The thought of suing your insurance company is overwhelming. The time, the expense, and the stress are enough to make anyone want to give up and accept a low offer. But what if there was a better way to settle the dispute? The appraisal process is a structured, cost-effective alternative to a lawsuit that can provide a final resolution. When you and the insurer are at an impasse, this process calls for an appraisal umpire to make the final call. This neutral expert reviews the evidence from both sides and makes a binding decision on the value of your claim, helping you avoid a lengthy court battle.

When you and your insurance company are at a standstill over the cost of your vehicle’s repairs or its diminished value, it can feel like you’ve hit a wall. You have your estimate, they have theirs, and the numbers are miles apart. This is where the appraisal process, and specifically an appraisal umpire, can step in to break the deadlock.

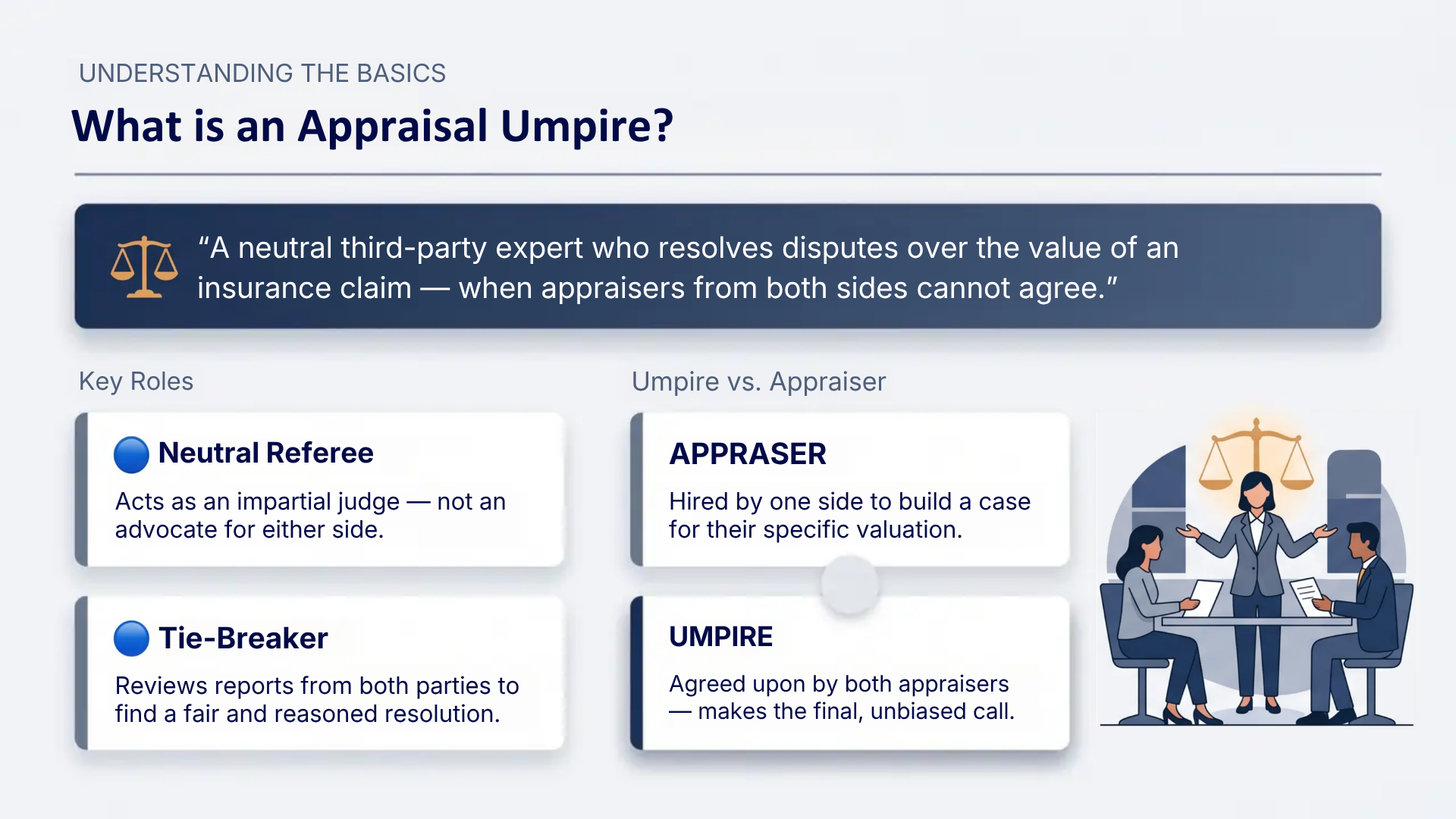

Think of an appraisal umpire as a neutral, third-party referee. Their entire job is to make a fair and impartial decision when two appraisers can’t agree. If you’ve invoked the appraisal clause in your insurance policy, both you and the insurance company will hire your own appraisers. If those two experts can’t reach an agreement, they will together select an umpire to make the final call. This process provides a structured way to resolve disputes without going to court, and the umpire’s decision is typically binding.

An umpire’s primary role is to act as a tie-breaker. They aren’t there to start a new investigation from scratch. Instead, they carefully review the reports and evidence submitted by both your appraiser and the insurance company’s appraiser. Their goal is to understand where the two sides differ and why.

