How to Win Your Total Loss Settlement Negotiation

No one knows your car’s history and condition better than you do. The insurance adjuster sees a set of statistics on a screen; you see the new tires you bought last fall and the money you invested in regular maintenance. This makes you the most important advocate in your own claim. This guide is designed to give you the tools and confidence to stand up to the insurance company. We will walk you through how to gather compelling evidence, build an undeniable case for your car’s true value, and handle the total loss settlement negotiation process like a pro, ensuring your voice is heard.

Key Takeaways

- Challenge the insurance company’s initial valuation: The first offer is a business calculation designed to save the insurer money, not a final verdict. Always review their valuation report for errors and prepare to counter with your own research.

- Prove your car’s value with solid documentation: Your negotiation strength lies in your evidence. Use maintenance records, receipts for recent upgrades, and photos to show your car was in above-average condition, justifying a higher settlement than the standard book value.

- Use your escalation options when negotiations stall: If the adjuster refuses to offer a fair amount, you are not out of options. You can use your policy’s appraisal clause, file a state complaint, or hire an attorney to take over the fight for you.

What Does “Total Loss” Actually Mean?

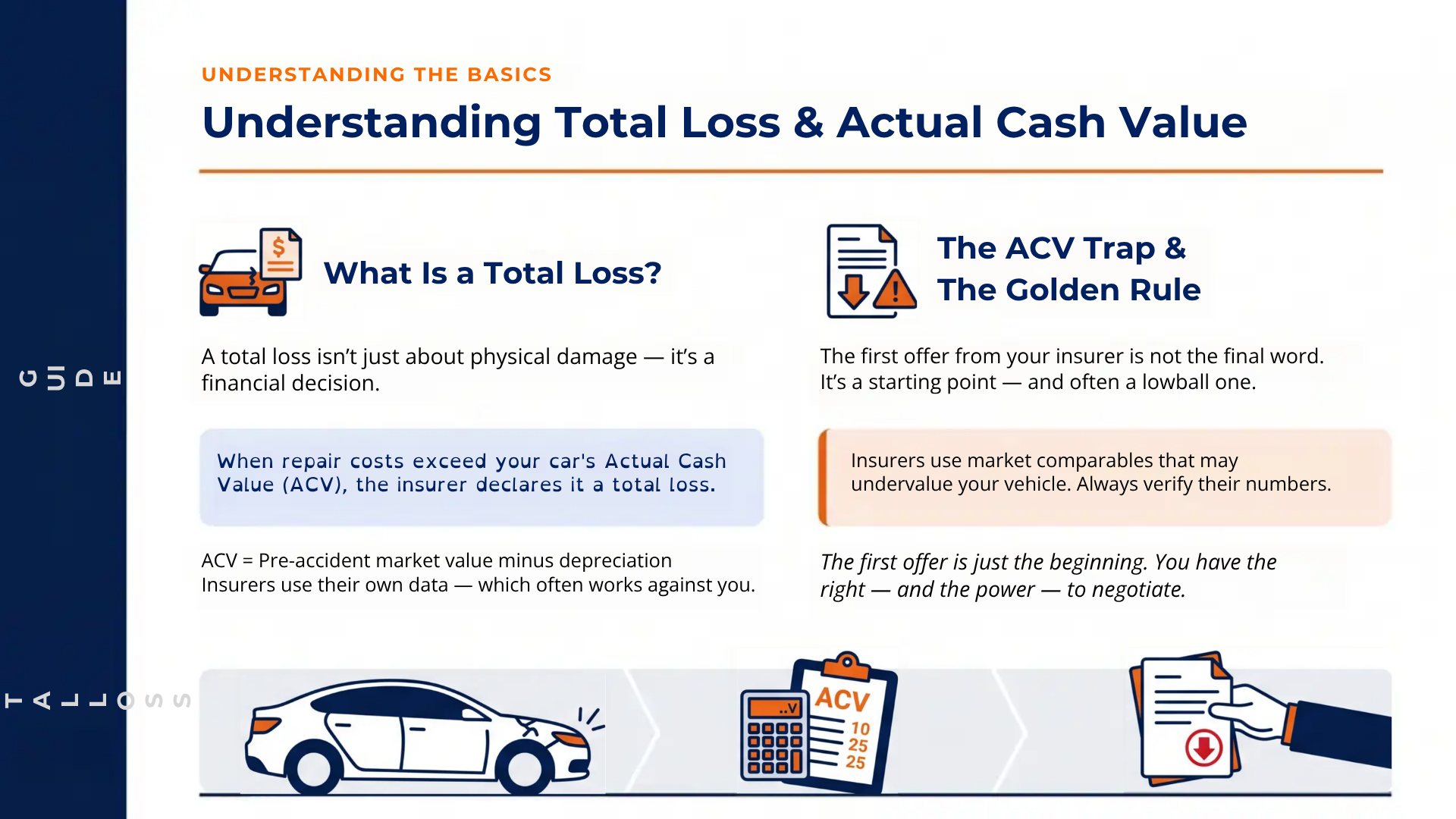

When you hear the phrase “total loss,” you probably picture a car that’s been completely mangled in a crash. While that’s sometimes the case, the term is actually a financial one that insurance companies use. A vehicle is declared a “total loss” when the estimated cost to repair it is more than its value was right before the accident. It’s a simple cost-benefit analysis for the insurer: is it cheaper to pay for the repairs, or is it more sensible to just pay you for the car’s value and take the damaged vehicle? In Georgia, this decision is often based on a specific formula, but the core idea is the same everywhere.

This pre-accident value is officially known as the Actual Cash Value, or ACV. Understanding your car’s ACV is the most important step in making sure you get a fair settlement from the insurance company. The entire negotiation will revolve around this number, so getting it right is crucial. It’s also important to know that even if your car is repaired instead of totaled, its resale value will likely take a hit. This is a separate issue known as diminished value, which is another type of claim you can make to recover that lost value. If your vehicle was repaired instead of totaled, speaking with an experienced Atlanta diminished value attorney may help you recover that additional loss. But for a total loss, the focus is entirely on getting the full pre-accident value of your car so you can replace it.

How Insurers Decide Your Car is a Total Loss

