Property Damage Demand Letter: A Step-by-Step Guide

Dealing with an insurance company after a car accident can feel like a full-time job you never wanted. You’ve made the phone calls, sent the photos, and now you’re stuck in a frustrating loop with an adjuster who seems determined to delay, deny, or lowball your claim. If you’re tired of feeling powerless, it’s time to make a move that they can’t ignore. A formal property damage demand letter is your most effective tool for cutting through the red tape. It shifts the conversation from casual phone calls to a serious, documented negotiation, showing the insurer you have a well-supported case and are prepared to fight for what you’re owed. This guide will walk you through how to write one that gets results.

Key Takeaways

- A strong demand letter starts with solid proof: Gather all your repair estimates, photos of the damage, and receipts for related expenses before you begin writing to build a compelling and undeniable case from the start.

- Professionalism gets results: Structure your letter clearly by telling a factual story of the incident, providing an itemized list of your costs, and setting a firm deadline for the insurance company to respond.

- Calculate your full damages and know when to get help: Your demand should include every single cost, especially your car’s diminished value. If the insurer makes a lowball offer or uses delay tactics, seeking legal help can level the playing field.

What Is a Property Damage Demand Letter?

Think of a property damage demand letter as your official, written request for compensation after your car has been damaged. It’s a formal document you send to the at-fault party’s insurance company, clearly stating what happened, the damage done to your vehicle, and exactly how much money you need to make things right. This isn’t just a simple note; it’s a structured argument for your case. You’ll include crucial evidence like repair estimates from trusted body shops, photos of the damage, and a copy of the police report if there is one.

Sending this letter is a powerful first step in the formal claims process. It puts the insurance company on notice that you are organized, serious, and fully aware of what you’re owed. It moves the conversation beyond casual phone calls with an adjuster and establishes a formal record of your claim. By presenting all the facts and figures in a professional format, you set the stage for a successful negotiation. This is a core part of the legal representation we provide, ensuring your claim is taken seriously from the very beginning.

Why It’s So Important

So, why go to the trouble of writing a formal letter? Because it works. A well-crafted demand letter shows the insurance company that you mean business. It proves you’ve done your homework and have the evidence to back up your claim. This single document can significantly increase your chances of getting a fair settlement without ever stepping into a courtroom. It also creates an official paper trail, which is incredibly valuable if the insurer continues to be difficult. Essentially, it gives them a clear chance to do the right thing before you take further legal action, especially when it comes to recovering the full diminished value of your car.

When to Send One

Timing is everything. You should send a demand letter after you have all your ducks in a row. This means you’ve collected repair estimates, documented all the damage with photos, and have a clear understanding of your total losses. It’s the perfect next step if the insurance adjuster is giving you the runaround, has made a lowball offer, or is dragging their feet. Sending the letter shows that you’re moving the process forward proactively. If you’ve reached a point where you feel stuck and aren’t getting a fair response, that’s your cue. It’s often at this stage that people decide to contact us for guidance.

