Taking a few minutes to locate and read this section will help you understand your rights and the procedures your insurer is required to follow if you decide to dispute their valuation of your claim.

Appraisal vs. Other Dispute Options

When you disagree with your insurer, it might seem like your only option is a lengthy and expensive court battle. The appraisal process, however, offers a different route. It’s generally faster, more informal, and less costly than litigation. The decision reached through appraisal is also binding, meaning there are no appeals.

However, it’s crucial to know its limitations. Appraisal is strictly for resolving disagreements over the amount of the loss. If your dispute is about whether your policy covers the damage at all, or if you disagree on how to interpret the policy’s language, appraisal isn’t the right tool. In those cases, you may need different kinds of legal representation to resolve the issue.

How Does the Insurance Appraisal Process Work?

When you and your insurance company are at a standstill over the cost of your vehicle’s damages, the appraisal clause in your policy offers a path forward. It’s a formal process designed to bring in neutral experts to determine the true value of your loss. Think of it as a structured negotiation with a clear set of rules. While it might sound complicated, breaking it down step-by-step makes it much easier to understand. Here’s a look at how the process typically unfolds.

Step 1: Start the Process

The first move is yours. To get the ball rolling, you need to formally notify your insurer that you want to invoke the appraisal clause in your policy. This is usually done in writing. It’s a clear signal that you dispute their valuation and are ready to bring in experts to get a fair assessment. This isn’t an aggressive tactic; it’s simply you exercising a right outlined in your insurance contract. If you’re unsure how to word this request or where to send it, getting some guidance can ensure you start the process correctly from day one.

Step 2: Choose Qualified Appraisers

Once the process is initiated, both you and the insurance company will select your own independent appraiser. It’s crucial to choose someone who is competent, impartial, and an expert in assessing vehicle damage and value. This isn’t the time to pick a friend who knows a bit about cars. You need a professional who can build a strong, evidence-based case for the true cost of your repairs and your vehicle’s diminished value. The insurer will certainly choose an expert to represent their interests, so you need an equally qualified professional on your side.

Step 3: Agree on a Neutral Umpire

What happens if the two appraisers can’t see eye to eye? This is where the umpire comes in. The two appraisers will select a neutral, third-party umpire to act as a tie-breaker. This person must be agreed upon by both sides. The umpire reviews the findings from both appraisers and helps them reach a resolution. Their role is to provide an objective perspective and ensure the final decision is fair. If the appraisers can’t agree on an umpire, sometimes a court is asked to appoint one.

Step 4: Receive a Final Decision

The goal of the appraisal is to arrive at a binding decision on the amount of your loss. This final number is determined when any two of the three parties (your appraiser and the insurer’s appraiser, or one appraiser and the umpire) come to an agreement. Once they sign off on a value, that amount is final. It’s important to remember that this process only settles disagreements over the dollar amount of the damage. It doesn’t determine whether your policy covers the claim in the first place.

Breaking Down the Costs and Timeline

It’s important to understand the costs involved before you begin. You are responsible for paying for your own appraiser, and the insurance company pays for theirs. The cost of the neutral umpire, along with any other administrative expenses, is split evenly between you and the insurer. The timeline can vary quite a bit, depending on how long it takes to select the appraisers and umpire and the complexity of your claim. Our firm can help you understand these potential costs and timelines as part of our legal services.

Common Myths About the Appraisal Clause

The appraisal clause can seem like a simple fix when you and your insurer are at a standstill. But there’s a lot of misinformation floating around that can lead you down the wrong path. Believing these myths can cost you time, money, and a whole lot of frustration. Before you decide to invoke this clause, it’s important to separate fact from fiction. Let’s clear up some of the most common misconceptions so you can make a smart, informed decision about your property damage claim.

Myth: Appraisal Decides If Your Claim Is Covered

This is one of the biggest misunderstandings about the appraisal process. Many people believe that starting an appraisal will force the insurance company to accept and pay their claim. In reality, the appraisal clause is only used when both sides already agree that the damage is covered by the policy. The disagreement is strictly about the dollar amount. If your insurer has denied your claim entirely, appraisal isn’t the right tool. It’s designed to settle disputes over the value of a loss, not whether the loss should be covered at all.

