Many people believe that as long as the insurance company pays for repairs, they’ve been made whole. Unfortunately, that’s a costly misconception. Even if your car is restored to pristine condition, its value is permanently damaged because it now has an accident history. Potential buyers will always choose a car with a clean record over one that’s been in a wreck, or they’ll expect a steep discount. This car value loss after accident is a legitimate damage you can and should be compensated for. This article will explain the different types of diminished value and show you how to fight for the money you’re owed.

Let’s start with the basics. Diminished value is the loss in your car’s market value after it’s been in an accident. Even if your car is repaired to look and drive like new, it’s now worth less than it was before the crash. Why? Because it has an accident history. When you decide to sell or trade in your vehicle, potential buyers will see that accident on a vehicle history report, like Carfax, and they won’t be willing to pay top dollar for it.

Think of it this way: if you were choosing between two identical used cars, but one had a clean record and the other had been in a wreck, you’d almost certainly choose the one with no accident history. Or, at the very least, you’d expect a significant discount on the one that was repaired. That discount is the diminished value. It’s a real financial loss you suffer simply because the accident happened, and it’s something you can and should be compensated for.

It’s easy to confuse diminished value with the cost of repairs, but they are two separate things. The insurance company pays a body shop to fix the dents, replace the bumper, and make your car look whole again. Those are repair costs. Diminished value, on the other hand, is the invisible loss that remains after the repairs are complete. It’s the permanent hit to your car’s resale value caused by the stigma of its accident history.

Even with the best repairs, the car is no longer what it was. The fact that it was damaged and rebuilt makes it less desirable to future buyers. Insurance companies are responsible for making you whole after an accident, and that includes covering this loss in market value, not just the bill from the mechanic. Our legal services focus on making sure you get compensated for both.

Diminished value isn’t just one single concept; it can be broken down into a few categories. Understanding them can help you see exactly what you’re owed.

It’s the question every car owner asks after a collision: even with perfect repairs, how much is my car really worth now? The unfortunate truth is that a vehicle’s value drops the moment an accident is reported. This loss in market value is known as diminished value, and it’s completely separate from the cost of repairs. Even if your car looks and drives like new, its history now includes a collision, making it less attractive to future buyers.

So, what kind of financial hit are we talking about? Generally, a car can lose anywhere from 10% to 30% of its pre-accident value, and in cases with significant damage, that number can climb even higher. For a car worth $20,000 before the wreck, that’s a loss of $2,000 to $6,000 that you’re left with. Insurance companies are supposed to compensate you for this loss, but they often don’t make it easy. Understanding the factors that contribute to this drop is the first step in getting the full compensation you deserve for your property damage claim.

While there isn’t a single formula to calculate value loss, the 10% to 30% range is a reliable starting point. This percentage can be influenced by the type of vehicle you drive. For example, newer cars, luxury brands, and electric vehicles often see a steeper drop in value. Buyers in these markets expect a clean history, so an accident record can be a major deal-breaker. A potential buyer comparing two identical cars will almost always choose the one without an accident history, forcing you to lower your price significantly to compete. This reality is the core of your diminished value claim.

The exact amount of value your car loses depends on a few key factors. The most obvious one is the severity of the damage; a minor fender bender won’t have the same impact as a collision that caused structural damage. Your car’s age, mileage, and overall condition before the accident also play a major role. However, one of the biggest factors is simply the accident history itself. Once a collision is listed on a vehicle history report, it creates uncertainty for future buyers. They may worry about hidden issues or the quality of the repairs, making them unwilling to pay full market price. This is precisely the diminished value you are entitled to recover.

Even after your car has been restored to look brand new, its market value takes a permanent hit. This frustrating reality is known as diminished value, and it happens because the accident becomes a permanent part of your vehicle’s story. No matter how flawless the repairs are, potential buyers will always see the car as having a history, which makes them less willing to pay top dollar.

This loss isn’t just theoretical; it’s a tangible financial setback that you shouldn’t have to absorb, especially if the accident wasn’t your fault. Understanding the reasons behind this drop in value is the first step toward recovering the money you’re rightfully owed. The stigma of the accident, concerns about safety, and official vehicle reports all play a role in defining your car’s new, lower market price.