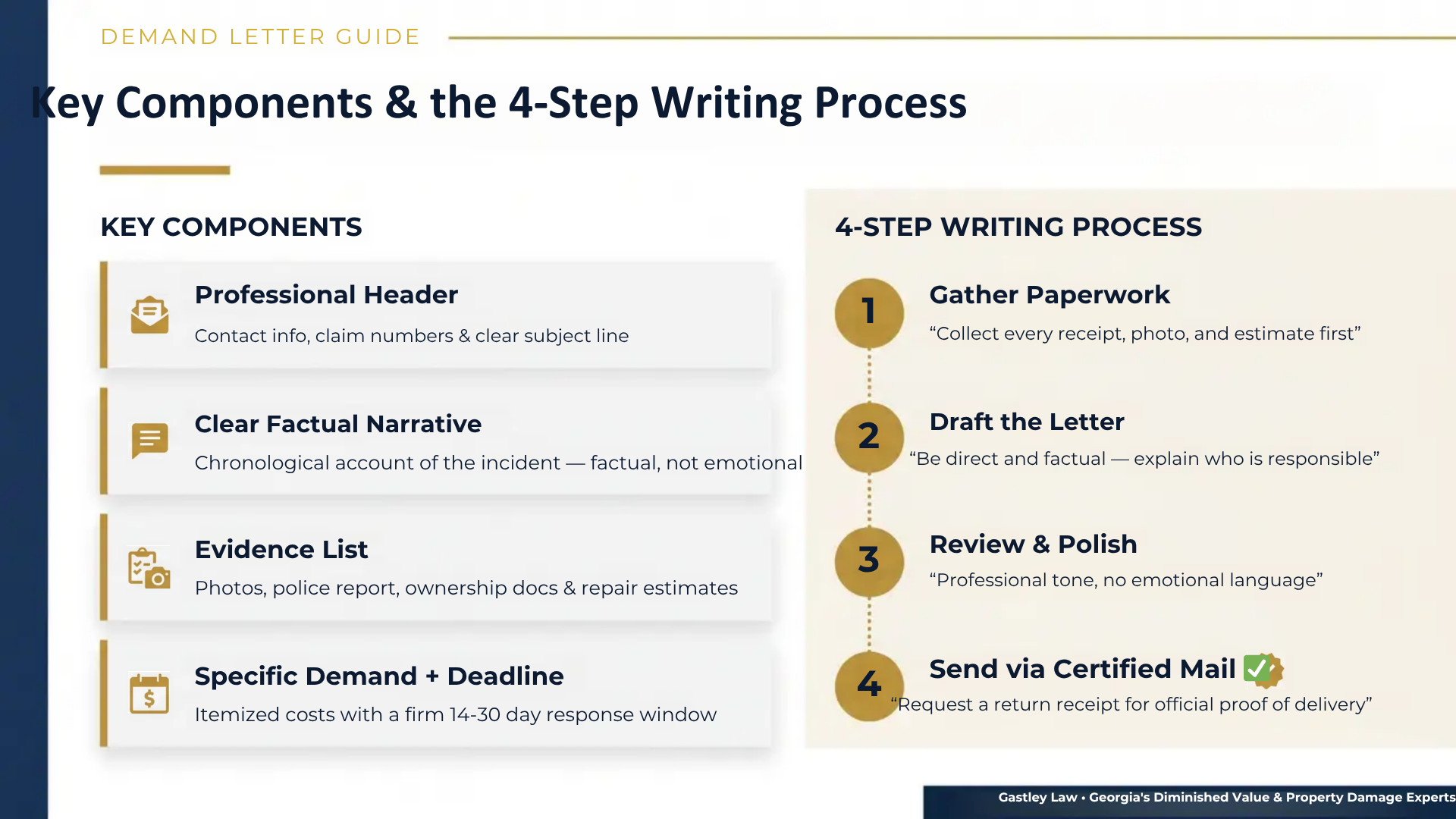

What to Include in Your Demand Letter

Think of your demand letter as the foundation of your property damage claim. A strong, well-organized letter shows the insurance company that you’re serious and have a solid case. It’s your first real opportunity to lay out the facts, present your evidence, and clearly state what you need to make things right. Getting the details correct from the start can make the entire process smoother and more effective. When you include all the necessary components, you leave less room for the insurer to question or delay your claim. Each piece of information builds upon the last, creating a comprehensive picture of what happened and what it will take to fix it.

Contact Information for Everyone Involved

First things first, you need to make it clear who is involved. This might sound basic, but missing or incorrect contact information can cause unnecessary delays. Your letter should clearly list your full name, address, phone number, and email. You also need to include the same information for the at-fault driver, if applicable, along with their insurance policy number and claim number. Providing all of this upfront makes it easy for the insurance adjuster to process your file and know exactly who to contact. It sets a professional tone and shows that you are organized and prepared to handle the claim efficiently.

A Clear Description of the Incident

Next, you need to explain exactly what happened. Write a clear, factual summary of the accident. Be sure to include the date, time, and specific location where the damage occurred. Describe the events in chronological order, sticking to the facts and avoiding overly emotional language. For example, instead of saying “the other driver recklessly slammed into me,” you could write, “the other vehicle failed to stop at the red light and collided with the passenger side of my car.” A straightforward, objective account of the incident helps the adjuster quickly understand the situation and establish liability without getting bogged down in dramatic details.

