A Guide to the Insurance Appraisal Process

You’ve done everything right after your car accident. You filed the claim, got repair estimates, and sent all the paperwork to the insurance company. But their offer is shockingly low, and the adjuster won’t budge. It’s a frustrating stalemate that can make you feel powerless. Before you even think about a lawsuit, you need to know about a powerful tool written into most auto policies: the insurance appraisal process. This is a formal method for resolving disagreements over the value of your claim. This guide will walk you through exactly what it is, how it works, and how to decide if it’s the right next step for you.

Key Takeaways

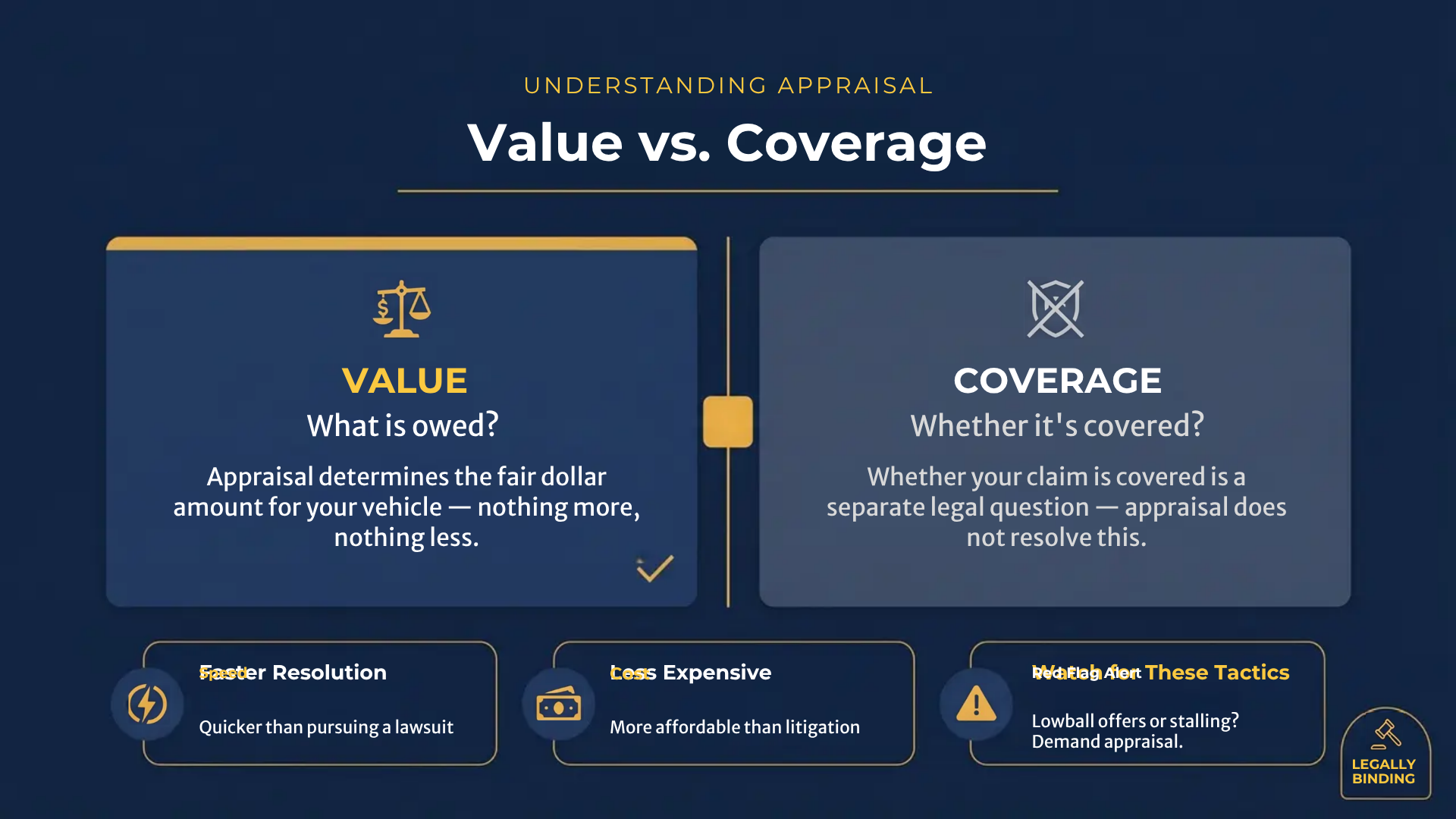

- Appraisal settles value, not coverage: Use this process when you and your insurer disagree on the cost of repairs or diminished value. It cannot resolve disputes where your claim has been denied entirely based on your policy’s coverage.

