Insurance companies have a playbook they follow after an accident, and its main goal is to pay you as little as possible. They’ll cover the repairs, but they hope you don’t know about the other major loss you’ve suffered: the drop in your car’s resale value. This is a real financial hit, and it’s called diminished value. Adjusters are trained to downplay, deny, or make confusing arguments to avoid paying for it. This guide is your counter-playbook. We’ll expose their common tactics, explain your rights under Georgia law, and give you the tools you need to fight back and recover the full amount for your vehicle diminished value.

After a car accident, your first priority is getting your vehicle repaired and back on the road. But even after the best body shop works its magic, your car carries a history that can’t be erased. This is where the concept of diminished value comes in. Simply put, diminished value is the loss in your car’s market value because it has been in an accident. Even if it looks and drives like new, its resale value has taken a hit.

Think about it from a buyer’s perspective. If you were choosing between two identical cars, but one had a clean history and the other had been in a wreck, which would you pick? Most people would choose the one without an accident record, or at least expect a significant discount on the one that was repaired. That discount is the diminished value. It’s a real, tangible financial loss that you experience the moment you try to sell or trade in your vehicle. In Georgia, you have the right to be compensated for this loss, but insurance companies often don’t make it easy.

The main reason your car’s value drops is its newly acquired accident history. This history is often documented in vehicle history reports like CARFAX, creating a permanent record that follows the car. Potential buyers are naturally cautious about vehicles that have been in a collision. They worry about hidden structural damage, potential long-term mechanical issues, or repairs that might not hold up over time. Even with flawless repairs using original manufacturer parts, the stigma of an accident remains. This perception of increased risk directly translates into a lower market value, as buyers are unwilling to pay the same price for a previously damaged car as they would for one with a clean history.

For Georgia drivers, this loss isn’t just theoretical; it can mean thousands of dollars out of your pocket. Many people are completely unaware that they can file a claim to recover this lost value from the at-fault party’s insurance company. This is an often-overlooked part of a property damage claim that you are legally entitled to. Insurance adjusters may not volunteer this information, leaving you to absorb the financial loss when you eventually sell or trade in your car. Understanding your rights is the first step toward making sure you are fully compensated for all your losses, not just the immediate repair costs. If you’re unsure where to begin, getting a thorough case evaluation can make all the difference.

When you hear the term “diminished value,” it’s easy to think of it as a single, straightforward loss. But it’s actually a bit more nuanced. The total loss in your car’s market value after an accident is broken down into three distinct categories. Understanding which type applies to your situation is the first step in building a strong claim and knowing exactly what you’re entitled to recover from the insurance company. Each type addresses a different aspect of how an accident impacts your vehicle’s worth.

This is the most common and unavoidable type of diminished value. Inherent diminished value is the automatic drop in your car’s resale price simply because it now has an accident on its record. Think about it: if you were choosing between two identical used cars, but one had a clean history and the other had been in a wreck, which would you pay more for? Even if the repairs are flawless, the vehicle is permanently branded with an accident history, making it less attractive to future buyers. This is the core of most diminished value claims.

Immediate diminished value measures the loss in your car’s worth right after the collision, before a single repair has been made. It’s the difference between the car’s pre-accident value and its value as a damaged vehicle sitting in a tow yard. While this figure is important for insurance adjusters to assess the total loss, it’s not typically the basis for a claim unless you plan to sell the car as-is without fixing it. For most drivers who repair their vehicle, this value is temporary, and the focus shifts to the value lost after repairs are complete.

Sometimes, the body shop doesn’t get it right. Repair-related diminished value is the extra loss your car suffers due to poor-quality repairs. This can include things like mismatched paint colors, using cheaper aftermarket parts instead of original manufacturer parts, or failing to align the frame correctly. These flaws make your car worth even less than it would have been with a perfect repair. Proving this type of loss often requires a detailed inspection and expert testimony, which is where our specialized legal representation can make a significant difference in your claim’s outcome.

Figuring out your car’s diminished value isn’t as simple as plugging numbers into a calculator. Insurance companies have their own methods, which, unsurprisingly, often lead to a lower payout for you. But when you understand how the numbers work, you can push back against a lowball offer and fight for the compensation you deserve. The calculation always starts with your car’s value before the accident, but from there, the path can split. Let’s walk through the common methods you’ll encounter.

At its core, diminished value is the difference between what your vehicle was worth before the accident and what it’s worth after repairs have been completed. To calculate this loss, the first and most important step is to establish a fair, accurate pre-accident value. Insurance adjusters will often use guides like Kelley Blue Book or NADA to find this number. While these are good starting points, they don’t always reflect the true market conditions in your specific area. An accurate pre-accident valuation is the foundation of your entire claim, so getting this number right is critical to securing a fair settlement.