Proof of Ownership

To make a claim for your damaged vehicle, you have to prove that you actually own it. This is a simple but essential step that confirms your legal standing to seek compensation. The insurance company needs this documentation for their records to verify that they are dealing with the rightful owner of the property. Including a copy of your vehicle’s title or registration with your demand letter is the easiest way to do this. It’s a small piece of paperwork that prevents any potential questions about your ownership, helping to keep your claim moving forward without a hitch.

Evidence of the Damage

This is where you show the insurance company the extent of the damage. Your description is important, but photos and official reports provide undeniable proof. Take clear, well-lit pictures of your vehicle from every angle, making sure to get close-ups of the specific areas that were damaged. If a police report was filed at the scene of the accident, include a copy. The officer’s official report serves as an unbiased account of the incident and often includes a diagram and initial assessment of the damage. This evidence is crucial for building a strong case and justifying the amount you are demanding for repairs.

Repair Estimates and Other Costs

Finally, you need to spell out the financial impact of the accident. This is the core of your demand. Get at least one, but preferably two, detailed repair estimates from reputable auto body shops. These estimates should itemize the costs for parts and labor. Beyond repairs, include any other expenses you’ve incurred because of the accident, such as towing fees or the cost of a rental car. This is also where you’ll want to address your vehicle’s diminished value, which is the loss in resale value your car suffers even after being repaired. Tallying up all these costs gives you the total amount you will demand in your letter.

How to Structure Your Demand Letter for Impact

Think of your demand letter as a business proposal. The way you organize it can make the difference between a quick, fair settlement and a long, drawn-out fight. A messy, confusing letter is easy for an insurance adjuster to set aside, but a clear, professional, and well-structured document commands attention. It shows you’re organized, serious, and have a solid grasp of your claim’s details. By following a logical structure, you make it easy for the adjuster to understand the facts, review your evidence, and see exactly what you’re asking for. This simple step sets a professional tone from the very beginning and puts you in a much stronger position.

Start with a Professional Header

First things first, you need a clean and professional header. This isn’t just about looking official; it’s about making the adjuster’s job easier. Include your full name, address, and phone number. Below that, add the date. Then, include the insurance adjuster’s name (if you have it), their title, and the insurance company’s address. Finally, add a clear and concise subject line, like “RE: Demand for Property Damage Compensation; Claim Number: [Your Claim Number].” This immediately tells the recipient what the letter is about and helps them locate your file quickly. A proper header ensures your letter gets to the right person and is taken seriously from the moment it lands on their desk.

Tell the Story Clearly

This is where you explain what happened. Your goal is to present a clear, factual, and easy-to-follow narrative of the incident. Write chronologically and stick to the facts. Avoid emotional language or angry accusations, as this can make you seem less credible. Start with the date, time, and location of the incident. Describe exactly what happened, step by step, and clearly explain why the other party is responsible for the damages. Think of it as telling a simple story to someone who knows nothing about the situation. The easier you make it for the adjuster to understand the events, the smoother the process will be.

Present Your Evidence

After telling your story, it’s time to back it up with proof. This section is where you methodically list all the evidence you’ve gathered to support your claim. A well-supported claim is much harder for an insurance company to dispute. You should reference the documents and photos you’re including with the letter, such as copies of the police report, photographs of the damage from multiple angles, and written repair estimates from reputable shops. If your vehicle suffered a significant loss in resale value, you should also include documentation supporting your diminished value claim. Listing your evidence clearly shows the adjuster that you’ve done your homework and have a strong case.

State Exactly What You’re Asking For

This is the most important part of your letter: the demand itself. Don’t be vague. You need to state the exact dollar amount you are seeking as compensation. Create an itemized list that breaks down this total figure. For example, list the cost of repairs, the cost of a rental car, and the amount of diminished value separately. Then, provide the final sum you are demanding. Outlining the facts and specifying a desired remedy makes your request clear and actionable. Calculating these costs accurately can be challenging, which is where professional legal representation can be invaluable in ensuring you ask for what you truly deserve.

