After a car accident, you expect the insurance company to make things right. But when you get their offer for your car’s lost value, the number can be shockingly low. More often than not, the reason for that lowball figure is a calculation called the 17c diminished value formula. This isn’t some universal law of physics; it’s a method created by an insurance company to standardize payouts in a way that consistently benefits them. It’s designed to look official and fair, but it’s built on a foundation of arbitrary caps and flawed logic that almost always undervalues your vehicle. Understanding how this formula works is the first and most critical step in challenging their offer and fighting for the compensation you are actually owed.

If you’ve filed an insurance claim for vehicle damage, you might hear the term “17c formula.” In short, it’s a calculation insurance companies often use to determine your car’s diminished value after an accident. The formula was created by an insurance company, and it’s designed to standardize the payout process. While that might sound fair on the surface, the formula has some serious flaws that almost always favor the insurer, not you.

The calculation itself involves three main steps. First, the insurer takes your car’s market value (often from a source like Kelley Blue Book) and caps the maximum potential loss at 10%. This becomes the “base loss.” Next, they apply a “damage multiplier,” a number that adjusts the value based on how severe the damage was. Finally, they apply a “mileage multiplier,” which reduces the amount even further based on how many miles are on your car. The final number is what the insurance company will likely offer you for your diminished value claim. It’s important to understand how this formula works because it’s often the basis for the first, and usually very low, offer you’ll receive.

The 17c formula isn’t just some random calculation; it has specific roots right here in Georgia. The name comes from a court case involving State Farm, where the insurance company developed this method to create a consistent way to calculate diminished value payouts for claimants. The goal was to turn a complex assessment into a simple, repeatable math problem.

While creating a standard is a logical business move, the formula was built to protect the insurance company’s bottom line. It was never designed to accurately reflect the true market value a car owner loses after an accident. Since its creation, many insurance companies have adopted it or similar versions because it provides a predictable, and often very low, figure for their claim payouts.

Insurance companies love the 17c formula for one simple reason: it saves them money. The entire calculation is built around limitations that reduce the final payout. The most significant of these is the 10% cap on the base value loss. Before any other factors like damage severity or mileage are even considered, the formula assumes your car could not have possibly lost more than 10% of its value.

This arbitrary cap rarely reflects reality. A luxury vehicle or a newer car can lose far more than 10% of its value from an accident showing up on its vehicle history report. By starting with this low ceiling, insurers can present you with a calculation that looks official and fair but is actually designed to undervalue your claim from the very beginning. Challenging this formula is a key part of our legal representation and is essential to getting the full compensation you deserve.