- The decision is final and made by experts: You and your insurer each hire an appraiser, and a neutral umpire makes the final call if they disagree. This decision is legally binding, so you cannot appeal it simply because you are unhappy with the amount.

- Prepare your evidence and get legal advice: Before demanding appraisal, gather all your repair estimates and documentation. An attorney can help you determine if appraisal is your best option and ensure you are fully prepared for the process.

What Is the Insurance Appraisal Process?

After a car accident, the last thing you want is a fight with your insurance company over repair costs. If you and your insurer agree the damage is covered but can’t agree on the price tag, the insurance appraisal process might be your next step. It’s a formal method in many policies to resolve disagreements about the dollar amount of a loss and get a binding second opinion when you’ve reached a stalemate.

What It Is and Why It Matters

Insurance appraisal is a dispute resolution tool for disagreements over the value of a claim. Let’s say your insurer offers $5,000 for repairs, but your quotes are closer to $8,000. This is where appraisal comes in. It’s not for arguing about coverage; it’s strictly for settling disputes about the amount you’re owed. This process is especially useful for complex issues like diminished value, where your car’s loss in market value is contested. Invoking the appraisal clause in your policy can be a powerful way to get a fair assessment.

Appraisal vs. Litigation vs. Mediation: What’s the Difference?

It’s easy to confuse appraisal, litigation, and mediation. Litigation means filing a lawsuit, which is often long, expensive, and confrontational. Mediation involves a neutral third party who helps you and the insurer try to reach an agreement, but they can’t force a decision. Appraisal is typically faster and less formal than a lawsuit. Each side hires an appraiser, and if they can’t agree, a neutral umpire makes the final call. The decision on the value is binding, so you usually can’t appeal it. Understanding which path is right for you is a key part of our legal services.

Common Myths About Insurance Appraisal

A big myth is that appraisal can solve any disagreement with your insurer. That’s not true. It only determines the amount of the loss; it cannot decide if your policy covers the damage. If your claim is denied entirely, appraisal isn’t the right tool. Another misconception is that the outcome is just a suggestion. In reality, the decision is binding for both you and the insurance company. It’s very difficult to challenge the final amount later, so it’s critical to get it right from the start. If you’re facing a lowball offer, it’s wise to contact an attorney to see if appraisal is your best option.

Is the Insurance Appraisal Process Right for Your Claim?

Deciding whether to enter the insurance appraisal process can feel like a major crossroads in your claim. It’s a powerful tool, but it isn’t the right fit for every situation. Before you demand an appraisal, you need to get clear on exactly what you’re disputing with the insurance company. Understanding the nature of your disagreement will help you choose the most effective path forward and avoid wasting time and money on a process that can’t solve your specific problem.

The key is to figure out if your fight is about the value of your loss or the coverage itself. Once you know that, you can determine if appraisal is your best move or if you need a different strategy.

Is Your Dispute About Coverage or Value?

The first question to ask is simple: Does the insurance company agree that your policy covers the damage? The appraisal process is designed to resolve disagreements over the amount of a loss, not whether the loss is covered in the first place. Think of it this way: appraisal can settle an argument over whether a repair costs $5,000 or $8,000. It cannot settle an argument over whether your policy should pay for the repair at all.

If your insurer denies your claim entirely, saying the damage isn’t covered, appraisal won’t help. In that scenario, you’re dealing with a coverage dispute, which is a legal issue that often requires legal representation to resolve.

When Appraisal Is the Best Path Forward

Appraisal is often the best path forward when you and the insurer agree that the damage is covered, but you’re far apart on the cost of repairs or the diminished value of your vehicle. For disputes involving lost resale value, an experienced Atlanta diminished value attorney can help evaluate whether appraisal or another strategy is the stronger move. If the insurance company’s offer seems unreasonably low and negotiations have stalled, either you or the insurer can formally request an appraisal in writing.

This process is typically much faster and less expensive than filing a lawsuit. It’s a structured way to get an impartial decision on the dollar amount of your damages without the drawn-out stress of litigation. When the only thing standing between you and a fair settlement is a number, appraisal can be the most efficient way to close the gap.