Set a Deadline for Their Response

To prevent your claim from getting lost in a pile of paperwork, you need to create a sense of urgency. End your letter by stating a reasonable deadline for the insurance company to respond. A period of 14 to 30 days is typical. Politely state that if you do not receive a response or a fair settlement offer by that date, you will be forced to consider your legal options. This shows the adjuster that you are serious about resolving the matter in a timely fashion. If that deadline comes and goes without a satisfactory answer, it may be the right time to contact our team to discuss the next steps.

A Step-by-Step Guide to Writing Your Letter

Writing a demand letter can feel intimidating, but it’s really just about laying out the facts clearly and professionally. Think of it as telling the story of what happened and what you need to make it right. By following these steps, you can create a strong letter that gets the insurance company’s attention and sets the stage for a fair resolution. Let’s walk through it together.

Step 1: Gather All Your Paperwork

Before you write a single word, you need to get organized. Think of this as building the foundation for your claim; the stronger your evidence, the more solid your case will be. Make sure you have gathered all your repair estimates, photos of the damage from multiple angles, a copy of the police report, and any receipts for related expenses like a rental car. Having all this documentation in front of you makes writing the letter much easier and ensures you don’t forget any crucial details that support your claim for property damage and diminished value.

Step 2: Draft the Letter

Now it’s time to start writing. A property damage demand letter is a formal request for the at-fault party or their insurer to pay for the damage to your vehicle. Start by clearly describing what property was damaged, where and when the incident happened, and how it occurred. You’ll need to explain why the other party is responsible for the damages. Be direct and stick to the facts. Remember to mention that you are attaching copies of your evidence, like photos, repair estimates, and the police report, to back up everything you’re saying.

Step 3: Review and Polish Your Draft

Once you have a draft, take a moment to review it. A well-written demand letter makes your case clear and convincing, which greatly increases your chances of getting paid. Read it out loud to catch any awkward phrasing and check for any spelling or grammar mistakes. Is your tone firm but professional? Is it easy to understand exactly what happened and what you’re asking for? After you’ve polished it, make copies of everything. Keep a copy of the final letter, all the evidence you attached, and your delivery records in a safe place.

Step 4: Send It Correctly

How you send the letter is almost as important as what’s in it. Use certified mail with a return receipt requested. This gives you official proof that the letter was sent and, more importantly, that it was received by the insurance company. This small step prevents them from ever claiming they didn’t get your demand. In your letter, be sure to give the other party a clear and reasonable date to respond by, such as 14 or 30 days. This establishes a timeline and shows you’re serious about resolving the issue. If that deadline passes without a fair response, it may be time to seek professional help with your property damage claim.

How Much Money Should You Ask For?

This is the part of the letter where you get down to business: the money. Deciding on a number can feel intimidating, but it’s not a guessing game. Your demand should be a carefully calculated figure that covers every single loss you’ve experienced because of the accident. Think of it as building a case with numbers. You need to account for the obvious repairs, the less obvious expenses, and the long-term loss in your car’s value. A strong, well-supported number shows the insurance company that you’ve done your homework and you’re serious about getting what you’re owed.

Calculate Repair and Replacement Costs

Your starting point is the cost to fix your car. Don’t just get one quote; aim for at least two or three detailed estimates from reputable, licensed repair shops. These estimates should break down the costs for parts and labor. This isn’t just about getting a total; it’s about showing the adjuster exactly what needs to be fixed and why it costs what it does. And don’t forget about diminished value, which is the loss in your car’s resale value even after it’s been perfectly repaired. This is a real, compensable loss that should absolutely be part of your calculation.

Add Other Related Expenses

The damage from an accident often goes beyond the vehicle itself. Did you have to rent a car while yours was in the shop? Add that cost. Did you pay for towing? Include the receipt. You might have even lost wages from taking time off work to deal with the accident’s aftermath, like meeting with adjusters or taking your car to the shop. Make a comprehensive, itemized list of every single expense you’ve incurred as a direct result of the incident. Keeping meticulous records and receipts for everything will make this part much easier and strengthens your claim significantly.

Settle on a Fair Number

Once you’ve tallied up all your costs, it’s time to land on your final demand amount. It’s wise to ask for a figure that is fair but also leaves a little room for negotiation, as the insurance company will almost certainly come back with a lower counteroffer. Your initial demand sets the tone for the entire negotiation. By presenting a number backed by detailed estimates and receipts, you’re not just asking for money; you’re demonstrating the true value of your claim. If you’re feeling unsure about what a fair number looks like, it might be time to get some professional advice.

