Your Guide to Rental Car Reimbursement in Georgia

Many drivers assume that if an accident isn’t their fault, the other person’s insurance will instantly provide a rental car. Unfortunately, that’s rarely how it works. Waiting for the other insurer to accept liability can take days or even weeks, leaving you without transportation. Your own rental car reimbursement coverage is often the fastest way to get back on the road. It allows you to get a rental immediately while your insurance company handles the reimbursement process with the at-fault party’s insurer. This guide will walk you through how this valuable coverage works and why you shouldn’t rely on someone else’s policy.

Key Takeaways

- Add rental reimbursement before you need it: This coverage is an inexpensive, optional add-on that helps pay for a rental car after a covered accident, but it won’t apply to mechanical failures or routine maintenance.

- Review your policy’s daily and total limits: Know your specific coverage caps, like $40 per day for 30 days, to manage your expenses and avoid paying out-of-pocket for a rental.

- Consult an attorney if your claim is delayed or denied: If an insurance company gives you the runaround, a lawyer can help you understand your rights and fight for the full compensation you deserve for your property damage claim.

What Is Rental Car Reimbursement Coverage?

After a car accident, one of the first problems you face is simple: how do you get around? If your car is in the shop for repairs, rental car reimbursement coverage can be a lifesaver. It’s a part of your insurance policy designed to keep you on the road while your vehicle is out of commission. Let’s break down what this coverage is, how it works, and some common misunderstandings about it.