After an accident, the insurance company will assign an adjuster to your claim. The adjuster’s first job is to inspect your car and create a detailed estimate of what it will cost to fix all the damage. At the same time, they will research your vehicle to determine its Actual Cash Value (ACV) from the moment right before the crash occurred. To do this, they look at your car’s year, make, model, mileage, overall condition, and recent sales of similar cars in your local market. The decision then comes down to a simple comparison. If the repair estimate is higher than the ACV, they will declare the car a total loss. This is a critical part of the property damage claims process.

Actual Cash Value vs. Repair Costs

The biggest point of confusion for most people is the “Actual Cash Value.” It’s not what you originally paid for the car, and it’s not necessarily what a dealer would sell it for today. ACV is the car’s fair market value minus depreciation for its age, mileage, and general wear and tear. Insurance companies use their own formulas and market data to calculate this number, and their initial offer is often on the low side. Remember, their goal is to pay out as little as possible. You do not have to accept their first offer. You have the right to review their valuation and negotiate for a higher, more accurate settlement. If their number seems unfair, it’s a good idea to contact us to review your case.

Your Car is Totaled. Now What?

Hearing that your car is a total loss can feel like a punch to the gut. It’s stressful, and it’s easy to feel rushed into accepting whatever the insurance company offers first. But take a deep breath. This is the moment to slow down and get organized, because the steps you take next can make a huge difference in the amount of money you receive.

Before you even think about accepting a settlement, you need to do a little homework. The insurance adjuster has a process for determining your car’s value, but it’s not always accurate, and it’s definitely not designed to be in your favor. Your job is to build a strong case for what your car was actually worth. Think of yourself as your car’s advocate. By gathering the right documents and understanding the process, you can confidently challenge a lowball offer and fight for the compensation you deserve. Let’s walk through exactly what you need to do.

Get Your Paperwork in Order

First things first, it’s time to gather every piece of paper related to your car. This is your evidence. Collect receipts for any recent repairs, new tires, or upgrades you’ve made. Did you just get a new sound system or have the engine serviced? Find that paperwork. You’ll also want to pull together any photos or videos you have of your car from before the accident. These visuals are powerful proof of its condition. This documentation helps you build a complete picture of your car’s value, showing it was more than just a line item on a standard valuation report.