What to Expect After You Send Your Letter

Sending your demand letter is a huge step, but the process isn’t over yet. Now, you enter a phase of waiting and, most likely, negotiating. The insurance company’s response can vary widely, so it’s smart to prepare for a few different scenarios. Staying organized and level-headed during this stage is key to getting the fair compensation you deserve for your property damage. Here’s a breakdown of what you can expect and how to handle each step.

How Long Until You Hear Back?

After you send your letter, the ball is in the insurance adjuster’s court. Their response will likely be one of five things: they agree to pay your demanded amount (this is rare), they make a counteroffer, they ask for more information, they deny your claim entirely, or they don’t respond at all. If you don’t hear anything by the deadline you set in your letter, it’s time to follow up. Don’t assume the worst, but be ready to be persistent.

How to Handle Counteroffers

It’s extremely common for an insurance company’s first offer to be a lowball number. Don’t get discouraged; this is just the start of the negotiation. Take a close look at their offer and compare it to your own calculations. If it’s too low, you can make a strategic counteroffer. Respond in writing, calmly explaining why their offer is insufficient and referencing the evidence you’ve already provided. A key part of this is understanding the full diminished value of your vehicle, which is often where adjusters try to cut corners.

Smart Negotiation Tips

Negotiating with an insurance adjuster can feel intimidating, but you have more power than you think. The key is clear, professional communication. Keep meticulous records of every conversation, including the date, time, and what was discussed. Always refer back to your documentation, like repair estimates and photos, to support your points. Know your bottom line, the lowest amount you’re willing to accept, but don’t reveal it right away. If the adjuster is being difficult or using delay tactics, it might be a sign that you need professional help.

Following Up Professionally

If your deadline passes with no word, a polite follow-up is in order. A simple phone call or email to the adjuster to confirm they received your letter and to ask about the status of your claim is a great next step. This shows you’re serious without being aggressive. If they continue to ignore you or refuse to negotiate in good faith, you don’t have to keep fighting alone. At that point, it’s best to contact a lawyer who can take over communication and apply the legal pressure needed to get a fair result.

Common Mistakes That Can Hurt Your Claim

Writing a property damage demand letter can feel like a big step, and it is. But it’s also a place where simple missteps can unfortunately weaken your position. When you’re trying to get fair compensation for your vehicle, the last thing you want is for a preventable error to cost you money. Knowing what to watch out for can make a huge difference in how the insurance company responds to your claim. By avoiding these common mistakes, you present a stronger, more professional case from the very beginning, showing the insurer that you are serious about getting what you’re owed. Let’s walk through some of the most frequent slip-ups so you can steer clear of them and keep your claim on the right track.

Weak Evidence or Missing Documents

Think of your demand letter as the story of your claim, and your evidence as the proof that makes it believable. A letter without solid documentation is just a list of requests, but one with strong evidence is a compelling case. Insurance adjusters review countless claims, so a well-organized file with clear proof stands out. Before you write a single word, gather every piece of paper and every photo related to the incident. This includes repair estimates from reputable shops, clear photos of the damage from multiple angles, and a detailed list of all your losses. A strong claim also includes a diminished value report to show how the accident has reduced your car’s resale price, a loss that is often overlooked.

An Unprofessional or Emotional Tone

It’s completely understandable to feel angry or frustrated after your car has been damaged. The process can be stressful, and it’s easy to let those emotions spill into your writing. However, an emotional or accusatory tone can work against you. The goal is to be firm and professional, not aggressive. A letter filled with anger can make the adjuster less willing to cooperate and may signal that you’re not approaching the situation logically. To avoid this, try writing a first draft where you get all your feelings out. Then, step away for a day and come back to edit it with a clear head, focusing only on the facts. If you’re struggling to remain objective, having a lawyer handle the communication can be a smart move.