Myth: The Winner Gets Their Costs Covered

It would be great if the losing party had to cover the costs, but that’s not how it works. When you enter the appraisal process, you are responsible for paying your own appraiser’s fee. You also have to split the cost of the neutral umpire with the insurance company. These expenses are paid out of your own pocket, and they are not reimbursed, even if the final award is much higher than the insurer’s initial offer. You have to carefully consider if the potential increase in your settlement is enough to justify these upfront, non-refundable costs.

Myth: The Umpire Is Always Unbiased

Ideally, every umpire would be a completely neutral third party. In practice, finding someone who is both experienced and truly impartial can be difficult. Some umpires may have existing professional relationships with insurance companies, which could potentially influence their judgment, even unintentionally. This is why it’s so important to have an expert on your side who knows the industry and can help vet and select a genuinely neutral umpire. An experienced property damage attorney can be a huge asset in making sure the process is fair.

Myth: Appraisal Solves Every Disagreement

The appraisal clause has a very narrow and specific purpose: to determine the financial amount of your loss. That’s its only job. It does not resolve disagreements about who was at fault for an accident (liability), what your policy covers, or any other disputes you might have. For instance, if the insurance company argues that some of your car’s damage was pre-existing and not covered, the appraisal process can’t overrule them. It only sets a price on the damages that are mutually agreed upon as being covered by the policy.

What an Appraisal Can (and Can’t) Do

So, let’s recap. An appraisal can be an effective way to break a deadlock with your insurer over repair costs or the diminished value of your vehicle. Once two of the three participants (your appraiser, the insurer’s appraiser, and the umpire) agree on a value, that decision is binding for both you and the insurance company. On the other hand, an appraisal can’t force an insurer to cover a denied claim, establish fault, or settle other policy-related arguments. It’s a specific solution for a very specific problem: a disagreement over money.

Should You Use Your Appraisal Clause?

Deciding whether to invoke the appraisal clause is a strategic move that depends entirely on your situation. It’s a powerful tool when used correctly, but it isn’t the right solution for every disagreement with your insurance company. Before you make the call, it’s important to understand when appraisal works best and when another path might be better for securing the compensation you deserve.

Think of it as a fork in the road. One path leads to a binding decision on the value of your damages, while the other might involve more direct negotiation or legal action. Let’s walk through the key factors to help you choose the right direction for your claim.

Signs Your Insurer’s Offer Is Too Low

The most common reason to consider appraisal is a lowball offer from your insurer. If you’ve done your research, gathered repair estimates, and believe the insurance company’s offer won’t cover your actual losses, the appraisal clause gives you a formal way to challenge their number. Insurance companies sometimes offer less than a property loss is truly worth, especially when it comes to complex claims like diminished value. When the gap between their offer and your expected repair costs is significant, and they refuse to negotiate in good faith, invoking appraisal can break the stalemate and bring in neutral experts to assess the damage.

When You Only Disagree on the Repair Cost

The appraisal process is designed for one specific type of conflict: when you and your insurer agree the damage is covered, but you can’t agree on the price tag. For example, if your policy clearly covers collision damage, but your insurer’s estimate for repairs is thousands less than what your body shop quoted, appraisal is the perfect tool. It’s meant to settle disputes over the dollar amount of the loss. However, if the insurance company is denying your claim entirely or arguing that your policy doesn’t cover the specific type of damage, appraisal won’t help. It’s a process for valuation, not for interpreting policy language.

Weighing the Costs vs. the Potential Payout

Invoking the appraisal clause isn’t free, so you need to do a quick cost-benefit analysis. You are responsible for paying for your own appraiser, and you’ll also have to split the cost of the neutral umpire with the insurance company. These fees can add up, often costing between $500 and $1,000 or more, and they are not refundable, even if the final decision is in your favor. You have to ask yourself if the difference between the insurer’s offer and what you believe you’re owed is large enough to justify these upfront costs. If you’re fighting over a few hundred dollars, the expense of appraisal might not be worth it.

When Appraisal Might Not Be Your Best Move

Appraisal is the wrong tool if your disagreement is about what your policy actually covers. If the dispute is over the meaning of your policy’s terms or how its rules apply, appraisal can’t resolve it. This type of conflict requires legal interpretation, not just a damage valuation. Furthermore, the outcome rests in the hands of an umpire who makes the final call, and there are few rules governing who can serve in this role. If you’re facing a claim denial or a complex coverage issue, you’re better off exploring other options. In these situations, it’s wise to get legal advice before committing to a process that may not address the core of your problem.