What It Is and Why You Might Need It

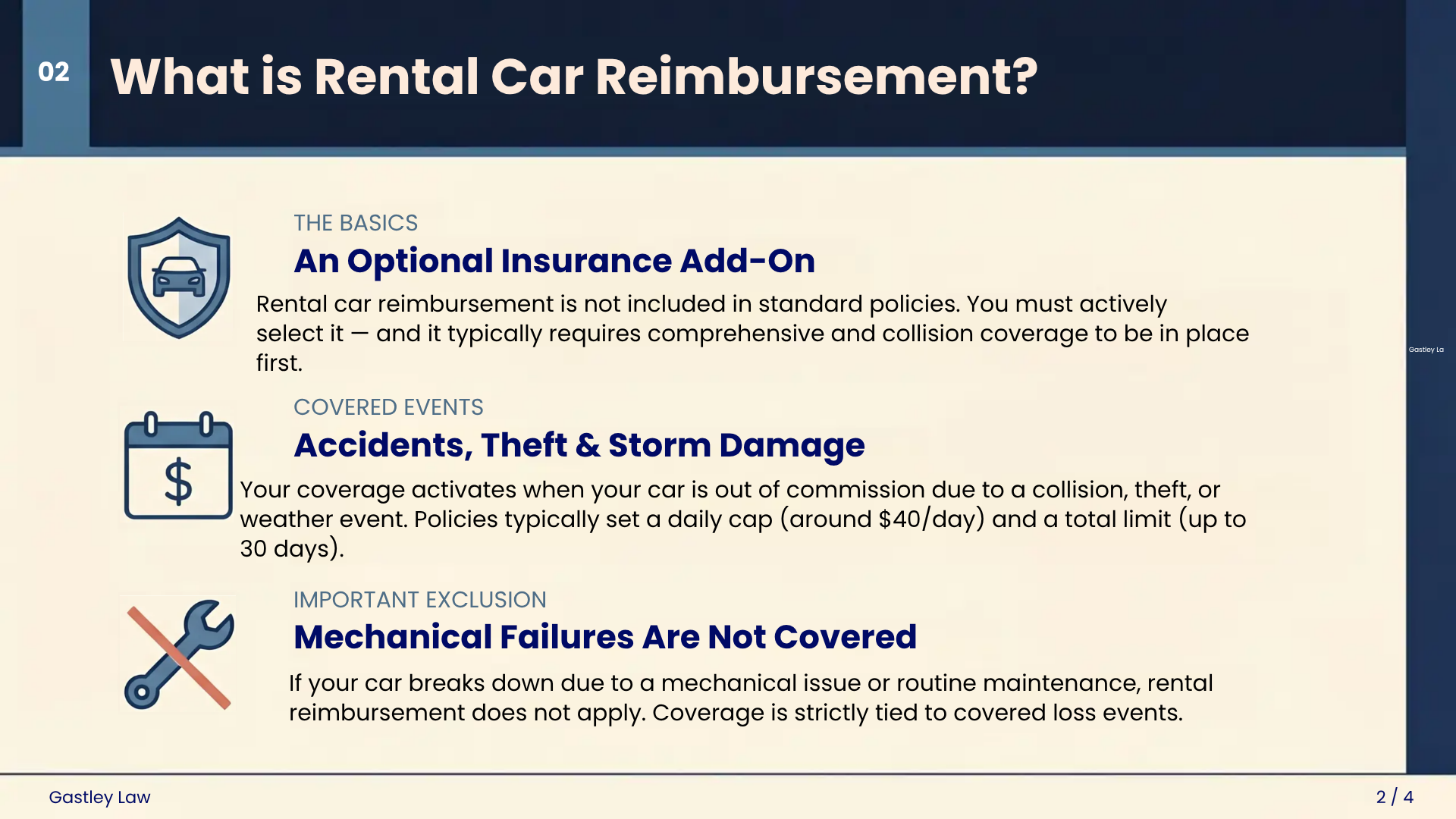

Think of rental car reimbursement as an optional add-on to your auto insurance policy. Its job is to help cover the cost of a rental car while yours is being repaired after a covered accident. Without it, you could be stuck paying out-of-pocket or relying on friends and family to get to work, pick up the kids, and run errands. This coverage is designed to keep your daily life on track with minimal disruption, giving you a temporary set of wheels when you need them most. It provides peace of mind and practical support right when things feel most chaotic.

How It Works with Your Existing Policy

To get rental reimbursement, you usually need to have comprehensive and collision coverage on your policy first. When you’re in an accident, you can file a claim to activate it. If the other driver was at fault, their insurance should eventually cover the rental, but that can take time. Using your own coverage is often much faster. Just be aware of the fine print: your policy will have a daily limit (like $40 per day) and a total maximum payout. Understanding these limits is crucial for managing your insurance claim and avoiding surprise costs down the line.

Common Myths About Rental Coverage

There’s a lot of confusion around rental reimbursement, so let’s clear a few things up. First, this coverage is for accidents, not for when your car breaks down from mechanical failure. Second, many drivers assume it’s standard, but it’s an optional add-on that you have to select. A big one to remember is that the coverage often stops once your insurance company declares your car a total loss, which can leave you without a rental before you’ve received a settlement check. If you’re unsure about your policy’s specifics, it’s always a good idea to get in touch with an expert for clarity.

How Does Rental Reimbursement Work After an Accident?

After an accident, the last thing you want to worry about is how you’ll get to work or pick up your kids. If your car is in the shop for repairs, rental reimbursement coverage can be a huge help. It’s an optional part of your auto insurance policy designed to cover the cost of a rental car so you can get back to your life with minimal disruption. Let’s walk through how it works.

When Your Coverage Kicks In

Rental reimbursement coverage applies when your car is undrivable due to a covered incident, like a collision. Once you file a claim and it’s approved, this coverage helps pay for a rental vehicle while yours is being repaired. It’s important to remember this isn’t standard on every policy; it’s an add-on you have to select. If you’re in an accident that wasn’t your fault, the other driver’s insurance should cover your rental, but having your own coverage can speed things up significantly, getting you back on the road faster.

The Fine Print: Daily Limits and Coverage Duration

It’s crucial to understand the limits of your rental reimbursement coverage to avoid surprise costs. Most policies have a per-day and a per-accident maximum. For example, your policy might cover $40 per day for up to 30 days. If you rent a more expensive car or if repairs take longer than a month, you could end up paying the difference out of pocket. Always check your specific policy details so you know exactly what’s covered before you head to the rental counter. This helps you make an informed choice and manage your expenses effectively.