Review Your Insurance Policy

Your insurance policy is more than just a bill you pay each month; it’s a contract that outlines your rights. Get a copy of your policy and look for sections that talk about how disputes are handled. You’re specifically looking for terms like “appraisal” or “dispute resolution.” Many policies include an “appraisal clause,” which is a powerful tool if you and the insurer can’t agree on a settlement amount. This clause allows both you and the insurance company to hire independent appraisers to determine the value, giving you a fair path forward. Understanding these details is a key part of handling your property damage claim.

Get the Insurer’s Valuation Report

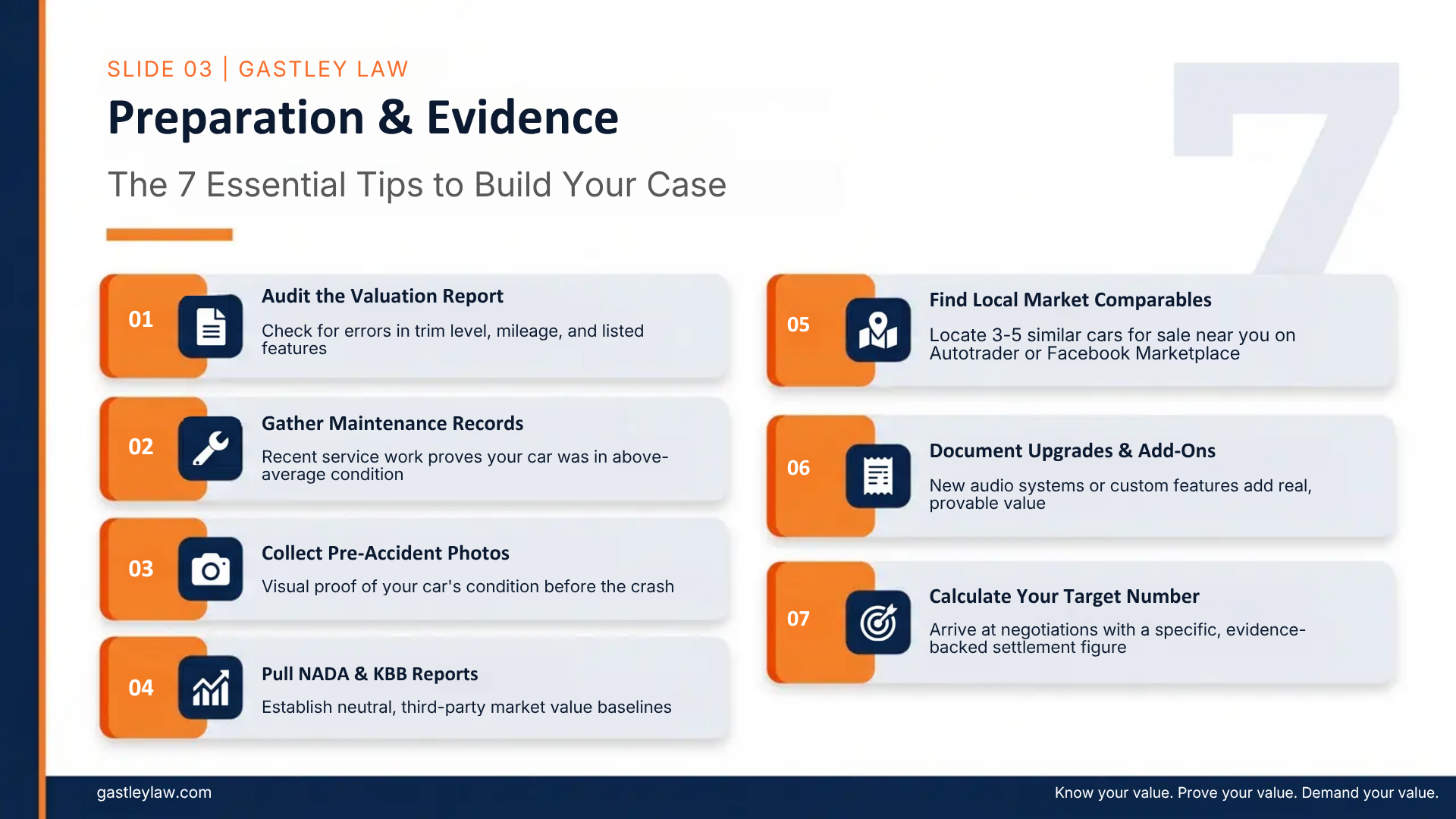

You can’t negotiate effectively if you don’t know how the insurance company arrived at their number. Always ask the adjuster for a complete copy of the valuation report. This document breaks down how they calculated your car’s value. Once you have it, go through it with a fine-tooth comb. Check for errors, because they happen all the time. Is the make, model, and trim level correct? Did they list all of your car’s features and optional packages? Is the mileage accurate? Any mistake, big or small, can lower the offer. If you find errors or need help understanding the report, don’t hesitate to contact us for a case evaluation.

How to Figure Out Your Car’s Real Value

The insurance adjuster’s first offer for your totaled car can feel like a final verdict, but it’s really just the opening line in a negotiation. Their number is based on their own valuation report, which often misses key details that made your car special. Your job is to show them what your car was actually worth right before the accident. This isn’t about what you feel it was worth; it’s about building a solid, evidence-based case for its true market value. Think of yourself as a detective gathering clues. You’ll need to pull together data from trusted guides, find real-world examples of similar cars for sale, and document every single thing that added value to your vehicle.

The goal is to present a counteroffer that is so well-supported by facts that the adjuster can’t ignore it. Insurance companies are required to make you whole, which means providing enough money to buy a comparable replacement vehicle in your local market. By doing your own research, you can hold them to that standard. It might sound like a lot of work, but each piece of evidence you find can add hundreds, or even thousands, of dollars to your final settlement. We’ll walk through exactly how to gather the proof you need to get the fair value you deserve for your car.

Start with NADA and Kelley Blue Book