After reviewing the facts, the umpire works to find a fair resolution. They might agree with one appraiser’s assessment entirely, or they might land on a value somewhere in between the two figures. The umpire’s job is to resolve the differences based on the information presented, ensuring the final amount is justified. This focused approach helps settle the dispute efficiently and prevents it from dragging on.

It’s easy to mix up the terms, but appraisers and umpires have very distinct roles. An appraiser is an expert you (and the insurance company) hire to represent your side. Your appraiser inspects your vehicle, documents the damage, and prepares a detailed report arguing for a specific dollar amount for the repairs or loss in value. The insurance company’s appraiser does the same thing for them. Each appraiser is an advocate for their respective party’s position.

An umpire only enters the picture when these two appraisers cannot agree. The umpire is a neutral party, not hired by you or the insurer, but agreed upon by both appraisers. While an appraiser builds a case, an umpire judges the case that has been presented. Their sole function is to listen to both sides and make an unbiased decision to settle the dispute.

If you and your insurance company are at a standstill over the cost of your vehicle’s repairs or its loss in value, you might feel stuck. You know your claim is worth more than their lowball offer, but how do you break the deadlock without heading straight to court? This is exactly where the appraisal process comes into play. It’s a formal method outlined in many insurance policies to resolve disagreements on value. An appraisal umpire is the neutral third party who steps in when your appraiser and the insurance company’s appraiser can’t reach an agreement, making them a key figure in settling the dispute fairly.