Red Flags: Signs You Should Demand Appraisal

So, when should you seriously consider demanding an appraisal? The most obvious red flag is a lowball offer that doesn’t come close to covering your repair estimates or documented value loss, especially if the difference is thousands of dollars. If you have solid evidence, like quotes from reputable body shops or a professional diminished value report, and the adjuster refuses to budge, it’s a clear sign that you need a neutral third party to step in.

Another red flag is when the insurer endlessly delays or uses vague excuses to avoid paying the full amount you are owed. If you feel like you’re being given the runaround on the value of your claim, initiating the appraisal process can force the issue and move your claim toward a final resolution. If you see these signs, it may be time to get in touch with an expert.

How the Insurance Appraisal Process Works, Step by Step

When you and your insurer disagree on your property damage claim’s value, the appraisal process offers a structured path to resolution. It follows clear steps, bringing in neutral experts to determine a fair value for your loss. Here’s what to expect at each stage.

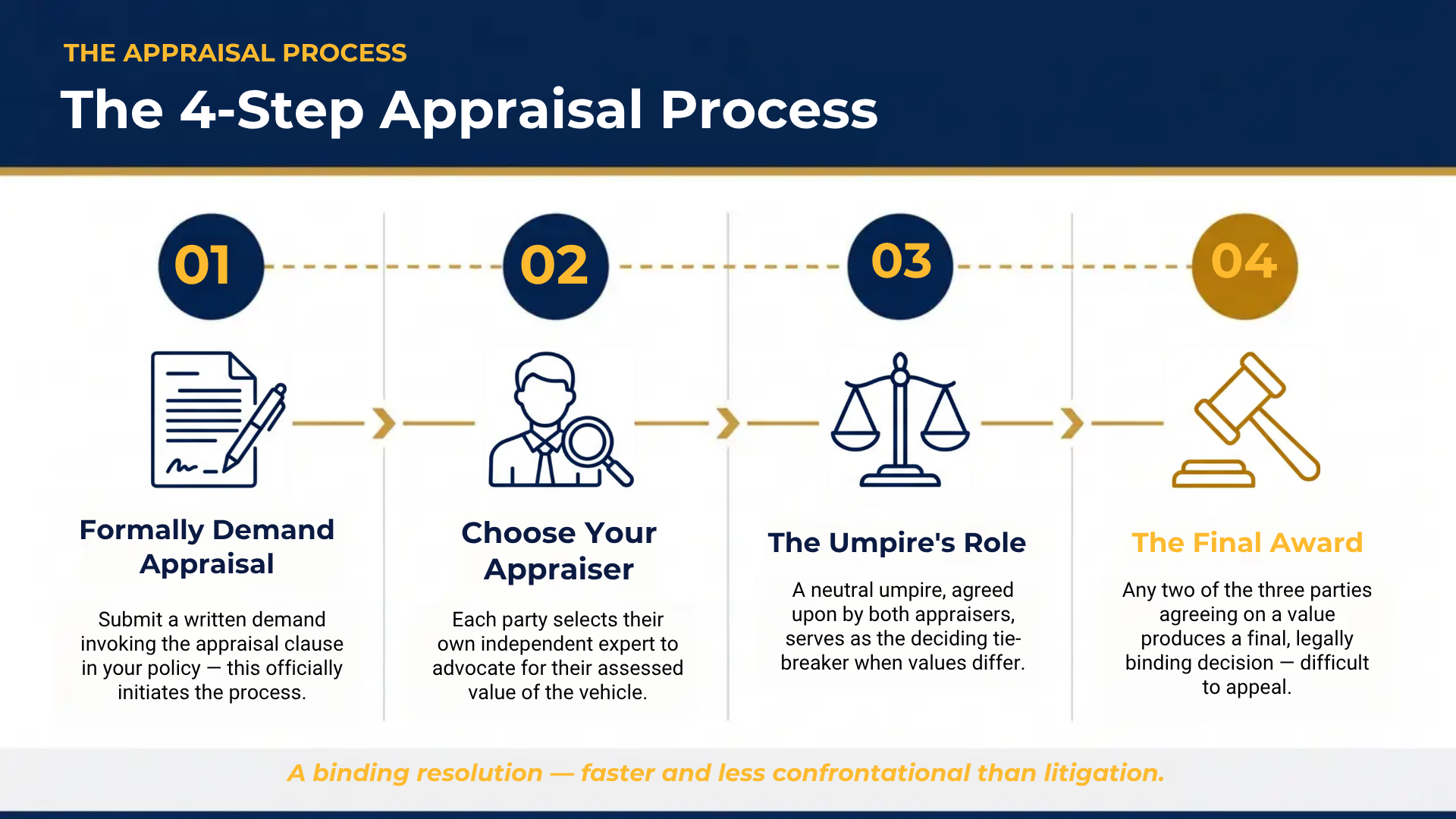

Step 1: Formally Demand an Appraisal

This is your official first move. To start the process, you must make a formal, written demand for appraisal. This isn’t just a casual email; it’s a formal action that invokes the appraisal clause in your policy. Putting your request in writing creates a clear record and legally requires the insurance company to participate. This single step shifts the dynamic from a frustrating back-and-forth to a structured process.