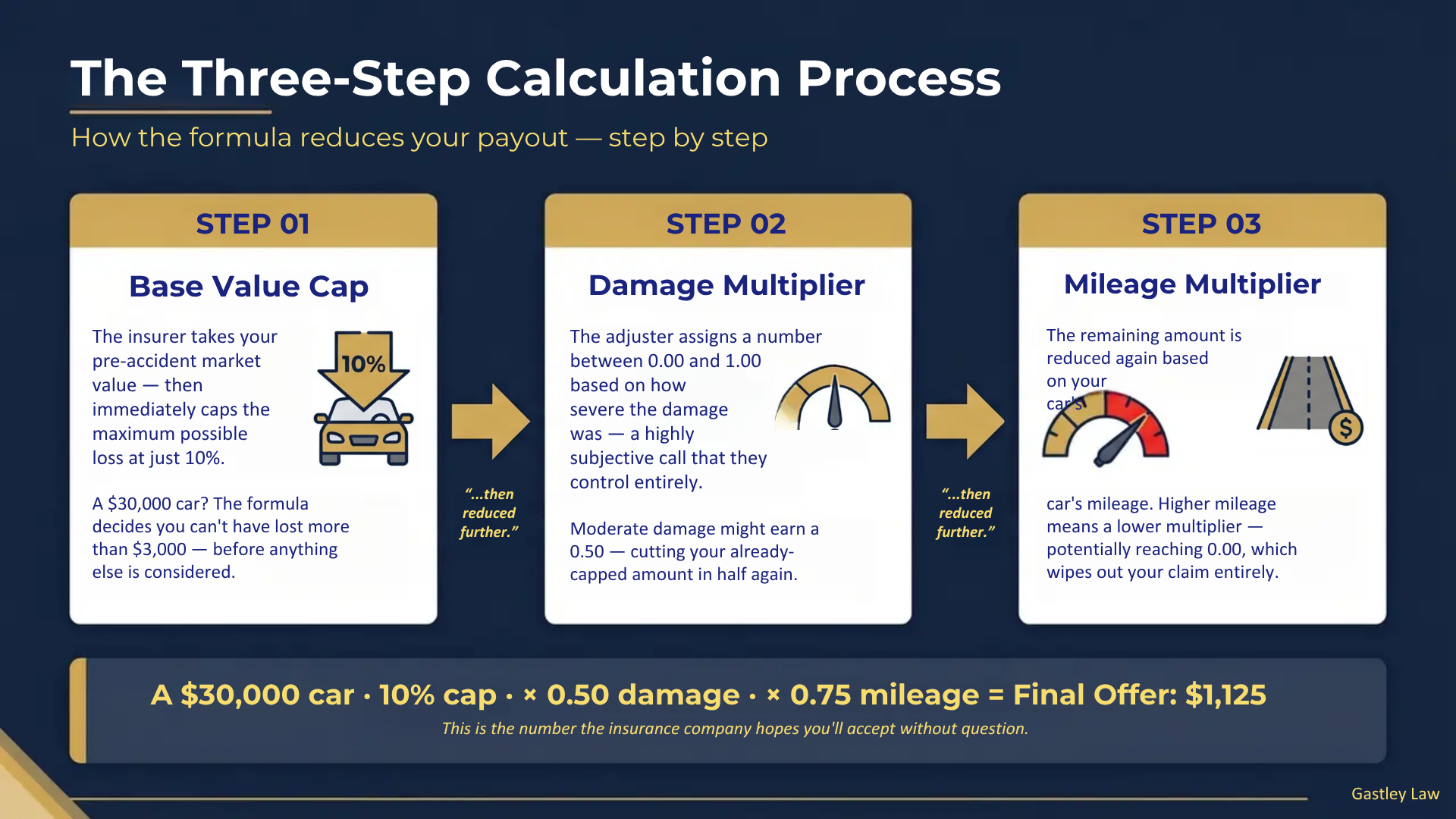

Insurance companies, especially in Georgia, often turn to the 17c formula to figure out how much they owe you for your car’s diminished value. While it sounds official, it’s really just a three-step calculation they use to standardize their payouts. Understanding how it works is the first step in recognizing a lowball offer when you see one. The formula essentially takes a percentage of your car’s value and then reduces it based on the severity of the damage and your vehicle’s mileage.

Think of it as the insurance adjuster’s playbook. They plug in the numbers, and it spits out a figure that, more often than not, benefits them more than it does you. Knowing these steps helps you see exactly where they might be undervaluing your claim. Let’s walk through how they arrive at their number so you can be prepared to challenge it.

First, the insurance company establishes your car’s pre-accident value. You can find a rough estimate of your car’s worth using resources like Kelley Blue Book. The 17c formula then immediately caps the maximum possible loss at 10% of that value. For example, if your car was worth $30,000 before the accident, the calculation starts with a maximum diminished value of $3,000. This 10% cap is one of the biggest problems with the formula, as the actual drop in market value is often much higher, especially for newer cars or vehicles with significant damage.

Next, that initial 10% figure is multiplied by a “damage multiplier.” This is a number between 0.00 and 1.00 that the insurer assigns based on the severity of the damage. A higher number is supposed to reflect more serious damage. For instance, severe structural damage might get a 1.00 multiplier, while moderate panel damage could be rated at 0.50. If your car had $3,000 as its base value loss and received a 0.50 damage multiplier, the amount is now cut in half to $1,500. This step is highly subjective and gives the adjuster a lot of control over the final payout.

Finally, the number is reduced again with a mileage multiplier. This adjustment is based on the idea that cars with higher mileage have already depreciated, so their diminished value loss is smaller. The multiplier is another scale from 0.00 to 1.00. A car with under 20,000 miles might have a 1.00 multiplier (no reduction), but a car with over 100,000 miles could have a 0.00 multiplier, wiping out the claim entirely. Using our example, if the $1,500 figure is multiplied by a mileage factor of 0.75, your final diminished value offer would be just $1,125.

On the surface, the 17c formula looks like a simple, standardized way to figure out your car’s lost value. Insurance companies often present it as the official method for calculating your payout. However, when you look closer, you’ll find several built-in flaws that almost always work in the insurer’s favor, not yours. These issues can drastically reduce the amount of money you receive, leaving you to cover the real financial loss. Let’s break down exactly where this formula misses the mark and why it’s so important to challenge it.

The biggest issue with the 17c formula is its very first step. It automatically caps the maximum possible loss at just 10% of your car’s pre-accident value. Think about that for a moment. If your car was worth $40,000 before the crash, the formula decides the absolute most it could have lost in value is $4,000, even before any other deductions are made. This is an arbitrary limit that doesn’t reflect reality. A vehicle with significant frame damage or a history of major repairs will lose far more than 10% of its value on the open market. This initial cap is the primary reason why so many diminished value offers feel unfairly low.