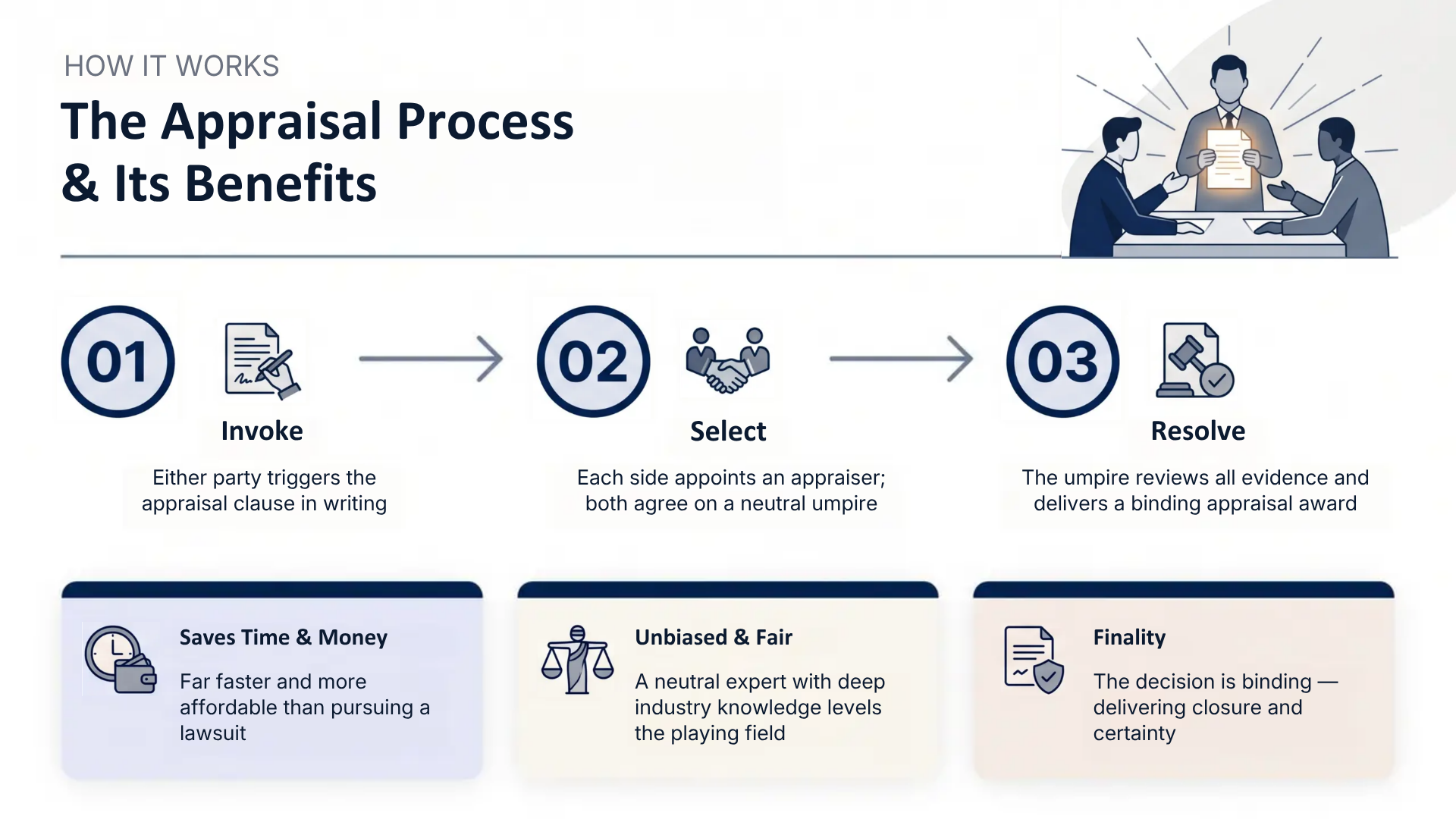

The appraisal process doesn’t just happen automatically. It begins when either you or the insurance company formally requests it in writing, invoking what’s known as the “appraisal clause” in your policy. Think of this clause as a built-in dispute resolution tool. Once invoked, both you and the insurer will hire your own independent, competent appraisers to evaluate the damage and determine the amount of the loss. These two appraisers will then try to negotiate and agree on a fair value. This step is a crucial part of our legal representation at Gastley Law, as we ensure a skilled appraiser is chosen to fight for the true value you’re owed.

Ideally, the two appraisers review the evidence, discuss their findings, and come to an agreement on the value of your claim. But what happens when they can’t? If they’re at an impasse and can’t agree on a final number, it’s time to bring in an umpire. The two appraisers are responsible for selecting a qualified and impartial umpire to act as a tie-breaker. The umpire’s job is to review the findings from both sides and make a final, binding decision. This is a common scenario in claims involving diminished value, where the difference between the two appraisals can be significant. The umpire helps settle the dispute so you can get your compensation and move forward.

When your appraiser and the insurance company’s appraiser can’t agree, an umpire steps in to break the tie. But how do they actually arrive at a decision? It’s not a random guess. The process is structured, impartial, and based entirely on the facts of your claim. Let’s walk through how an umpire is chosen, what they look at, and how final their decision really is.

The first step is selecting the right person for the job. The umpire isn’t assigned by a court; instead, your appraiser and the insurance company’s appraiser must agree on a neutral and competent third party. This selection should happen in a timely manner after both appraisers are appointed. The goal is to find someone who is completely impartial and has the expertise to understand the complexities of your property damage claim. A qualified umpire ensures the process remains fair and focused on the evidence, giving both sides confidence in the outcome.

An umpire doesn’t start from square one. Their main role is to analyze the two different appraisals and find a resolution. They carefully review all the evidence presented by both your appraiser and the insurance company’s appraiser. This includes repair estimates, photographs of the damage, vehicle condition reports, and market analysis for your car’s value. The umpire’s job is to bridge the gap between the two figures, not to create a third, entirely new estimate. By focusing on the existing information, they can pinpoint the exact areas of disagreement and make an informed decision on a fair settlement value.

Yes, the umpire’s decision is typically final and binding. Before making a ruling, a good umpire will often encourage the two appraisers to resolve their differences and reach an agreement on their own. However, if they remain at a standstill, the umpire will make the final call. Once the umpire signs off on an award amount with one of the appraisers, that decision becomes legally binding for both you and the insurance company. This means the dispute is settled, and the agreed-upon amount must be paid. This finality is what makes the appraisal process an effective way to resolve a claim without a lengthy court battle.