Step 2: Choose Your Appraiser

After demanding appraisal, both you and the insurer select an independent appraiser. You have 20 days to choose your representative and notify the other party. This is a critical decision. Your appraiser is your advocate, responsible for evaluating the damage and arguing for its true value. Getting specialized legal representation can help you find a qualified appraiser who will fight for your best interests and ensure your claim is valued fairly.

Step 3: Understand the Umpire’s Role

Next, the two chosen appraisers will select a neutral third party called an umpire. Think of the umpire as a tie-breaker. Their job is to step in if your appraiser and the insurer’s appraiser can’t agree on the final amount. If they can’t decide on an umpire within 15 days, either side can ask a judge to appoint one. The umpire is essential for ensuring that a deadlock between the two sides doesn’t stop your claim from moving forward.

Step 4: Receive the Final Decision

The process ends when a final decision on your loss is reached. This decision, or “award,” is determined when any two of the three parties (your appraiser, the insurer’s, or the umpire) agree. Once set, the award is legally binding for both you and the insurance company. This means the dispute over value is officially over, and the insurer must pay the agreed-upon amount. Because the decision is final, it’s wise to get answers to your questions beforehand. Feel free to contact us for guidance.

The Costs and Challenges of Insurance Appraisal

While the appraisal process can be a powerful tool for resolving disputes over the value of your claim, it’s important to go in with your eyes open. Like any formal process, it comes with its own set of costs and potential roadblocks. Understanding these challenges ahead of time will help you decide if it’s the right move for you and prepare you for what’s to come.

What Will It Cost You?

One of the first questions people ask is about the cost. When you demand an appraisal, you are responsible for paying for your own appraiser. Think of this as hiring an expert to represent your side of the argument. The insurance company will do the same.

From there, you and the insurance company will split the costs for the umpire and any other related expenses right down the middle. While it is an out-of-pocket expense, it’s often a necessary investment to fight a lowball offer and get the full amount you’re truly owed for your vehicle’s damages.

The Challenge of Finding an Unbiased Appraiser

Finding the right appraiser is crucial, but it isn’t always easy. You need someone who is not only an expert in vehicle valuation but also completely neutral and dedicated to fighting for a fair outcome. Unfortunately, it can be hard to find qualified, unbiased appraisers who are willing to work for policyholders.

On top of that, both sides have to agree on a neutral umpire. Insurance companies can sometimes be difficult, rejecting qualified umpires in an attempt to delay the process or gain an advantage. This is one of the key areas where having an experienced attorney on your side can make a significant difference.

How Long Does It Take (and Is the Decision Final)?

The appraisal process is generally faster than a lawsuit, but it isn’t instant. The timeline can vary depending on how quickly you and the insurer select your appraisers and agree on an umpire.

Once the umpire makes a decision, that’s usually the end of the road. The appraisal award is binding for both you and the insurance company. It is very difficult to challenge the outcome later unless you can prove the insurer acted in bad faith or breached the terms of your policy. This finality is why it’s so important to get the process right from the start.

Know the Limits: What Appraisal Can and Can’t Do

It’s critical to understand what appraisal can and cannot accomplish. The appraisal process is designed to resolve one thing and one thing only: the amount of the loss. It answers the question, “How much is this damage worth?”

What appraisal doesn’t do is determine whether your damage is covered by your policy in the first place. If the insurance company is denying your claim entirely, saying the damage isn’t covered, appraisal won’t solve that. It only deals with disagreements over the cost of the damage, not disputes about coverage or bad faith practices by the insurer.

Appraisal or Lawsuit: Which Should You Choose?