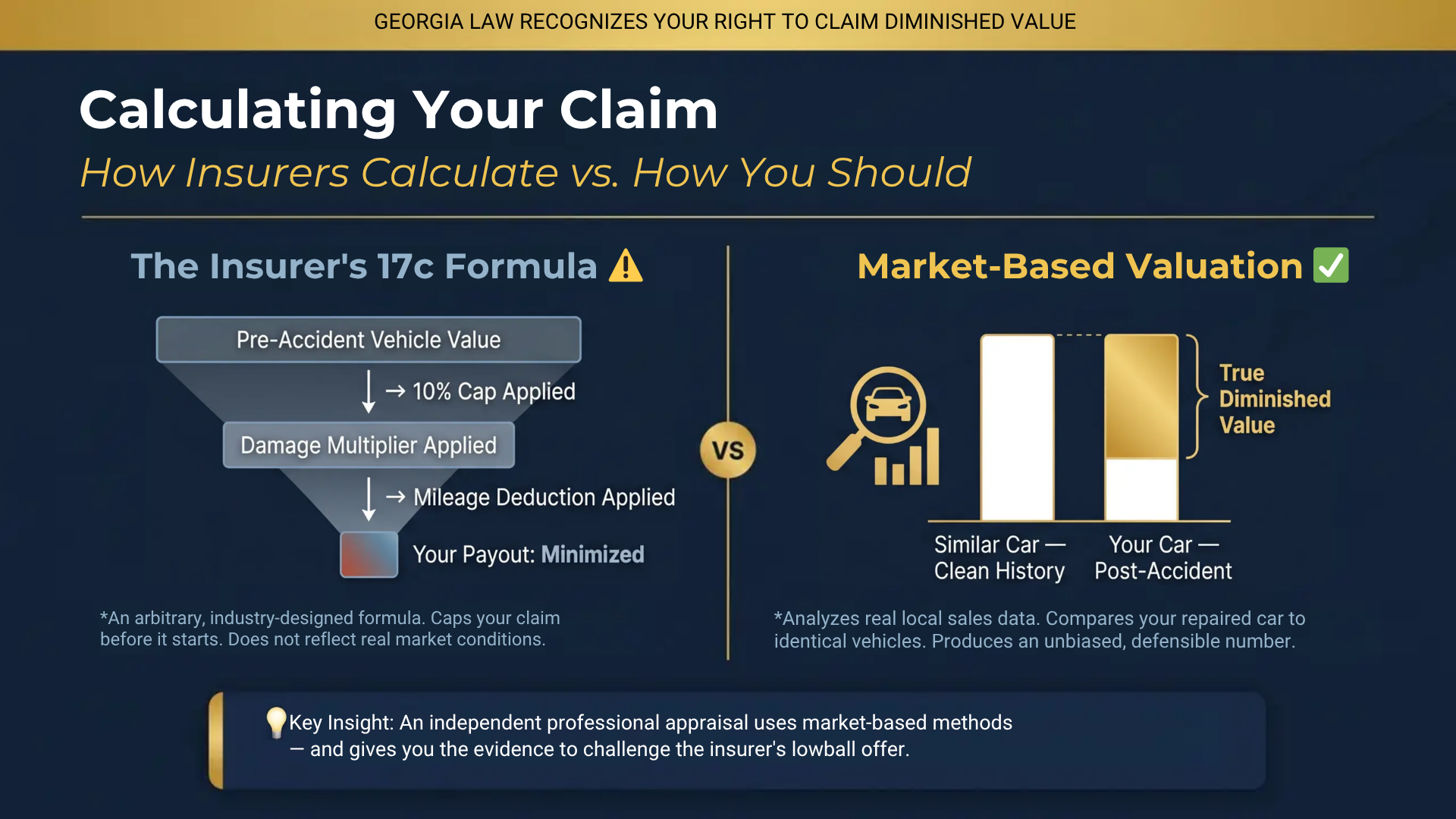

Many Georgia insurance companies use a formula called “17c” to calculate diminished value. It starts by taking your car’s pre-accident value and applying a 10% cap, which immediately limits your potential claim. From there, the adjuster applies multipliers to reduce the amount even further based on the severity of the damage and your vehicle’s mileage. This formula is controversial because it’s an arbitrary method designed to minimize what the insurance company has to pay. It doesn’t reflect the real-world market loss. Knowing that this is the insurer’s go-to playbook helps you understand why their initial offer might seem so low and why you may need to challenge their calculation.