The biggest reason for a car’s value drop is the simple fact that it now has an “accident history.” Think of it from a buyer’s perspective. If you were choosing between two identical cars, but one had been in a wreck, you would almost certainly choose the one with a clean record or expect a significant discount on the other. This permanent mark on the car’s record creates a stigma. Even with perfect repairs, the diminished value is the financial loss resulting from this buyer hesitation. The accident history makes buyers less trusting, and that lack of trust directly translates into a lower selling price for you.

Potential buyers often worry about what they can’t see. Even with a clean bill of health from a mechanic, they may have nagging questions about the car’s long-term reliability and safety. Was the frame’s structural integrity compromised? Could there be hidden damage that will cause problems down the road? These lingering concerns are valid, as a serious collision can affect a vehicle in ways that aren’t always obvious. Because of this uncertainty, buyers are rarely willing to pay the full pre-accident price for a car that has been in a crash. They are essentially pricing in the risk of future issues, which lowers the car’s overall market value.

In the past, a car’s accident history might have been harder to uncover. Now, it’s public information. Vehicle history reports from services like Carfax and AutoCheck make it easy for any potential buyer to see if a car has been in a reported accident. Once an accident is on the record, it stays there forever. This report is often the first thing a savvy buyer checks. Studies have shown that cars with an accident on their record can sell for thousands less than their counterparts with a clean history. This documented history provides concrete proof of the accident, making it nearly impossible to sell the car for its pre-accident value.

After a car accident, it’s natural to wonder just how much your vehicle’s value has dropped. The answer isn’t a simple one-size-fits-all number. Instead, the loss in value is determined by a combination of factors that insurance companies and potential buyers will scrutinize. Understanding what diminished value is and how it’s calculated is the first step toward recovering the money you’re rightfully owed. This isn’t about the cost of repairs; it’s about the permanent financial hit your car takes simply because it now has an accident in its history.

Think of it like this: two identical cars could be in similar accidents but end up with vastly different diminished value amounts. Why? Because the specifics matter. A dented bumper on a ten-year-old sedan won’t have the same financial impact as frame damage on a brand-new luxury SUV. Insurance adjusters will look at the severity of the damage, your car’s specific characteristics like its age and model, and the quality of the repair work. Each of these elements plays a crucial role in the final calculation, and knowing how they work together will help you build a stronger claim. It’s not just about getting the car fixed; it’s about being compensated for the permanent hit to its market value, a loss that stays with the car long after it leaves the body shop.