How to File Your Claim (and the Paperwork You’ll Need)

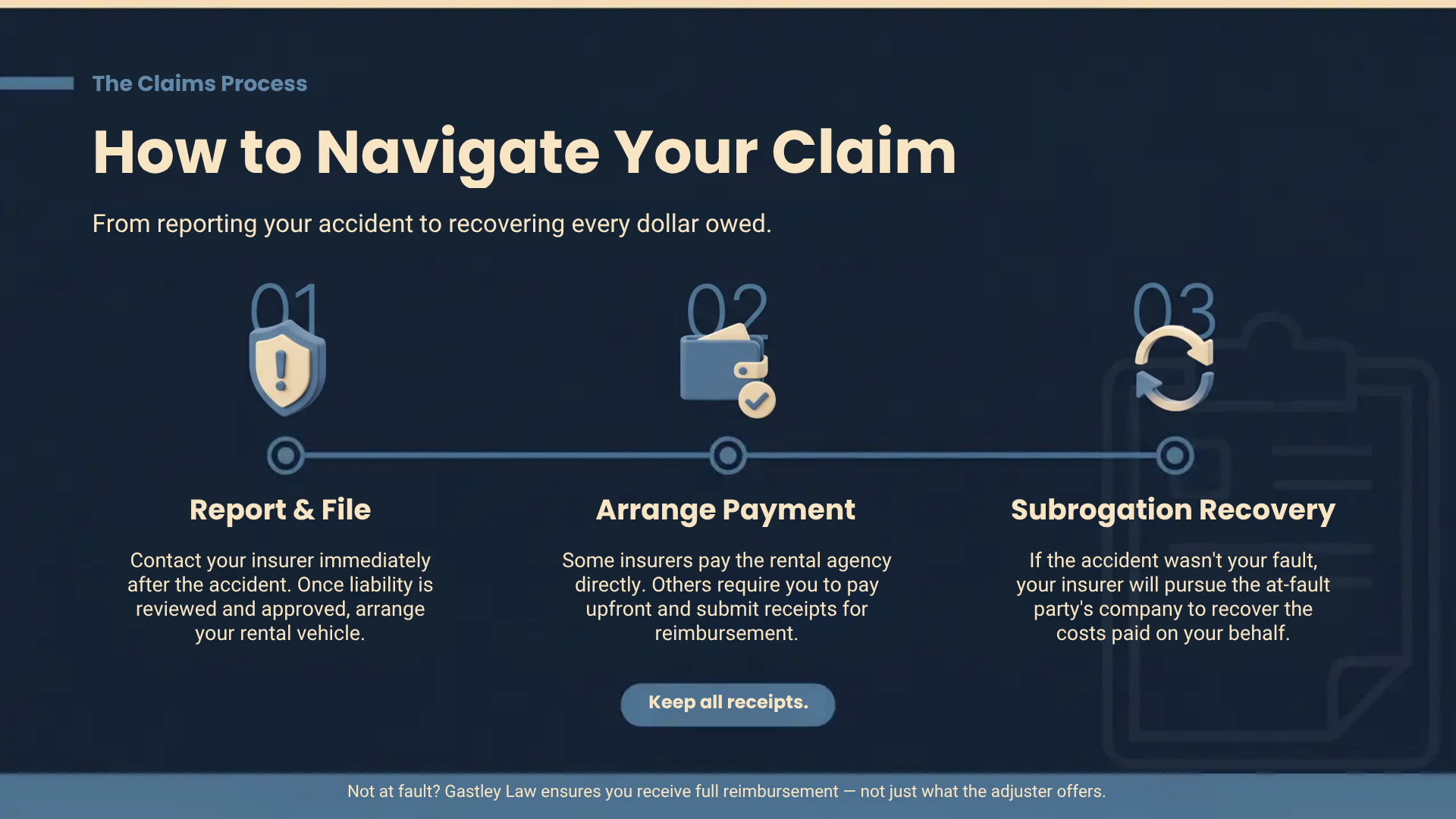

To use your rental reimbursement, you first need to report the accident to your insurance company. Once they approve your property damage claim, you can arrange for a rental car. Some insurers have partnerships with specific rental companies and can pay them directly, which is very convenient. In other cases, you’ll pay upfront and submit your receipts for reimbursement. Either way, hold on to every piece of paperwork, including your rental agreement and all payment receipts. Having a clear paper trail makes the entire process much smoother and helps ensure you get paid back promptly.