The 17c formula has a strange way of accounting for mileage that ends up penalizing you twice. First, your car’s starting value, usually taken from a guide like NADA, already reflects its mileage. A car with 80,000 miles is naturally valued lower than the same model with only 20,000 miles. The formula, however, takes this already reduced value and then applies a second reduction based on mileage. It’s like getting a discount on an item at the store, and then having the cashier apply the same discount again to your final, lower price. This double-dip on mileage unfairly lowers your car’s value and, consequently, your final payout.

Another misleading part of the formula is its use of “retail value.” The formula starts its calculation using the retail price of your car, which is what a dealer would sell it for on their lot. This sounds good, but it doesn’t match the real world for a private owner. You can’t sell your car for the same price a dealership can. Dealers offer financing, warranties, and a trusted name that private sellers simply can’t compete with. When you go to sell or trade in your repaired vehicle, you’ll be offered a price based on its private-party or trade-in value, which is always lower than retail. The formula ignores this crucial difference.

The timing of the valuation also creates a problem. The 17c formula calculates your car’s value at the time you file the claim, not at the time the accident actually happened. Weeks or even months can pass between the crash, the repairs, and the final claim processing. During that time, your car continues to depreciate naturally. By using the later date, the formula starts with a lower initial value, which means your final diminished value payment will also be lower. Any delays, whether for repairs or paperwork, end up benefiting the insurance company. If you’re facing these kinds of delays, it might be time to contact an expert for help.

Insurance companies didn’t adopt the 17c formula because it’s the most accurate way to measure your car’s lost value. They use it because it’s predictable, simple, and consistently produces low numbers that protect their bottom line. For them, it’s a tool to standardize claims and minimize payouts. They can plug in a few numbers, generate an offer, and present it as a data-driven result, hoping you won’t question it.

Understanding their strategy is the first step toward building a strong claim. Insurers rely on the formula’s official-sounding name and structure to convince you that their offer is fair and final. They count on you not knowing that the formula itself is fundamentally flawed and designed to undervalue your vehicle from the very beginning. By knowing how they use it, you can prepare to counter their arguments and fight for the compensation you actually deserve for your diminished value claim.

The primary way insurance companies use the 17c formula is to justify a low settlement offer. The formula’s structure is set up to limit your payout from the start. It begins by capping the maximum possible loss at just 10% of your car’s pre-accident value. This arbitrary cap often has no connection to the real-world market depreciation your car will suffer, especially if it sustained significant damage.

From there, the formula applies multipliers for damage and mileage that reduce the payout even further. An adjuster can present you with a calculation that looks methodical and fair, but it’s based on a foundation that guarantees a low number. It’s a strategic move to anchor the negotiation in their favor, starting you at a figure that is far below what your claim is likely worth.

When an insurance adjuster presents you with a diminished value amount calculated using the 17c formula, they often frame it as a final, take-it-or-leave-it offer. They might say, “This is what the formula shows,” implying that the number is a non-negotiable result of a standard industry calculation. This is a tactic designed to make you feel powerless.

Remember, the 17c formula is not a law in Georgia. It is simply an internal tool used by insurers. You should treat their initial offer as what it is: a starting point for negotiation. It’s the lowest amount they hope you’ll accept, not the final amount you are owed. Our firm specializes in challenging these lowball offers and demonstrating the true loss in your vehicle’s value through our legal representation.

Insurers often rely on a few key myths to support their low 17c-based offers. One common myth is that there’s no diminished value if the damage was purely cosmetic or if panels were replaced. However, any accident history, even with perfect repairs, can lower a car’s resale value because buyers will always prefer a vehicle with a clean record.

Another misleading point is the use of “retail value” in their calculations. They might value your car based on what a dealer would sell it for, but as a private owner, you can’t command that same price. You typically get less when selling privately or trading in, so their starting value is already flawed. If an adjuster is using these arguments, it’s a clear sign that you need to push back and get a professional evaluation.

On the surface, the 17c formula looks like a simple, objective way to calculate your car’s lost value. Insurance companies certainly present it that way, often acting as if it’s an industry standard that can’t be questioned. But when you look closer, you’ll find several issues that consistently work in their favor, not yours. The formula is less of a fair calculator and more of a tool designed to minimize the amount of money they have to pay you. It contains built-in caps and multipliers that often produce a number far below what your vehicle has actually lost in market value after an accident.