Deciding between invoking the appraisal clause in your insurance policy and filing a lawsuit can feel overwhelming. Both paths are designed to resolve disputes with your insurance company, but they work very differently. An appraisal is a structured process to determine the amount of your loss, while a lawsuit is a formal legal action. Understanding the key differences, including the time, cost, and potential outcomes, is the first step toward getting the fair compensation you deserve for your vehicle’s damages. Let’s walk through the pros and cons of each so you can make an informed choice for your situation.

The Pros of Choosing Appraisal

When you and your insurer agree that the damage to your car is covered but can’t agree on the repair cost or its diminished value, appraisal can be a great option. Generally, the appraisal process is much faster and less expensive than a lawsuit. It’s a more direct route to a resolution because it avoids the lengthy procedures of the court system.

Think of it as a focused negotiation. It’s less confrontational than litigation because it centers on one specific question: how much is your claim worth? This process can be a powerful tool, especially when you feel your insurance company is offering too little. The final decision is binding, which means once the amount is set, the dispute is over, and you can move forward.

The Cons You Need to Consider

While the finality of an appraisal can be a good thing, it’s also one of its biggest drawbacks. The decision is binding, which means it’s very difficult to challenge the outcome later. Unless you can prove there was fraud or misconduct, you can’t appeal the decision simply because you’re unhappy with the amount.

Another major limitation is that appraisal only addresses the dollar value of your damages. It cannot resolve disputes over whether your policy covers the damage in the first place. If your insurer has denied your claim entirely or if you believe they’ve acted in bad faith, appraisal won’t help. It’s a tool for disagreements about value, not coverage or unfair practices.

How to Prepare Your Evidence for the Best Outcome

To get the best possible result from an appraisal, you need to come prepared. Your appraiser will advocate for you, but they need strong evidence to build their case. Start by gathering all your documentation. This includes taking clear photos of the damage from multiple angles, getting detailed repair estimates from reputable body shops, and keeping a meticulous record of every conversation and email with the insurance company.

Your appraiser will inspect your vehicle and use your evidence to argue for the true cost of repairs. The more proof you can provide, the stronger their position will be. Think of yourself as the chief investigator of your own claim. Every receipt, every estimate, and every note you take helps build a comprehensive picture of your loss for the appraisal panel.

Why You Should Talk to a Lawyer First

Before you demand an appraisal, it’s wise to get legal advice. An experienced attorney can review your case and help you decide if appraisal is truly the best path forward. Sometimes, an insurer might push for appraisal to avoid addressing bigger issues, like acting in bad faith. A lawyer can spot these red flags and protect your rights.

If your insurance company is denying coverage altogether, you’ll likely need legal help to fight that decision. At Gastley Law, we can assess your policy and the specifics of your claim to determine the right strategy. We’ll help you understand all your options so you can confidently pursue the full compensation you’re owed. Contact us for a clear evaluation of your case.

Related Articles

Frequently Asked Questions

Can I use the appraisal process if my insurance company denies my claim?

No, the appraisal process is not the right tool if your claim has been denied entirely. Appraisal is specifically designed to settle disagreements about the dollar amount of a covered loss, like the cost of repairs or your car’s diminished value. If the insurer says your policy doesn’t cover the damage at all, you are facing a coverage dispute, which is a separate legal issue that appraisal cannot resolve.

Who pays for the insurance appraisal process?

You and the insurance company share the costs. You are responsible for paying the appraiser you hire to represent your side of the case. The insurance company pays for its own appraiser. The cost of the neutral umpire, who acts as a tie-breaker, is split evenly between you and the insurer.

What happens if I disagree with the final appraisal decision?

The decision reached by the appraisal panel, known as the award, is legally binding for both you and the insurance company. This means the outcome is final, and it is very difficult to challenge it later on. You generally can’t appeal the decision just because you are unhappy with the amount, which is why it’s so important to have a strong case and an expert appraiser from the very beginning.

Why would I choose appraisal instead of just filing a lawsuit?

Appraisal is often a much faster and more cost-effective way to resolve a dispute over the value of your claim. Lawsuits can take a long time and involve significant legal fees and court costs. Appraisal is a more focused process that avoids the complexities of litigation by concentrating only on settling the disagreement over the monetary value of your damages.

Do I need to hire a lawyer to help me with the appraisal process?

While you aren’t required to have a lawyer, getting legal advice is a very smart move. An attorney can help you determine if appraisal is the best strategy for your specific situation, assist you in finding a qualified and unbiased appraiser, and ensure your rights are protected throughout the process. Sometimes, an insurer might try to use appraisal to avoid dealing with other issues, and a lawyer can identify these tactics.