Know Your Rights When Filing a Claim

You have options when it comes to getting a rental car. If the other driver was at fault, their liability insurance should pay for your rental. However, dealing with another person’s insurance company can sometimes be slow. Using your own rental reimbursement coverage is often the quickest way to get a vehicle. Your insurance company can then seek reimbursement from the at-fault driver’s insurer, a process called subrogation. If you run into any issues or feel the insurance company isn’t treating you fairly, don’t hesitate to contact a lawyer to understand your rights and get the help you deserve.

What’s Covered (and What’s Not)?

Understanding the fine print of your rental reimbursement coverage can save you a lot of headaches after an accident. It’s not a free pass for any rental car, anytime. Instead, it’s a specific tool designed to help you in a specific situation. Knowing the boundaries of your policy helps you plan accordingly and avoid surprise expenses while your car is in the shop. Let’s break down what your policy likely includes and, just as importantly, what it leaves out.

What Your Policy Typically Covers

Think of rental reimbursement as an optional add-on to your auto insurance that helps you stay on the road after a covered accident. If your car is undrivable or in the repair shop, this coverage helps pay for a rental vehicle. Most policies set a daily limit, often between $30 and $50 per day, and a maximum number of days, usually around 30. This is meant to cover the cost of a basic rental while you wait for repairs. It’s a lifesaver when you rely on your car for daily life, ensuring you can still get to work and run errands without paying entirely out of pocket. These insurance services are designed to minimize disruption to your routine.

Common Exclusions to Watch Out For

It’s crucial to know that this coverage isn’t for every situation. For instance, it won’t apply if your car breaks down from a mechanical failure or needs routine maintenance like an oil change. It also doesn’t cover a rental car for a vacation or a weekend trip. The key is that the need for a rental must stem from a “covered loss” under your policy, like a collision, theft, or storm damage. An insurer will only approve the rental expense if the primary damage to your car is something your policy is already set to cover. Reading your policy carefully helps you understand exactly what a covered event includes.

How Georgia’s Rules Affect Your Coverage

Here in Georgia, the terms of your rental reimbursement coverage are dictated by your specific insurance policy. While a 30-day limit is common, it’s not a universal rule, so you should always check your own documents for the exact daily rate and duration. If another driver was at fault for the accident, their insurance company is responsible for your “loss of use,” which includes the cost of a rental. However, dealing with the other party’s insurer can be slow. Having your own coverage allows you to get a rental right away while your insurance company seeks reimbursement from the at-fault party. If you’re unsure about your policy’s specifics, we can help you understand your rights.

Potential Gaps That Can Cost You

Many drivers are surprised to learn that rental reimbursement is not standard and must be added to a policy. If you don’t have it, you could be left paying for a rental yourself. Another common issue is when the daily coverage limit, say $40 a day, isn’t enough to rent a vehicle comparable to your own, especially if you drive an SUV or truck. This gap means you’ll have to pay the difference out of pocket. Using your own coverage is often faster than waiting for the at-fault driver’s insurance to act, but the claims process can be tricky. An experienced attorney can help you manage your property damage claim and fight for full compensation.

Is Rental Reimbursement Coverage Worth It for You?

Deciding whether to add another line item to your insurance bill can be tough. But when you rely on your car every day, going without it for weeks can throw your entire life off track. Rental reimbursement coverage is designed to bridge that gap, but is it the right choice for your specific needs and budget? Let’s look at the costs, how to get it, and what to do if the insurance company pushes back. Understanding these details will help you make an informed decision and know how to handle a claim if you ever need to.