When you’re relying on someone to make a final, binding decision on your vehicle’s value, you want to be absolutely sure they know what they’re doing. The appraisal umpire holds a lot of power in this process, so their qualifications are incredibly important. A great umpire isn’t just a random third party; they are a seasoned professional with a specific skill set designed to handle these disputes fairly and accurately. Think of them as a specialized, neutral judge for your property damage claim. They need to be unbiased, deeply knowledgeable, and thorough in their evaluation.

Choosing the right umpire can be the difference between getting the compensation you deserve and walking away with much less than you’re owed. An unqualified or biased umpire can easily side with the insurance company’s lowball offer, leaving you to cover the remaining costs. That’s why it’s so important to understand what separates a truly effective umpire from the rest. It comes down to a solid combination of formal credentials that prove their training and hands-on experience that demonstrates their real-world expertise. Looking for these key qualities helps ensure the person making the final call is equipped to deliver a fair and just outcome for your claim.

One of the clearest indicators of a qualified umpire is their professional certifications. These aren’t just fancy titles; they show that an individual has completed rigorous training and is committed to upholding high industry standards. Organizations like the National Association of Independent Insurance Adjusters (NAIIA) maintain an Appraiser/Umpire Directory of professionals who have met their strict requirements. Similarly, the International Association of Umpires and Appraisers (IAUA) provides respected certifications for property insurance experts, including the Certified Property Insurance Umpire (CPIU). When an umpire holds these credentials, you can feel more confident that they have the specialized knowledge needed to evaluate your claim properly and make an informed decision.

Beyond certifications, practical experience is non-negotiable. A good umpire needs deep subject matter expertise to ensure accurate outcomes in the appraisal process. This means they should have years of experience dealing with vehicle damage, repair costs, and market valuations. They must be fair, impartial, and proactive. A skilled umpire won’t just sit back and listen; they will actively seek more information if they feel the evidence is lacking. They understand their critical role in the resolution of insurance valuation disputes and will give both sides a full opportunity to present their case. This hands-on approach is essential for a just and well-reasoned final award.

When you’re at a standstill with your insurance company over a property damage claim, the thought of a long, drawn-out legal battle can be overwhelming. Fortunately, there’s a more direct path to resolution. The appraisal process, which includes an umpire, is designed to settle these disputes efficiently. It’s a structured way to get a fair outcome without the stress and expense of going to court. Think of it as a practical middle ground that brings in a neutral expert to break the deadlock and help both sides move forward. This process is a key part of the services we offer to ensure you get what you’re owed for your claim. By choosing this route, you are taking a proactive step toward a fair settlement, bypassing many of the headaches associated with traditional litigation.

One of the biggest advantages of using an appraisal umpire is that it’s a way to solve disagreements without immediately heading to court. Lawsuits can take months, or even years, to resolve, all while legal fees pile up. The appraisal process is much faster. Instead of lengthy court procedures, you and the insurance company each present your case to a neutral third party who helps make a final decision. This streamlined approach saves you significant time and money, allowing you to get your settlement and get back on the road sooner. It’s a practical solution for settling disputes over your vehicle’s value and repair costs.

When you’re fighting with an insurance company, it can feel like you’re up against a biased system. An appraisal umpire levels the playing field. This person is a completely neutral expert who isn’t connected to you or the insurer. Their job is to review the evidence from both sides and make an impartial judgment based on their expertise. A qualified umpire has deep knowledge of vehicle values and repair costs, which helps ensure the final decision is accurate and fair. This unbiased perspective is crucial for determining the true diminished value of your car after an accident, ensuring you receive the compensation you deserve.

The goal of the appraisal process is to reach a final, binding decision. After the umpire reviews the evidence and listens to both appraisers, they make a determination on the value of the claim. Once that decision is made, the settlement amount is set, and both you and the insurance company must abide by it. This brings a definitive end to the disagreement, providing the closure you need to move on. You get a clear resolution without the uncertainty and stress of a court trial. If you’re stuck in a dispute and need help getting a final answer, it might be time to contact us to discuss your options.

Navigating a property damage claim can feel overwhelming, but understanding the appraisal process can make it much more manageable. This process is a structured way to resolve disagreements about the value of your claim without heading straight to court. It’s designed to focus on one thing: determining a fair and accurate monetary value for your vehicle’s damages. Knowing what’s coming can help you feel more in control and prepared to advocate for what you’re owed.