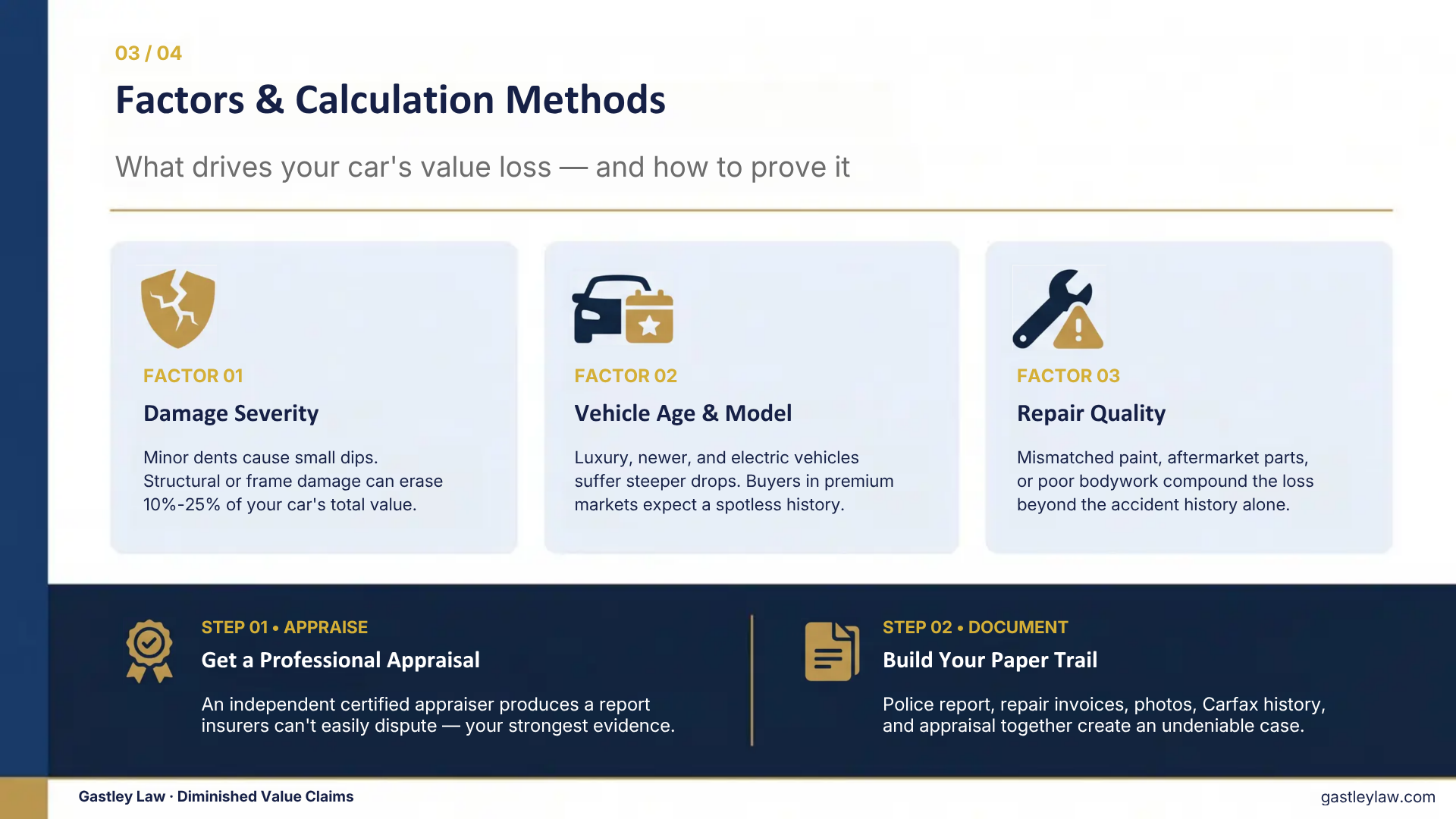

The single biggest factor influencing your car’s value loss is the extent of the damage it sustained. Minor cosmetic issues like scratches or a small dent will cause a dip in value, but significant structural damage is what leads to a major drop. If the frame was bent, airbags were deployed, or major mechanical components were replaced, the vehicle is seen as inherently less safe and reliable, even after repairs. As a general rule, cars can lose 10% to 25% of their pre-accident value. For a $30,000 car, that’s a loss of $3,000 to $7,500 that you have to account for.

Your car’s specific profile plays a huge part in determining its diminished value. Newer, high-end, or luxury vehicles tend to lose a larger percentage of their value because buyers in that market expect a clean history. An accident record on a premium car is a major red flag. However, older cars aren’t immune. A well-maintained older vehicle with low mileage can also see a significant value drop. Once an accident is reported, it becomes a permanent part of the vehicle’s history report. This stigma makes it much harder to sell later, forcing you to lower the price to attract wary buyers.

Even with the best repairs, a car’s value will still be lower simply because it has an accident history. However, subpar repair work will make the situation much worse. If the body shop used low-quality aftermarket parts instead of original manufacturer equipment, or if the new paint doesn’t perfectly match the original color, these flaws will be obvious to any potential buyer or appraiser. These visible imperfections serve as a constant reminder of the accident and give buyers a powerful reason to demand a lower price. Proving this loss requires a detailed evaluation, so it’s important to get help with your claim to ensure nothing is overlooked.

Figuring out exactly how much value your car has lost isn’t a guessing game. Insurance companies won’t accept a number you pull out of thin air. To build a successful claim, you need a clear, evidence-based calculation that shows the real drop in your vehicle’s market value. This calculation is the foundation of your entire diminished value claim. While you can start the research on your own, getting an accurate number often requires a combination of professional insight and solid documentation. Let’s walk through the key steps to determine what you’re truly owed.

The most powerful tool in your corner is an independent appraisal from a certified expert. An appraiser provides an unbiased, professional opinion on your car’s pre-accident value versus its post-repair value. They consider everything from the severity of the damage to the quality of the repairs and the market demand for your specific make and model. This isn’t just an estimate; it’s a detailed report that insurance companies have a hard time disputing. Think of it as bringing in a specialist whose entire job is to assess vehicle value. Their report serves as credible, third-party evidence that strengthens your position and shows the insurer you’re serious about getting fair compensation.