These flaws aren’t just small details; they can cost you thousands of dollars. The formula penalizes you for things that are already accounted for, like mileage, and completely ignores critical factors that any real car buyer would care about, such as the quality of repairs and the severity of the accident. It’s a one-size-fits-all approach that fails to capture the unique circumstances of your vehicle and its specific damage. Understanding these problems is the first step toward challenging a lowball offer and fighting for the compensation you deserve. Let’s break down the biggest issues you’re likely to face when an insurer uses the 17c formula for your claim.

If you own a newer or more expensive vehicle, the 17c formula is particularly unfair. It starts by capping the initial loss at 10% of the car’s pre-accident value, which is an arbitrary limit that doesn’t reflect reality. A luxury car or a brand-new truck can lose much more than 10% of its value just by having an accident on its vehicle history report. Potential buyers are especially wary of accident histories on high-end cars, leading to a steep drop in what they’re willing to pay. The formula simply doesn’t account for this significant market reality, resulting in an offer that falls short of your car’s true diminished value.

The 17c formula essentially penalizes you twice for your car’s mileage. Here’s how it works: the starting value of your car, often taken from a guide like NADA, has already been adjusted downward for its mileage. A car with 80,000 miles is naturally worth less than the same model with 20,000 miles, and that’s reflected in its base value. However, the 17c formula then applies a second reduction based on that same mileage. This “mileage multiplier” further decreases your payout for a factor that was already considered. It’s a flawed method that unfairly lowers your claim, and it’s one of the key areas where our legal representation can challenge the insurer’s math.

One of the most illogical parts of the 17c formula is how it handles the actual damage. The formula often disregards the extent of the repairs, even though this is a huge factor for any potential buyer. It might classify damage as “minor” even if the repair bill was thousands of dollars. It also fails to recognize that repaired parts are never the same as factory-installed ones. A car with replaced panels or structural repairs, no matter how well done, is less valuable than one with its original factory components. The formula’s failure to consider the real-world impact of an accident history and the quality of repairs means its final number rarely reflects your car’s actual loss in value.

Relying on the insurance company’s 17c formula calculation is like letting the other team’s coach be the referee. It’s not in your best interest. The good news is that you don’t have to accept their number. There are far more accurate and fair methods to determine how much value your car has actually lost. Taking the initiative to get your own valuation is the first step toward securing the compensation you deserve. These methods provide a realistic picture of your car’s post-accident market value, giving you the solid evidence needed to counter a lowball offer.

The most powerful tool you have is an expert opinion. Hiring a professional, independent appraiser gives you a detailed and unbiased valuation of your vehicle’s diminished value. Unlike the insurance adjuster, who works for the insurance company, an independent appraiser works for you. They will thoroughly inspect your car, consider the specifics of the damage and repairs, and analyze current market trends to provide a precise assessment. This professional report carries significant weight in negotiations and is a crucial piece of evidence if you need to pursue specialized legal representation. It replaces the insurer’s generic formula with a real-world valuation based on your specific car.

Another effective strategy is to conduct a comparative market analysis. This approach grounds your claim in real-time market data. The process is straightforward: you research the selling price for cars that are the same make, model, year, and mileage as yours but have a clean accident history. Then, you find comparable vehicles that have a reported accident on their record. The difference between these two prices is a strong indicator of your car’s diminished value. This method clearly shows how much less a buyer would be willing to pay for your car now that it has an accident history, providing a practical basis for your claim.

While the 17c formula is deeply flawed, understanding its components can actually work in your favor. The formula relies on a base loss value, a damage multiplier, and a mileage multiplier to arrive at a final number. By learning how your insurance company applied these factors, you can pinpoint where they undervalued your claim. Was the initial value of your car too low? Did they apply an unfairly harsh damage multiplier? Knowing the logic they used allows you to build a targeted counterargument and challenge their assessment on their own terms. It’s less about using the formula yourself and more about deconstructing their offer to prove it’s inadequate.

Receiving a lowball offer based on the 17c formula can feel defeating, but it’s important to remember that this is just the insurance company’s starting point. You don’t have to accept it. With the right preparation and evidence, you can effectively challenge their number and fight for the compensation you truly deserve. The key is to build a case that’s stronger than their formula.

This involves gathering solid proof of your car’s value, presenting a more accurate calculation of its diminished value, and confidently negotiating with the insurer. Think of it as a business transaction where you need to prove your position with facts. By taking a systematic approach, you can counter their low offer and work toward a fair settlement for your diminished value claim. Let’s walk through the steps you can take to make that happen.