Your first stop should be the big names in car valuation: the NADAguides and Kelley Blue Book (KBB). These online tools give you a baseline value based on your car’s make, model, year, mileage, and overall condition. Be honest about your car’s condition (or what it was before the crash) to get the most accurate starting number. While insurance companies often use these guides themselves, they might select a lower condition rating or overlook certain options. Getting your own report from both KBB and NADA gives you a solid, third-party reference point to begin your negotiation and challenge their initial assessment.

Find Similar Cars for Sale Near You

This step is one of the most powerful things you can do. The value of your car isn’t just a number in a book; it’s what it would cost to buy a similar one in your area right now. Hop onto sites like Autotrader, Cars.com, and even Facebook Marketplace to find vehicles for sale that are just like yours. Look for the same make, model, year, and similar mileage and features. Save screenshots of these listings, paying close attention to the asking prices. If you find several examples priced higher than the insurer’s offer, you have concrete proof that their valuation is too low for your local market.

Document Your Car’s Condition and Upgrades

Did you just buy new tires a month before the accident? Get a major service done? Add a new sound system? Every one of these things adds value, and the insurance company’s report probably missed them. Go through your records and gather receipts for any recent repairs, maintenance, or upgrades. Even regular oil change receipts can help show that your car was well-maintained. If you have any photos or videos of your car from before the crash, especially ones that show off its great condition or special features, get those ready too. This documentation helps prove your car was in better-than-average shape, which justifies a higher value. This is a key part of building a strong property damage claim.

What Paperwork Do You Need to Negotiate?

Walking into a negotiation with an insurance adjuster without proof is like showing up to a test without a pencil. You can’t expect to get the best result. The adjuster has a report full of data to justify their low offer, so you need to come prepared with your own evidence to prove what your car was really worth. Think of yourself as building a case for your vehicle. Your goal is to present a clear, logical argument backed by documents that show your car was in great shape, well-maintained, and has a higher market value in your local area than the insurance company claims.

Gathering this paperwork does more than just support your claim; it shows the adjuster that you’re serious and have done your research. It shifts the power dynamic from them simply telling you what your car is worth to you leading a conversation based on facts. This preparation is the foundation of a strong negotiation. With the right documents in hand, you can systematically counter their valuation and work toward a settlement that truly reflects your loss. If you find the process overwhelming, remember that expert help is available to handle these property damage claims for you.