How Much Does It Cost?

The good news is that rental reimbursement insurance is usually a low-cost extra you can add to your auto policy. For just a few dollars a month, it can save you from paying hundreds or even thousands out of pocket for a rental car while yours is in the shop. Think of it as a safety net. If you don’t have a second vehicle, can’t rely on public transportation, and would struggle to pay for a rental yourself, this affordable coverage can be a lifesaver after an accident.

Adding Coverage to Your Policy

Adding rental reimbursement to your policy is straightforward. You don’t have to wait for your renewal period; you can add this coverage at any time. Just call your insurance agent or update your policy online. The key thing to remember is that the coverage only applies to accidents that happen after you’ve added it. So, if you’re thinking about it, it’s better to act sooner rather than later. Most major insurance providers offer it, making it an accessible option for almost any driver.

What to Do If Your Claim Is Denied

If you find yourself needing a rental car after an accident, your first step is to file a claim. If another driver was at fault, their insurance company should cover the cost, but be prepared for delays. It can often be faster to use your own rental reimbursement coverage and let your insurance company seek reimbursement from the at-fault party’s insurer later. If the other driver’s insurance is giving you the runaround or denying the claim, you’ll need to speak directly with their adjuster and stand firm on your right to a rental.

How a Lawyer Can Help You Get What You’re Owed

Insurance adjusters often try to settle claims quickly and for the lowest amount possible. This is especially true when it comes to things like rental cars and diminished value. Before you accept any offer, it’s wise to get a professional opinion. An experienced Atlanta diminished value attorney can help review the full value of your claim and identify compensation you may be missing. At Gastley Law, we fight to make sure you receive fair treatment and the compensation you deserve for all your property damage needs. If you’re struggling with an insurer, contact us for help.

Related Articles

- When to Hire a Property Damage Car Accident Attorney

- What to Do If You Don’t Agree With a Total Loss Adjuster

- How Often Do Insurance Companies Deny Claims? Data

Frequently Asked Questions

What if the other driver was at fault? Should I use their insurance or my own for the rental?

While the at-fault driver’s insurance is ultimately responsible for your rental car costs, it can be much faster to use your own rental reimbursement coverage first. Dealing with another person’s insurer often involves delays while they investigate the claim. By using your own policy, you can get a rental car right away. Your insurance company will then work to get its money back from the other insurer through a process called subrogation.

What happens if my car repairs take longer than my policy’s rental limit, like 30 days?

If your repairs extend beyond your policy’s maximum number of days, you will likely have to pay for the additional rental days out of your own pocket. This is why it’s so important to stay in close contact with the repair shop for updates. If the delays are unreasonable or caused by the insurance company, you may have grounds to push for an extension, but this can be a difficult process to handle on your own.

Does rental reimbursement cover extra costs like gas or the rental company’s insurance?

Typically, no. Your rental reimbursement coverage is designed to cover the daily rental rate of the vehicle up to your policy limit. It does not usually cover additional expenses like fuel, security deposits, mileage fees, or the supplemental insurance offered at the rental counter. You should plan to cover these costs yourself.

My policy has a daily limit. What if that’s not enough to rent a car similar to mine? This is a common problem, especially if you drive a larger vehicle like an SUV or a truck. If your policy’s daily limit (for example, $40 per day) doesn’t cover the cost of a comparable rental, you are responsible for paying the difference. When you purchase the coverage, it’s a good idea to choose a daily limit that reflects the actual cost of renting a vehicle similar to the one you drive.

If my car is totaled, how long do I get to keep the rental?

This is a critical point many people miss. If your insurance company declares your car a total loss, your rental reimbursement coverage often ends very quickly, sometimes as soon as they make you a settlement offer. This can happen before you’ve even received the check, leaving you without a vehicle. It’s a tough situation, and it’s one of the key moments where having an advocate on your side can make a significant difference.