The foundation of a strong diminished value claim is thorough documentation. Before you can argue for a higher payout, you need proof to back up your position. Start collecting every piece of paper related to the accident and your vehicle from the very beginning. This includes the official accident report, all repair bills and invoices, and any estimates of your car’s value before the crash from sources like Kelley Blue Book. Keep a dedicated folder for these documents, both physical and digital. This organized evidence is your best tool for showing the insurance adjuster exactly what your car was worth and what it took to repair it.

To get more money, you need stronger proof than the 17c formula provides. The most effective way to do this is with a market comparison. Start by looking up the sale prices for cars just like yours (same year, model, features, and similar mileage) that have a clean history. Then, find comparable cars that have been in an accident. The price difference between these two groups is a real-world demonstration of your car’s diminished value. For the strongest case, consider hiring a licensed, independent appraiser who specializes in diminished value. Their expert report carries significant weight and is much harder for an insurance company to dismiss than a simple formula.

The insurance company’s initial offer is just that: an offer. It is not the final word, and you have every right to negotiate for a better one. Once you have your documentation and an independent appraisal, present your evidence to the adjuster in a clear and organized way. Be firm and professional, explaining why their 17c calculation is inaccurate and how your evidence supports a higher amount. Insurance companies often expect you to negotiate. If they refuse to offer a fair settlement or the process becomes too stressful, don’t hesitate to get legal help. An experienced attorney can handle the negotiations for you and ensure your rights are protected. If you feel you’ve hit a wall, you can always contact us for guidance.

Dealing with an insurance company after an accident can feel like an uphill battle, especially when they present you with a low offer based on the 17c formula. While you can try to negotiate on your own, there are specific moments when bringing in a legal expert is the best move you can make. A lawyer can level the playing field and show the insurer that you won’t be pushed around. If you find yourself in any of the following situations, it’s a good sign that you need professional help to protect your rights and your car’s value.

This is the most obvious red flag. If the insurance adjuster denies your diminished value claim outright or sends you a check that barely covers a tank of gas, don’t just accept it. Insurance companies often rely on the hope that you’ll be too tired or intimidated to fight back. A lowball offer is a negotiation tactic, not a final decision. Bringing in an attorney signals that you are serious about receiving fair compensation. Working with an experienced Atlanta diminished value attorney can strengthen your claim and help counter unfair valuation tactics. We can step in, handle all communication, and build a case that forces the insurer to re-evaluate their unfair offer.

Your car’s lost value is often just one piece of the puzzle. Did the collision leave you without a vehicle for weeks? You could have a loss of use claim. Are you unhappy with the quality of the repairs? That’s another issue. If you were injured, that adds another layer entirely. A skilled attorney can look at your situation as a whole and bundle these different claims together. This creates a much stronger negotiating position than fighting for each item separately. Our team handles all types of property damage claims, ensuring no money is left on the table.

Let’s be honest: filing claims, documenting evidence, and arguing with adjusters is exhausting. It’s a full-time job you didn’t ask for. If you feel stressed, confused by the jargon, or simply don’t have the time to handle it, that’s a perfectly valid reason to seek help. A lawyer takes that entire burden off your shoulders. We manage the paperwork, the phone calls, and the negotiations so you can focus on your life. You don’t have to become an expert in insurance law overnight. If you’re ready to hand the fight over to a professional, contact us for a consultation.

No, it is not. This is a common misconception that insurance companies are happy to let you believe. The 17c formula is simply an internal tool created and used by insurers to standardize their process and keep payouts low. You are not obligated to accept a settlement based on this calculation, and you have every right to challenge it with a more accurate, real-world valuation of your car’s lost value.

Insurance companies use the 17c formula because it is designed to save them money, not to give you a fair payout. The formula starts with an arbitrary 10% cap on your car’s value and applies other reductions that don’t accurately reflect the market. Trusting their initial offer is like accepting the first price on a used car without negotiating; you’re almost certainly leaving money on the table.

This depends on your specific insurance policy. In Georgia, you typically file a diminished value claim against the at-fault driver’s insurance. If you were at fault, you generally cannot claim diminished value from your own collision coverage. However, every policy is different, so it’s always a good idea to review your coverage details or consult with an expert to understand your options.

The most effective step you can take is to get an independent appraisal. An expert report from a licensed appraiser provides a detailed, unbiased valuation of your car’s true diminished value based on its specific damage and current market conditions. This professional document replaces the insurer’s flawed formula with hard evidence, giving you a much stronger position for negotiation.

Hiring a lawyer can be a smart move, especially if the insurance company is denying your claim, refusing to negotiate, or if the value of your claim is significant. An attorney takes the stress of dealing with the insurer off your shoulders and shows them you are serious about getting a fair settlement. They can handle all the communication and legal arguments needed to fight for the full amount you are owed.