How a Lawyer Protects Your Interests During Appraisal

The appraisal process might seem like a simple way to settle a dispute, but it’s full of complexities that can trip you up. An experienced attorney does more than just offer advice; they act as your advocate and strategist. They ensure the process is fair, your appraiser is qualified, and your claim is presented in the strongest way possible. Having a legal expert on your side from the beginning can make all the difference between accepting a low offer and getting the compensation you truly deserve.

Why You Should Get Legal Advice First

Before you even think about invoking the appraisal clause, it’s wise to talk to a lawyer. The appraisal process isn’t the right solution for every disagreement. An attorney can review your policy, the insurer’s offer, and the specifics of your vehicle’s damage to determine if appraisal is your best strategic move. Sometimes, negotiation or another form of dispute resolution might be more effective. Getting this guidance upfront prevents you from committing to a process that might not be in your best interest. A quick consultation can clarify your options and set you on the right path from day one.

Select the Right People for the Job

Your case is only as strong as the appraiser you choose. You need someone who is not just a mechanic, but an expert in vehicle valuation, insurance policies, and the appraisal process itself. They must be able to build a detailed, evidence-based report and negotiate effectively with the insurance company’s appraiser. Finding a professional with this specific skill set can be challenging. A property damage lawyer will have a network of trusted, independent appraisers who have a proven track record of securing fair outcomes for clients. This connection ensures you have a true expert fighting for you.

Fight for the Full Value of Your Claim

The goal of an appraisal is to get you the money you’re owed, but the process itself has costs. You have to pay for your appraiser, and if an agreement can’t be reached, you’ll also have to split the cost of a neutral umpire. These expenses are not reimbursed, even if you win. A lawyer helps you fight for the full value of your claim by ensuring your appraiser has all the necessary documentation to build an undeniable case. Their involvement puts pressure on the insurance company to be reasonable, increasing the chances of a fair settlement without needing a costly umpire.

What to Do if You Disagree with the Outcome

Once the appraisers (and umpire, if needed) make a decision, that number is almost always final and legally binding. There are very few grounds to challenge an appraisal award after the fact. This is why having legal representation from the start is so critical. An attorney ensures the process is followed correctly and that your claim is presented persuasively from the beginning. If you end up with an outcome you believe is unfair, your lawyer can review the proceedings for any procedural errors or signs of bad faith from the insurer, but your legal options become much more limited once the award is signed.

Related Articles

Frequently Asked Questions

Can I handle the appraisal process myself without a lawyer?

While you technically can initiate the appraisal process on your own, it’s a bit like performing your own car repairs without being a mechanic. You might get it done, but you risk missing crucial steps. An attorney ensures the process is followed correctly, helps you select a truly qualified and impartial appraiser, and makes sure your claim is presented in the strongest possible light. Having a professional guide you protects your interests against the insurance company’s experienced team.

Is the appraisal award the final check I’ll receive?

Not exactly. The appraisal award determines the total amount of your loss. From that amount, or out of your own pocket, you are still responsible for paying your appraiser’s fee and your half of the umpire’s fee if one was needed. Think of the award as the gross settlement amount before your expenses for the process are deducted.

What happens if my insurance company ignores my request for an appraisal?

Because the appraisal clause is part of the insurance contract you both agreed to, your insurer is generally obligated to participate if your dispute meets the criteria. If they refuse to respond or try to deny your right to an appraisal, it could be a sign of bad faith. This is a critical moment where you should seek legal advice immediately to understand how to enforce your policy rights.

Can I use the appraisal clause for a diminished value claim?

Yes, absolutely. A diminished value claim is a perfect example of when to use the appraisal clause. You and the insurer likely agree that the accident caused a loss in your car’s market value, but you disagree on the dollar amount of that loss. The appraisal process is designed specifically to resolve these kinds of valuation disputes.

How do I find a qualified appraiser for my car?

Finding the right appraiser is key to a successful outcome. You should look for an independent professional who specializes in vehicle valuation and has direct experience with the insurance appraisal process, not just a local mechanic. A good property damage attorney will have a network of vetted, competent appraisers they trust to handle these specific types of claims.