A far more accurate way to determine diminished value is through a market-based valuation. Instead of relying on a rigid formula, this method involves analyzing real sales data from your local market. An expert appraiser will compare your repaired vehicle to similar cars that have and have not been in accidents to determine the true loss in resale value. This approach provides a transparent, data-driven assessment of your car’s diminished value. An independent appraisal based on market data gives you the concrete evidence you need to counter the insurance company’s low offer. If you’re ready to get a professional appraisal, an experienced attorney can connect you with a trusted expert.

When you file a diminished value claim, the amount you can recover isn’t a random number pulled out of a hat. It’s a calculated figure based on several key factors. Insurance companies will look at everything from the car you drive to the details of the accident to determine how much value your vehicle has lost. Understanding these elements will not only help you set realistic expectations but also empower you to build a stronger case for the compensation you deserve.

The type of car you drive is a major piece of the puzzle. Generally, newer, more valuable, and luxury vehicles experience a greater drop in value after an accident. Think about it: a potential buyer is going to be much more hesitant about purchasing a one-year-old premium SUV with an accident history than a 10-year-old commuter sedan. The amount of diminished value depends heavily on the vehicle’s pre-accident value, its age, and its mileage. A car with low mileage and a high market value simply has more value to lose.

Not all accidents are created equal, and the specifics of the collision play a huge role in your claim. A minor fender-bender that only requires cosmetic fixes will result in a much lower diminished value amount than an accident that causes structural or frame damage. The location of the damage is also critical. Damage to the frame, engine, or transmission is a major red flag for future buyers and will significantly reduce your car’s resale value. An accident history report that shows major repairs will always be a point of negotiation for a potential buyer, which is the core of your claim.

Your car’s journey doesn’t end when it leaves the repair shop. The quality of the work performed can also impact its final value. This is known as repair-related diminished value, which happens if the repairs are done poorly. Things like mismatched paint, misaligned panels, or the use of aftermarket parts instead of original equipment manufacturer (OEM) parts can make the car worth even less. This loss is a real financial hit, separate from the cost of repairs. If you suspect the repairs weren’t up to par, it’s important to have it inspected and documented.

After a car accident, one of the most common questions is, “Who is going to pay for all of this?” When it comes to diminished value, the answer isn’t always straightforward, but it generally depends on who was at fault for the collision. In most situations, you’ll be dealing with the at-fault driver’s insurance company to get compensation for your car’s lost value. However, your own insurance policy and specific state laws play a significant role in how your claim is handled.

Understanding who is responsible is the first step in recovering the money you’re owed. It helps you know where to direct your claim and what to expect from the process. For Georgia drivers, the law provides a clear path, but insurance companies can still make it a difficult journey. Knowing your rights and the roles of each insurance provider will put you in a much stronger position to get a fair settlement for your vehicle’s loss in value.

If another driver caused the accident, their insurance company is on the hook for your diminished value. This is because their policyholder is legally responsible for making you “whole” again, which includes covering the cost of repairs and compensating you for the loss in your car’s resale value. The at-fault driver’s liability coverage is what pays for these damages. Getting the insurer to agree to a fair amount is the real challenge. They will often try to minimize the payout, which is why having a solid appraisal and understanding your rights is so important. Our firm’s specialized legal representation focuses on holding these companies accountable.

What if you were at fault, or if you decide to file a claim through your own insurance for other reasons (like an uninsured at-fault driver)? In most cases, your own collision coverage will pay for your vehicle’s repairs, minus your deductible. However, standard auto policies almost always exclude coverage for diminished value. This means your own insurance company will fix your car, but they won’t pay you for the drop in its market value. This is a critical distinction to remember. You generally cannot file a first-party diminished value claim against your own insurer. The claim must be made against the person who caused the damage.

Here’s some good news for drivers in the Peach State: Georgia law is on your side. The state legally recognizes a vehicle owner’s right to claim diminished value from an at-fault driver’s insurance company. This isn’t the case in every state. Georgia’s legal framework provides a clear basis for pursuing compensation, making it one of the more favorable states for these types of claims. The law essentially confirms that you are entitled to recover the difference in your car’s value before the accident and after repairs. This legal backing is a powerful tool when an insurer tries to deny or lowball your diminished value claim.