When your insurance company’s offer seems too low, you don’t have to simply accept it. You have the right to dispute their valuation through the appraisal process. It’s important to understand that this process doesn’t determine if your policy covers the damage; it only settles disagreements about the cost of the damage itself. Think of it as a specialized negotiation focused entirely on the numbers. This is a powerful tool that allows you to challenge an unfair assessment. Our firm handles these types of property damage claims to ensure you get the full compensation you deserve.

The process begins when both you and the insurance company hire your own independent appraisers. Your appraiser works for you, and their job is to thoroughly inspect your vehicle, review all the documentation, and present a case for its true value after the accident. If the two appraisers can’t agree on a number, they will select a neutral, third-party umpire to help resolve the dispute. The cost of the umpire is typically split 50/50 between you and the insurance company. A skilled appraiser will build a strong case for your vehicle’s diminished value, giving you the best chance at a fair outcome.

If the appraisers reach a stalemate, the umpire steps in to make the final call. The umpire reviews the evidence and arguments from both sides before making a decision on the value of the damage. Once the umpire and one of the appraisers agree on a figure, they sign what is called an “appraisal award.” This award is binding, meaning both you and the insurance company must accept it. The insurer is then expected to pay the amount of the award, closing the claim. If you have questions about this stage of the process, feel free to contact us for guidance.

When you’re already dealing with the financial stress of a car accident, the last thing you want is another huge bill. So, let’s talk about the bottom line: what does an appraisal umpire actually cost? While the final amount can vary based on the complexity of your claim and the umpire’s specific rates, the key thing to remember is that this process is designed to be a cost-effective alternative to litigation. You won’t be facing this expense alone, and it’s structured to be fair to both you and the insurance company.

Think of the umpire’s fee not as just another bill, but as an investment in reaching a fair resolution. You’re paying for an impartial expert’s time, knowledge, and judgment to break a deadlock that could otherwise cost you much more. These appraisal and umpiring services are a practical way to avoid a lengthy and expensive court battle. The total cost typically includes the umpire’s review of all the evidence from both sides, any necessary inspections, and the time it takes to write the final decision, or “award.” Understanding how these costs are split and how they stack up against the alternative will show you why this is often the smartest financial move when you and your insurer can’t agree on the value of your vehicle’s damage.

Here’s the good news: you are not expected to cover the entire cost of the umpire yourself. In the appraisal process, the umpire’s fee is split right down the middle. You pay half, and the insurance company pays the other half. This 50/50 split is a standard part of the process and ensures that both sides have an equal stake in the outcome. Because the umpire is paid by both you and the insurer, it reinforces their neutrality. They aren’t working for one side; they’re working to find a fair value based on the facts. This shared financial responsibility helps keep the process balanced and focused on a just resolution for your property claim.

Hiring an umpire might seem like an added expense, but it’s crucial to compare it to the alternative: a full-blown lawsuit. Going to court can be incredibly expensive, with costs quickly piling up from attorney fees, court filing fees, and expert witness testimony, which can drag on for months or even years. The appraisal process, on the other hand, is designed to be a much faster and more affordable solution. It’s a way to solve disagreements about your claim without immediately resorting to litigation. By sharing the umpire’s fee with the insurer, your total out-of-pocket cost is significantly lower than what you would likely face in a legal battle, giving you a final, binding decision in a fraction of the time.

When you and the insurance company are at a standstill, an appraisal umpire steps in to act as a neutral tie-breaker. Their role isn’t to handle every aspect of your claim but to focus specifically on disagreements about the “amount of loss.” Think of them as a specialist called in to resolve financial disputes after an accident. If your appraiser and the insurance company’s appraiser can’t see eye to eye on the numbers, the umpire is there to make a final, binding decision on those specific points of conflict.

This process is a core part of many property damage claims and is designed to provide a fair resolution without the time and expense of a full-blown lawsuit. The umpire’s job is to analyze the evidence presented by both sides and settle the financial disagreements that are holding up your claim. They focus on the facts and figures to help everyone move forward. This includes disagreements over the vehicle’s value, the cost of repairs, and the true extent of the damage.