Maintenance Records and Receipts

Did you buy new tires a few months before the accident? Get a major service done? Any money you recently invested in your car is proof of its condition and value, and you need the receipts to prove it. Insurance companies often value cars based on an assumed “average” condition. Your maintenance records are the perfect way to show your vehicle was above average.

Dig up receipts for oil changes, new brakes, a new battery, engine work, and any other repairs or upgrades. These documents create a timeline of care that justifies a higher valuation. Organize them by date to clearly show the adjuster that your car was a well-maintained, reliable vehicle right up until the moment of the crash.

Photos and Videos from Before the Accident

A picture really is worth a thousand words, especially when you’re trying to prove your car’s condition. The insurance adjuster never saw your car before the accident, so they have no idea if it was meticulously clean or had dents and scratches. Photos and videos are your visual proof. Scroll through your phone’s camera roll and social media feeds for any pictures where your car is visible.

Look for images that show off its clean interior, shiny paint, or any special features like custom wheels or a sunroof. Even a simple photo of your car parked in the driveway can help establish its pre-accident condition. This evidence makes it much harder for the adjuster to claim your car was in poor shape and helps you argue for its true value.

Local Car Listings and Market Data

This is one of the most powerful tools you have. The insurance company’s valuation is based on their own market survey, but it may not accurately reflect prices in your specific area. Your job is to find what a car just like yours is actually selling for nearby. This research gives you concrete evidence to support your counteroffer.

Search websites like Cars.com, AutoTrader, and even Facebook Marketplace for vehicles that are the same make, model, year, and trim as yours, with similar mileage. Save screenshots of at least three to five listings. This real-world data is your best evidence for proving the local market value and showing the adjuster their offer is too low.

How to Build Your Negotiation Strategy

Once you have the insurance company’s valuation report, you can start building your case. A strong negotiation strategy isn’t about being confrontational; it’s about being prepared. You need to approach the conversation with clear, documented evidence that supports a higher valuation for your vehicle. Think of it as presenting a logical argument that the adjuster can’t ignore. By doing your homework and organizing your facts, you shift the power dynamic and show the insurer you mean business. This preparation is the key to getting the fair settlement you deserve.

Break Down the Insurer’s Valuation Report

The first step is to ask the insurance adjuster for a complete copy of their valuation report. This document outlines exactly how they arrived at their settlement offer, including the comparable vehicles they used for their analysis. Don’t just accept their final number at face value. You need to see the data behind it to challenge it effectively. This report is the foundation of your negotiation, and reviewing it gives you the roadmap for your counteroffer. It shows you where they might have cut corners or used data that doesn’t accurately reflect your car’s true diminished value.

Pinpoint Errors and Inconsistencies

Carefully read through the insurer’s report, looking for any mistakes. Check that every detail about your car is correct, including the specific trim level, optional features, recent upgrades, and mileage. Insurance companies often use automated systems that can miss these important details. Next, scrutinize the “comparable” vehicles they listed. Are they truly similar to yours? Look them up to see if they are from your local market, have a clean title, and are actually available for sale. Often, insurers use comps that are base models or have a history of accidents to justify a lower offer. Finding these errors is your first line of defense.

Calculate Your Ideal Settlement Number

Before you even think about making a counteroffer, you need to determine how much you believe your car is worth. This isn’t a guess; it’s a number based on solid research. Search online listings from local dealerships and private sellers to find vehicles that are as close to yours as possible in terms of make, model, year, mileage, and condition. Save screenshots of these listings as evidence. Having a specific, evidence-backed number in mind gives you a clear goal for your negotiation. If your research leads to a number that’s far from the insurer’s offer, it might be time to contact a professional for help.

Smart Tactics for Negotiating Your Settlement

Once you have your evidence and your ideal settlement number, it’s time to negotiate. This can feel intimidating, but it’s a standard part of the claims process. The insurance adjuster’s first offer is just that: a starting point. With the right approach, you can successfully argue for a higher, fairer amount. The key is to be prepared, professional, and persistent. Let’s walk through the tactics that will help you get the compensation you deserve for your vehicle.