Filing a diminished value claim might seem complicated, but it really comes down to building a strong, evidence-based case. Insurance companies are not in the business of volunteering extra money, so you need to be prepared to prove your car’s loss in value. The process involves gathering the right proof, getting an expert opinion, and presenting your claim in a way that’s hard to ignore. By following a few key steps, you can confidently state your case and show the insurer exactly what you are owed. Think of it as creating a file that tells the complete story of your car’s diminished worth, leaving no room for doubt. Let’s walk through how to put that file together.

Your claim is only as strong as the evidence you have to support it. Before you even think about contacting the insurance company, you need to collect all the necessary paperwork. Start with the final repair bill and the police accident report. Then, find your vehicle’s bill of sale and title to establish its history. The most important piece of evidence will be a professional appraisal report, which we’ll cover next. It’s also helpful to get written quotes from a few car dealerships stating they would offer less for your car now that it has an accident history. This collection of documents proves the value of your car before the crash and demonstrates the specific financial loss you’ve suffered.

This is the single most important step in the process. A professional, independent appraisal is the cornerstone of a successful diminished value claim. An experienced appraiser will conduct a thorough inspection of your vehicle, review the repair records, and compare your car to similar models on the market that have not been in an accident. They will then produce a detailed report that calculates the exact amount of value your car has lost. This isn’t just an estimate; it’s an expert assessment that provides the hard data you need to justify your claim to the insurance adjuster. Without this professional report, your claim is just your word against theirs, and that’s a tough battle to win.

Once you have your professional appraisal and all your supporting documents in hand, you’re ready to formally submit your claim. Draft a letter to the insurance company clearly stating that you are filing for the diminished value of your vehicle. Attach a copy of your appraisal report, the repair bills, the accident report, and any other evidence you’ve gathered. Send everything to the insurance adjuster handling your case. Presenting a complete, well-documented package from the start shows the insurer you are serious and have done your homework. It makes your claim much harder to dismiss and sets the stage for a more successful negotiation. If you need guidance, you can always contact us for help.

Filing a diminished value claim sounds straightforward, but insurance companies often create hurdles. Their goal is to pay out as little as possible, so you can expect some pushback. They have a playbook of common tactics designed to discourage you or convince you to accept a lowball offer.

Knowing what to expect is the first step in preparing a strong response. Insurance adjusters handle these claims every day; you might only do it once in your lifetime. This puts you at a disadvantage unless you understand their strategies and your rights. From outright denials to confusing arguments, being ready for these roadblocks will help you stand firm and pursue the full compensation you deserve. Let’s break down the common challenges and how you can handle them effectively.

Insurance companies often start by making a low offer, hoping you’ll take the quick cash and move on. Another frequent tactic is to claim your car is “good as new” after repairs. They completely ignore the fact that a vehicle with an accident history is inherently worth less to a potential buyer, no matter how great the repairs are. They might also deny the claim by saying you don’t have enough proof or that their own internal formula shows no loss in value. Don’t let these initial responses discourage you. They are standard negotiation tactics, not the final word on your claim.

Many Georgia drivers don’t realize they are entitled to compensation for their vehicle’s lost value. A diminished value claim isn’t an extra favor; it’s a legitimate part of your property damage recovery after an accident caused by someone else. You have the right to be made whole, and that includes recovering the drop in market value your car suffered. You are not required to accept the insurance company’s assessment of your loss. You have the right to present your own evidence and fight for a fair amount that reflects your car’s actual loss in value.

Successful negotiation starts with solid preparation. The single most powerful tool you have is an independent, professional appraisal. This report from a credible expert gives you a specific, evidence-based number to counter the insurer’s low offer. When you submit your claim, include your appraisal and all other documentation. Be prepared for the adjuster to push back, but stand firm on the value determined by your expert. Respond to their offers in writing and always refer back to your evidence. If the process feels overwhelming or the insurer refuses to negotiate fairly, it may be time to get in touch with us for legal support.

Getting the full compensation you deserve for your car’s diminished value requires a proactive approach. Insurance companies often try to pay as little as possible, but with the right strategy, you can build a strong case they can’t ignore. It comes down to proving your loss with solid evidence and acting within the required timeframes. By taking a few key steps, you can significantly improve your chances of a successful claim and get the money you’re rightfully owed. Let’s walk through exactly what you need to do.

The insurance company will have its own method for calculating your car’s lost value, but you shouldn’t just accept their number. The best way to determine your car’s true diminished value is to hire a professional, independent appraiser. An expert appraiser will conduct a thorough inspection and compare your vehicle to similar cars on the market, both with and without accident histories. This provides an unbiased, market-based valuation that carries much more weight than an insurer’s internal formula. Think of it as your most powerful piece of evidence for proving the full extent of your financial loss.