One of the most common disputes involves the actual value of your vehicle. This can be its pre-accident cash value if it’s a total loss, or its diminished value after repairs have been completed. You might believe your car was worth $20,000 before the accident, but the insurance company offers only $15,000. An umpire plays a crucial role in resolving these disagreements. They will review both appraisals, look at market data, and consider the vehicle’s condition to determine a fair and impartial value, breaking the deadlock so you can get the compensation you deserve.

Sometimes, the conflict isn’t about the car’s total value but about how much the repairs should cost. Your trusted body shop might quote $6,000 for a quality repair, while the insurer’s appraiser insists it can be done for $4,000 using different parts or labor rates. Many insurance policies state that the appraisal process is specifically for disputes over the amount of loss, which directly includes conflicts over repair costs. An umpire will examine both estimates, consider industry standards for labor and parts, and decide on a reasonable cost for the necessary repairs.

An umpire also settles disagreements about the scope of the damage itself. For instance, your appraiser might say a door needs to be completely replaced, while the insurance company’s appraiser argues it can be repaired. The umpire’s job is not to create a new estimate from scratch. Instead, they review the two existing appraisals and resolve the specific disputes about the extent of the damage. They look at photos, repair procedures, and expert opinions to decide which assessment is more accurate. If you’re facing this kind of stalemate, you can always contact our team to understand your options.

When you’re in a dispute with an insurance company, the idea of bringing in another person can feel daunting. The appraisal process, and the role of an umpire, is often surrounded by misinformation that can make people hesitant. Let’s clear up a few common myths so you can feel more confident about the process. The truth is, using an appraisal umpire is a standard and effective way to settle disagreements over your vehicle’s value, and understanding how it works is the first step toward getting the compensation you deserve.

One of the biggest fears people have is that an umpire will automatically side with the insurance company. It’s easy to think they’re just another part of the system working against you. In reality, umpires are required to be neutral third parties. Their professional reputation depends on their impartiality. An umpire’s job isn’t to save the insurer money; it’s to provide a fair and objective resolution based on the facts presented by both sides. Think of them as a referee whose goal is to make the right call, ensuring your diminished value claim is assessed fairly.

It’s a common misunderstanding that an umpire has free rein to come up with any number they want. That’s simply not the case. An umpire doesn’t start from scratch. Instead, their role is to review the two different appraisals submitted by you and the insurance company. They then work within that range to find a fair middle ground and resolve the specific points of disagreement. They can’t introduce new types of damage or create their own estimate out of thin air. Their authority is limited to settling the dispute between the two existing figures, which keeps the process focused and efficient.

The thought of a formal appraisal process can sound intimidating, like you’re about to enter a complex legal battle. But the appraisal clause in your insurance policy is actually designed to be a more straightforward alternative to a lawsuit. It’s a structured method for resolving disagreements about the amount of a loss without the time and expense of going to court. While there are specific steps to follow, the process is much more direct than litigation. Having an experienced attorney guide you through our legal services can make it feel even more manageable, ensuring your rights are protected every step of the way.

This is a common concern, but it’s important to know that the umpire’s decision is almost always final and legally binding. Once the umpire and one of the appraisers sign the award, both you and the insurance company are required to accept it. The process is designed this way to provide a definitive end to the dispute without dragging it into court. This finality is what makes it an effective alternative to a lengthy lawsuit.

The appraisal process is not just for cars that are a total loss. It is frequently used to settle disputes over the cost of repairs and, very importantly, for diminished value claims. Even if your car is perfectly repaired, its market value has likely dropped. If you and the insurer can’t agree on the amount of that value loss, invoking the appraisal clause is an excellent way to get a fair and final number.

Yes, you are responsible for paying for the appraiser you hire to represent your side of the dispute. The umpire’s fee is a separate cost that is typically split evenly between you and the insurance company. While it is an investment, hiring a skilled appraiser is crucial for building a strong case and ensuring the umpire has all the correct information to make a fair decision.

While both are neutral third parties, their roles are very different. A mediator helps facilitate a conversation between you and the insurance company, guiding you toward a mutual agreement. However, a mediator cannot force a decision. An umpire, on the other hand, has the authority to make a final, binding decision. They act more like a judge for the specific financial dispute, breaking the tie when the two appraisers cannot agree.

No, you cannot hire an umpire directly. The umpire must be selected and agreed upon by both your appraiser and the insurance company’s appraiser. This procedure ensures the umpire remains a neutral party who is acceptable to both sides. The process starts with each party hiring their own appraiser, and only if those two experts reach a deadlock is an umpire brought into the picture.