Write a Clear and Professional Counteroffer

Your first move is to respond to the insurance company’s low offer with a formal counteroffer letter or email. Putting your response in writing makes your position official and shows you’re serious. In this document, clearly state that you are rejecting their initial offer and explain why. Present your own valuation, supported by the evidence you’ve gathered. Keep the tone professional and business-like. This isn’t the place for angry rants; it’s about laying out the facts. A well-written counteroffer sets a strong foundation for the rest of the negotiation and creates a paper trail of your communications.

Present Your Evidence in a Logical Order

An adjuster is more likely to approve a higher amount if you make their job easy. Don’t just send a messy folder of links and receipts. Organize your evidence into a clear, logical package. Start with your valuation summary, then provide the supporting documents. For example, create a list of your comparable vehicle listings with screenshots and direct links. Follow that with your maintenance records and receipts for any upgrades. By presenting your case in a step-by-step manner, you help the adjuster understand and justify why your vehicle is worth more than their initial assessment. This shows you’ve done your homework and builds a compelling argument for your diminished value claim.

Be Persistent, Not Aggressive

Negotiation is a marathon, not a sprint. It requires persistence, but that doesn’t mean you need to be aggressive. Maintain a firm but polite tone in all your communications, whether on the phone or in writing. If the adjuster pushes back, calmly refer to your evidence and ask them to explain the specific data they used to justify their lower number. Don’t be afraid to follow up if you don’t hear back. Remember, this is a business transaction. Staying calm and focused on the facts will get you much further than losing your cool. If you find the back-and-forth draining, that’s a sign it might be time to get professional legal representation.

What to Do When the Insurance Company Says No

It can feel like hitting a brick wall when the insurance adjuster won’t budge on their low offer. After all the research and preparation you’ve done, a flat-out “no” is incredibly frustrating. But this isn’t the end of the road. You still have several powerful options to get the fair settlement you deserve.

Don’t let the insurance company have the final say. When negotiations stall, it’s time to shift your strategy. Instead of continuing to go back and forth with an adjuster who won’t listen, you can escalate the issue. Think of it as moving up to the next level of the game. You can invoke a specific clause in your policy, file an official complaint with the state, or bring in a legal professional to fight on your behalf. Let’s walk through what each of these steps looks like.

Use Your Policy’s Appraisal Clause

Did you know your policy might have a secret weapon? Buried in the fine print of many auto insurance policies is something called an “appraisal clause.” This is a powerful tool when you and the insurer agree that the car is a total loss but can’t agree on its value.

Here’s how it works: The clause allows both you and the insurance company to hire your own certified, independent appraisers. Those two appraisers then select a neutral third appraiser, known as an umpire. The umpire reviews the findings from both sides and makes a final, binding decision on your car’s value. It’s a formal process that takes the decision out of the adjuster’s hands and puts it into the hands of neutral experts. Check your policy documents to see if you have this option.

File a Complaint with the State

Insurance companies are regulated by the state, and there’s an official body designed to protect you. If you believe your insurer is acting in bad faith, dragging out the process, or simply not treating you fairly, you have the right to file a formal complaint.

In Georgia, you can file a complaint with the Office of Insurance and Safety Fire Commissioner. This government agency will investigate your claim and can mediate the dispute. Sometimes, just the act of filing an official complaint is enough to get the insurance company to take your claim more seriously and come back to the table with a much more reasonable offer. It’s a free and effective way to add pressure and hold them accountable for their decisions.

Know When It’s Time to Call a Lawyer

If you’ve presented all your evidence and the insurance company still refuses to offer a fair settlement, it might be time to bring in a professional. When negotiations get tough or the offer is just too low, an experienced attorney can make all the difference. They aren’t intimidated by adjusters because they deal with them every single day.

A lawyer who specializes in property damage and diminished value claims understands the tactics insurers use to minimize payouts. They can take over all communication, present your case forcefully, and fight for the full amount you’re owed. You don’t have to accept a lowball offer, and you don’t have to fight this battle alone. If you’re ready for support, we’re here to evaluate your case.

Common Mistakes That Can Lower Your Settlement

Navigating a total loss claim can feel overwhelming, and it’s easy to make a misstep that costs you hundreds or even thousands of dollars. Insurance adjusters handle these claims every day; you don’t. But by knowing what to watch out for, you can protect your interests and stand firm in your pursuit of a fair settlement. Avoiding these common mistakes is the first step toward getting the full amount you’re owed for your vehicle. Let’s walk through the most frequent pitfalls and how you can sidestep them.