A strong claim is a well-documented one. To prove your case, you need to gather all the paperwork that tells the story of your car’s accident and subsequent loss in value. This includes the official police report, detailed repair invoices, and photos of the damage before and after the repairs. Most importantly, you’ll need your professional appraisal. It’s also helpful to get quotes from car dealerships showing they would offer less for your car specifically because of its accident history. Organizing these documents creates a clear and compelling file that makes it difficult for an insurer to dispute your claim. Our team can help you with these legal services.

Timing is critical when filing a diminished value claim. In Georgia, there are strict deadlines, known as statutes of limitations, for taking legal action. If you miss this window, you could lose your right to recover any compensation for your car’s lost value, no matter how strong your case is. Don’t wait too long to start the process. The clock starts ticking from the date of the accident, so it’s important to act quickly to protect your rights. If you’re feeling overwhelmed or unsure about the deadlines that apply to your situation, it’s always a good idea to contact an attorney for guidance.

Let’s be honest, dealing with an insurance company after an accident is rarely a walk in the park. While you might handle a straightforward claim on your own, there are times when calling in a professional is the smartest move you can make. Think of it this way: insurance companies have teams of experts, adjusters, and lawyers all working to protect their bottom line. Shouldn’t you have an expert on your side, too?

Hiring a diminished value attorney is about leveling the playing field. It’s for when the insurance adjuster is giving you the runaround, the offer seems insultingly low, or the details of your case are just plain complicated. An experienced attorney understands the specific laws in Georgia, knows the tactics insurers use to minimize payouts, and can build a powerful case on your behalf. For Georgia drivers facing resistance from insurers, an experienced Atlanta diminished value attorney can help pursue a fair settlement backed by strong evidence. They gather the right evidence, communicate with the insurer for you, and take the stress of negotiating off your shoulders so you can focus on getting back to your life. Many people hesitate, thinking a lawyer is only for major lawsuits, but an attorney can often secure a fair settlement much faster and for a higher amount than you could alone. If you’re feeling stuck or overwhelmed, it’s probably a good time to get a professional opinion.

Not all car accidents are simple fender benders. Sometimes, unique circumstances can make a diminished value claim much more complicated. For example, if you’re leasing your vehicle, your lease agreement likely has specific rules about accident damage that can affect your claim. High-value, classic, or exotic cars also present a challenge, as their value loss is often significant and requires specialized proof.

An attorney is essential in these situations. They can parse the fine print of a lease, bring in the right appraisers for a unique vehicle, and build a case that accounts for every complex detail. If you’re facing a situation that feels anything but standard, getting legal help ensures your claim is handled correctly from the start. Gastley Law offers specialized legal representation to manage these exact types of complex cases.

One of the most common and frustrating roadblocks you’ll face is a lowball offer or an outright denial from the insurance company. Many drivers don’t even know what diminished value is, and insurers often count on that. They might tell you that diminished value isn’t covered, use a flawed formula to come up with a tiny number, or simply deny the claim hoping you’ll give up.

A denial is not the end of the road. An attorney knows that these are just negotiation tactics. They can effectively counter the insurance company’s arguments with a solid, evidence-based claim backed by a professional appraisal. If the insurer still refuses to pay what you’re rightfully owed, your attorney can take legal action to recover the full amount. You don’t have to accept an unfair outcome.

Not at all. The financial loss happens the moment the accident becomes part of your vehicle’s history, not when you decide to sell it. You have the right to be compensated for that drop in market value right now, even if you plan on driving the car for several more years. The claim is about restoring the value of your asset.

Typically, you cannot file a diminished value claim against your own insurance policy. These claims are made against the at-fault driver’s liability coverage. Your own collision policy is designed to cover the cost of repairs to get your car back on the road, but it almost always excludes coverage for the loss in market value.

In Georgia, the statute of limitations for property damage claims is generally four years from the date of the accident. While that sounds like a lot of time, it is always best to start the process as soon as your vehicle repairs are finished. Acting quickly ensures that evidence is fresh and makes it easier to build a strong case.

There is no standard amount, because every vehicle and accident is different. The final compensation depends heavily on your car’s age, make, model, and pre-accident condition, along with the severity of the damage it sustained. A professional appraisal is the most accurate way to determine the specific financial loss for your car.

Yes, you can still file a claim. The calculation will focus on the additional loss in value caused by this most recent accident. An appraiser will first establish your car’s value with its existing accident history and then determine how much more its value dropped due to the new damage. It makes the case more complex, but you are still entitled to compensation for the new loss.