Before you hire an appraiser, you can get a general idea of your car’s value loss by doing some homework. Websites like Kelley Blue Book can give you a baseline for your car’s value before the accident. From there, you can research local listings for cars similar to yours. Look for two types of vehicles: those with a clean history and those with a reported accident. The price difference between them gives you a real-world glimpse into how an accident history affects resale value. While these online tools and market comparisons are a great starting point, they usually aren’t enough to win a claim on their own. Use this research to inform yourself, but be prepared to back it up with an expert opinion.

Solid paperwork is non-negotiable. Your ability to prove your claim depends on the evidence you can provide, so it’s time to become a meticulous record-keeper. Gather every document related to the accident and your vehicle. This includes the official police report, all repair invoices and estimates, photos of the damage before and after repairs, and a copy of your vehicle’s history report. Each piece of paper tells part of the story, from the initial impact to the final repair. This collection of documents creates a clear and undeniable record for the insurance adjuster, leaving little room for them to question the facts. If you need help organizing your evidence, our team is ready to review your case and guide you through the process. You can contact us for a free consultation.

Filing a diminished value claim in Georgia involves more than just paperwork. You need to be aware of state-specific rules and deadlines that can make or break your case. Understanding these key points before you contact the insurance company will put you in a much stronger position. Here’s what you need to know to get started.

In Georgia, time is of the essence. The state has a statute of limitations that gives you two years from the date of the accident to file a lawsuit for property damage. While that might sound like a lot of time, gathering evidence, getting appraisals, and negotiating with insurers can be a lengthy process. If you wait too long, you could lose your right to pursue compensation entirely. It’s always best to start the process as soon as possible after your accident to ensure you don’t miss this critical deadline. If you’re approaching the two-year mark, it’s important to contact an attorney right away.

Determining who was at fault is a crucial step in any car accident claim. If the other driver was at fault for the accident, you are entitled to file a claim for the diminished value of your vehicle against their insurance company. This is in addition to the costs of repair. Establishing fault clearly from the beginning is essential, as it forms the foundation of your claim. Even if the situation seems straightforward, insurance companies may try to dispute liability. Having a clear police report and witness statements can make a significant difference. Our team can help you understand the details of your case and how fault impacts your claim for diminished value.

Here’s something insurance companies might not tell you: you have the right to claim diminished value. It’s a legitimate loss, but insurers often don’t volunteer this information, hoping you don’t know to ask for it. To build a strong case, you need solid proof. Start by gathering all your documents, including the police report, repair estimates and final invoices, and photos of the damage. A professional appraisal that compares your car’s value before and after the accident is also powerful evidence. The more documentation you have, the harder it is for an insurer to downplay your loss. We specialize in these types of property damage claims and can guide you through the process.

Filing a diminished value claim might seem complicated, but it really comes down to being organized and prepared. Think of it as building a case for the value your car has lost. The stronger your evidence, the better your chances of getting the compensation you deserve. It’s about proving the financial impact of the accident, even after the repairs are done. Let’s walk through the steps to get your claim started on the right foot.

Your first step is to collect everything that tells the story of your car’s value before and after the accident. A strong paper trail is your best tool. Insurance companies require solid proof, so the more detailed you are, the better.

Start by gathering these key items:

In Georgia, you will file your diminished value claim with the at-fault driver’s insurance company. This is known as a third-party claim. You are seeking compensation from the person responsible for the damage, and their insurance is obligated to cover that loss. It’s important to remember that you’re not filing against your own policy unless you live in a state with specific provisions for it, which is uncommon. The other driver’s insurer will handle the claim, so all your carefully gathered evidence will be submitted directly to them for review.

Be prepared for some pushback. Insurance adjusters are trained to minimize payouts, and their first offer will almost certainly be low. They might even try to deny the claim outright, arguing that proper repairs restored the car’s full value. A common tool they use is the “17c Formula,” a calculation that often undervalues what you’re truly owed. Don’t get discouraged. Politely reject the low offer and present your professional appraisal and evidence. If they refuse to offer a fair amount, it may be time to get expert help. An experienced attorney can handle the negotiations and fight for the full amount you deserve.

Filing a diminished value claim can feel like a maze, and insurance companies don’t always make it easy. It’s common for people to make small missteps along the way that end up costing them hundreds or even thousands of dollars. But knowing what these common pitfalls are ahead of time can help you secure the full amount you’re rightfully owed.