Bad Timing

When it comes to a property damage claim, timing is everything. On one hand, you shouldn’t rush to send a demand letter the day after the accident. You need time to fully assess the damage, get professional repair estimates, and understand the total financial impact. On the other hand, waiting too long can be just as harmful. Delaying can make it seem like your claim isn’t urgent, and you could even risk missing your state’s statute of limitations for filing a lawsuit. The best approach is to notify the insurance provider as soon as possible to get the process started. Then, send your formal demand letter once you have all your evidence collected but well before any legal deadlines are approaching. This shows the insurer you are organized, serious, and proactive.

When Is It Time to Hire a Lawyer?

While you can certainly write a property damage demand letter on your own, some situations call for professional backup. Think of it this way: you’re going up against an insurance company with a team of adjusters and lawyers whose job is to pay out as little as possible. Bringing in your own expert can level the playing field and take a huge amount of stress off your shoulders. If you feel overwhelmed, confused by the process, or suspect the insurance company isn’t treating you fairly, it’s probably time to consider legal help.

An experienced attorney knows exactly what to include in a demand letter, how to phrase your requests for maximum impact, and what evidence will make your case undeniable. They handle the back-and-forth with the adjuster, so you don’t have to. More importantly, the insurance company knows you’re serious when you have legal representation. This simple fact can often motivate them to offer a better settlement much faster. If your claim involves significant damage or you’re just not getting anywhere on your own, exploring legal representation is a smart next step to protect your interests and get the compensation you deserve.

Your Situation Is Complex

If your accident was more than a simple fender-bender, you might need a lawyer. A complex situation could involve multiple vehicles, unclear fault, or significant damage that affects your car’s long-term value. For these bigger cases, a lawyer can help make sure your letter is strong and follows all the necessary legal rules. They understand the nuances of Georgia law, including concepts like diminished value, which is the loss in your car’s resale value even after it’s been repaired. An attorney can build a compelling case that an insurance adjuster can’t easily dismiss, ensuring you account for every dollar you’re owed.

The Insurance Company Isn’t Playing Fair

Negotiating with insurance adjusters can be incredibly frustrating. If you’re getting the runaround, facing constant delays, or receiving a lowball offer that doesn’t even cover your repair estimates, it’s a clear sign you need help. An experienced Atlanta diminished value attorney can help challenge undervalued offers and pursue the full value of your property damage claim. Insurance companies sometimes use these tactics hoping you’ll get tired and accept an unfair settlement. When negotiations become difficult or the insurer refuses to offer a fair amount, professional assistance is your best bet. An attorney can step in, cut through the red tape, and show the insurance company that you won’t be pushed around. If you feel like you’ve hit a wall, it’s time to contact a professional who can fight for you.

Related Articles

Frequently Asked Questions

Why can’t I just handle this over the phone with the adjuster?

While phone calls are a part of the process, a formal demand letter is crucial because it creates an official record of your claim. It prevents the insurance company from claiming there was a misunderstanding about what you discussed. A written letter shows you are organized and serious about your claim, forcing the adjuster to respond more formally and thoughtfully than they might in a casual phone conversation.

What if the insurance company’s offer seems reasonable but doesn’t cover everything?

This is a very common tactic. An initial offer might cover the basic repair estimate but completely ignore other costs like your rental car, towing fees, or the diminished value of your vehicle. Before accepting any offer, review it carefully against your own itemized list of expenses. If it falls short, you can send a written counteroffer explaining exactly what is missing and why you are entitled to it.

Do I really need to include a diminished value claim?

Yes, you absolutely should. Even if your car is repaired to look brand new, its accident history will permanently lower its resale value. This loss is a real financial damage you have suffered, and you are entitled to be compensated for it. Overlooking diminished value means you are leaving money on the table that is rightfully yours.

What’s the single biggest mistake people make when writing these letters themselves?

The most common mistake is failing to provide strong, organized evidence. Simply stating a dollar amount isn’t enough; you have to prove why you’re owed that specific amount. A letter without attached repair estimates, clear photos of the damage, and a report justifying your diminished value claim is easy for an adjuster to dismiss. Your evidence is what gives your demand its power.

Can I still send a demand letter if the accident was partially my fault?

Yes, you can. Georgia follows a rule that allows you to recover damages as long as you are found to be less than 50% at fault for the accident. However, your final compensation will be reduced by your percentage of fault. Because determining fault can be complex, this is a situation where getting professional legal advice is especially important to protect your claim.