Accepting the First Lowball Offer

After a wreck, you just want to get things over with. It’s tempting to accept the first settlement offer the insurance company puts on the table just to move on. Please don’t. Remember, insurance companies are for-profit businesses, and their initial offer is often a starting point for negotiations, not their final number. They expect you to negotiate. Accepting that first lowball offer means leaving money on the table that you are rightfully owed. Take a deep breath, thank the adjuster for the offer, and tell them you need time to review it carefully before making a decision. This gives you the space to build your counteroffer without feeling pressured.

Ignoring Errors in the Valuation Report

The insurance company’s settlement offer is based on a detailed valuation report. This document lists your car’s specs, including its trim level, mileage, condition, and any special features. It’s incredibly common for these reports to contain errors. An adjuster might list your car as a base model when it’s a premium trim, or they might overlook recent upgrades like new tires. These small mistakes can significantly reduce your car’s value. Scrutinize every line of that report. If you find inaccuracies, gather your proof (like receipts or the original window sticker) and point them out. Having an expert review the report can also uncover hidden errors, which is a key part of our legal representation.

Talking to the Adjuster Unprepared

Never get on the phone with an insurance adjuster without doing your homework first. If you don’t know what your car is actually worth, you have no foundation to negotiate from. Before you discuss numbers, you should have already researched your vehicle’s value using resources like NADAguides and found comparable vehicles for sale in your area. When the adjuster calls, you should have your own ideal settlement figure in mind, supported by solid evidence. Walking into the conversation prepared shows the insurance company that you’re serious and won’t be easily swayed by a low offer. It shifts the power dynamic and puts you in a much stronger position to negotiate effectively.

Related Articles

- Car Accident Settlement Negotiations in Georgia

- Diminished Value Claims in Georgia

- What to Do If You Don’t Agree With a Total Loss Adjuster

- How to Get a Fair Settlement for Car Damage

Frequently Asked Questions

What if I still owe more on my car loan than the settlement offer?

This is a tough situation, and it’s more common than you might think. If your settlement doesn’t cover your auto loan, you are still responsible for paying off the remaining balance. This is often called being “upside down” on your loan. Some auto insurance policies offer optional “gap insurance” which is designed specifically to cover this difference. If you have gap insurance, now is the time to start that claim. If not, you will need to work with your lender to figure out a plan to pay the rest of the loan.

Can I decide to keep my car even if it’s declared a total loss?

Yes, in most cases you have the option to keep your vehicle. If you choose to do this, the insurance company will pay you the actual cash value of the car minus its salvage value (what they would have gotten for it at a salvage auction). However, the car will be issued a “salvage title,” which can make it difficult to insure and register in the future. You would also be responsible for arranging and paying for all repairs yourself, which can be a complicated and expensive process.

How is a total loss claim different from a diminished value claim?

A total loss claim happens when your car is too damaged to be repaired, and the insurance company pays you for the car’s pre-accident value. A diminished value claim, on the other hand, applies when your car is repaired after an accident. The claim is for the loss in resale value your car suffers simply because it now has an accident history. Even if it’s perfectly fixed, a car with a wreck on its record is worth less than one without, and a diminished value claim helps you recover that financial loss.

The insurance company’s “comparable” cars aren’t really like mine. What do I do?

This is a very common negotiation tactic. If the insurer’s comparable vehicles are a lower trim level, have higher mileage, or are located far from your local market, you need to point it out. Your job is to find better, more accurate comps. Present the adjuster with your own list of vehicles for sale in your area that are a much closer match to your car’s specific features and condition. This direct, evidence-based comparison makes it much harder for them to justify their low valuation.

How long should I wait for the insurance company to respond to my counteroffer?

After you send your written counteroffer with all your supporting evidence, give the adjuster a reasonable amount of time to review it, perhaps three to five business days. If you haven’t heard back by then, it’s perfectly acceptable to send a polite follow-up email or make a phone call. Just ask if they’ve had a chance to review the information you sent and if they have any questions. Persistence is key, so don’t be afraid to check in regularly until you get a response.