Think of this as your roadmap to avoiding the most frequent mistakes. From gathering the right paperwork to knowing when to push back on a low offer, a little preparation goes a long way. By steering clear of these errors, you put yourself in a much stronger position to get a fair outcome.

When you file a claim, the burden of proof is on you. You can’t just say your car lost value; you have to prove it with solid documentation. This is where many people fall short. To build a strong case, you need to collect everything related to the accident and your car’s value. This includes detailed repair records, before-and-after photos, your vehicle’s history report, and most importantly, a professional appraisal. Without this evidence, it’s your word against the insurer’s, making it difficult to prove the true diminished value of your vehicle.

After an accident, you just want things to be over. It’s tempting to accept the first offer the insurance company makes just to move on. Please don’t. Insurance adjusters are trained to settle claims for the lowest amount possible, and their initial offer is almost always a starting point for negotiation, not the final number. It rarely reflects what your claim is actually worth. Take a breath, review the offer carefully, and be prepared to negotiate. Remember, you have the right to counter an offer that you feel is unfair. Our legal representation can help you challenge these low offers.

Life gets busy, but putting your claim on the back burner is a costly mistake. In Georgia, you generally have four years from the date of the accident to file a lawsuit for property damage, which includes diminished value. While that sounds like a lot of time, waiting can seriously weaken your case. Evidence can disappear, and details become harder to recall. Acting quickly after your repairs are complete shows the insurance company you’re serious. If you’re feeling overwhelmed by the process or worried about deadlines, it’s always a good idea to contact an attorney to get things moving in the right direction.

After an accident, the last thing you want is a battle with an insurance company. Their goal is to protect their bottom line, which often means paying you as little as possible for your car’s damages and lost value. This is where we come in. At Gastley Law, we step in to manage the entire process for you, from calculating what you’re truly owed to fighting for every dollar.

You don’t have to be an expert in insurance policies or negotiation tactics. That’s our job. We handle the communication, the paperwork, and the pushback from adjusters so you can focus on getting back to your life. We believe you deserve full compensation for your property damage and your car’s diminished value, and we have the experience to make sure you get it. Working with an experienced Atlanta diminished value attorney can help strengthen your claim and pursue fair compensation from the insurance company. Think of us as your dedicated advocates, committed to turning a frustrating situation into a fair resolution.

First things first, we’ll take a close look at your situation to build a strong case. We start by calculating the permanent loss in your car’s market worth, which is its diminished value. Even if your car looks brand new after repairs, its accident history on reports like Carfax can scare away future buyers and lower its resale price. This loss is real, and you deserve to be compensated for it. We handle filing the claim with the at-fault driver’s insurance company and manage all the complicated details, ensuring everything is submitted correctly and on time.

Insurance adjusters are trained to pay as little as they can get away with. Their first offer is almost always a lowball one, and they often deny valid claims, hoping you’ll just give up. Don’t. We know their tactics and we’re prepared to counter them with solid evidence and expert negotiation. If your claim is denied, it’s not the end of the road. We can challenge the denial and aggressively fight for the fair payment you are entitled to. You don’t have to accept an unfair offer or take no for an answer.

In Georgia, a diminished value claim is typically filed against the at-fault driver’s insurance company. This means that if you were the one responsible for the accident, you generally cannot claim diminished value from your own insurance policy. The purpose of the claim is to compensate you for a loss caused by another person’s negligence.

It certainly can be. While newer cars often experience a larger drop in value, any vehicle with a good pre-accident history can suffer a financial loss. If your older car was well-maintained and had a solid market value before the crash, you likely have a valid claim. The important factor is the difference in market value before and after the accident, not just the car’s age.

Insurance companies often use a standard calculation that is designed to produce a low number that benefits their bottom line, not yours. These formulas rarely consider the unique details of your vehicle, the severity of the damage, or how the local market will react to its accident history. Accepting their initial calculation almost always means you are leaving money on the table.

While you can file a claim yourself, working with an attorney can make a huge difference. Insurance adjusters are skilled negotiators who often use tactics to underpay or deny valid claims. A lawyer manages the entire process, counters low offers with strong evidence, and signals to the insurer that you are serious about receiving fair compensation. It removes the stress from you and strengthens your position.

The timeline can vary depending on the details of your case and how cooperative the insurance company is. Some straightforward claims might be settled in a few weeks, while more complex cases that require significant negotiation could take several months. The key is to be patient and thorough. Starting the process promptly with all your documents in order can help it move more efficiently.