How to Win Your Allstate Diminished Value Claim

If you’re a driver in Georgia dealing with Allstate after a crash, your diminished value claim is about more than getting the car repaired. It is about proving the vehicle lost market value because the accident is now part of its history. Allstate may review the claim, assign an adjuster, and make an initial offer, but that offer may not reflect the full real-world loss. This guide explains how Georgia drivers can document an Allstate diminished value claim, evaluate a low offer, understand the limits of the 17c formula, and decide when to get help from Gastley Law.

Key Takeaways

- Georgia drivers may have a path to diminished value recovery: Depending on fault, coverage, and claim facts, a Georgia driver may have first-party or third-party options for an Allstate diminished value claim.

- Documentation drives the claim: Repair invoices, supplement history, photos, the accident report, mileage, trim, pre-loss value support, and Allstate’s written offer or denial can all affect how strong your demand package is.

- Allstate’s first offer is not always the full value: If the offer relies on a formula or internal calculation, compare it against market evidence and an independent appraisal before accepting it.

- An independent appraisal can support negotiations: A market-based appraisal can help counter a low calculation and give you a clearer number for negotiations.

- Legal help may make sense when negotiations stall: If Allstate delays, denies the claim, or refuses to explain a low offer, contact Gastley Law to discuss next steps.

What Is a Diminished Value Claim with Allstate?

In Georgia, an Allstate diminished value claim is a request for payment for the loss in market value your vehicle suffers after a crash, even after repairs. The strength of the claim usually depends on repair records, pre-accident value, accident history, mileage, damage severity, and whether the offer reflects the vehicle’s real post-repair market value.

If you’re dealing with Allstate after an accident, you’ve probably heard the term “diminished value.” It sounds complicated, but the concept is pretty straightforward. Filing a claim is your right, but getting a fair payment requires understanding how Allstate operates. They have a specific process, and knowing what to expect can make a huge difference in the amount of money you recover. Let’s break down what a

First, What Is Diminished Value?

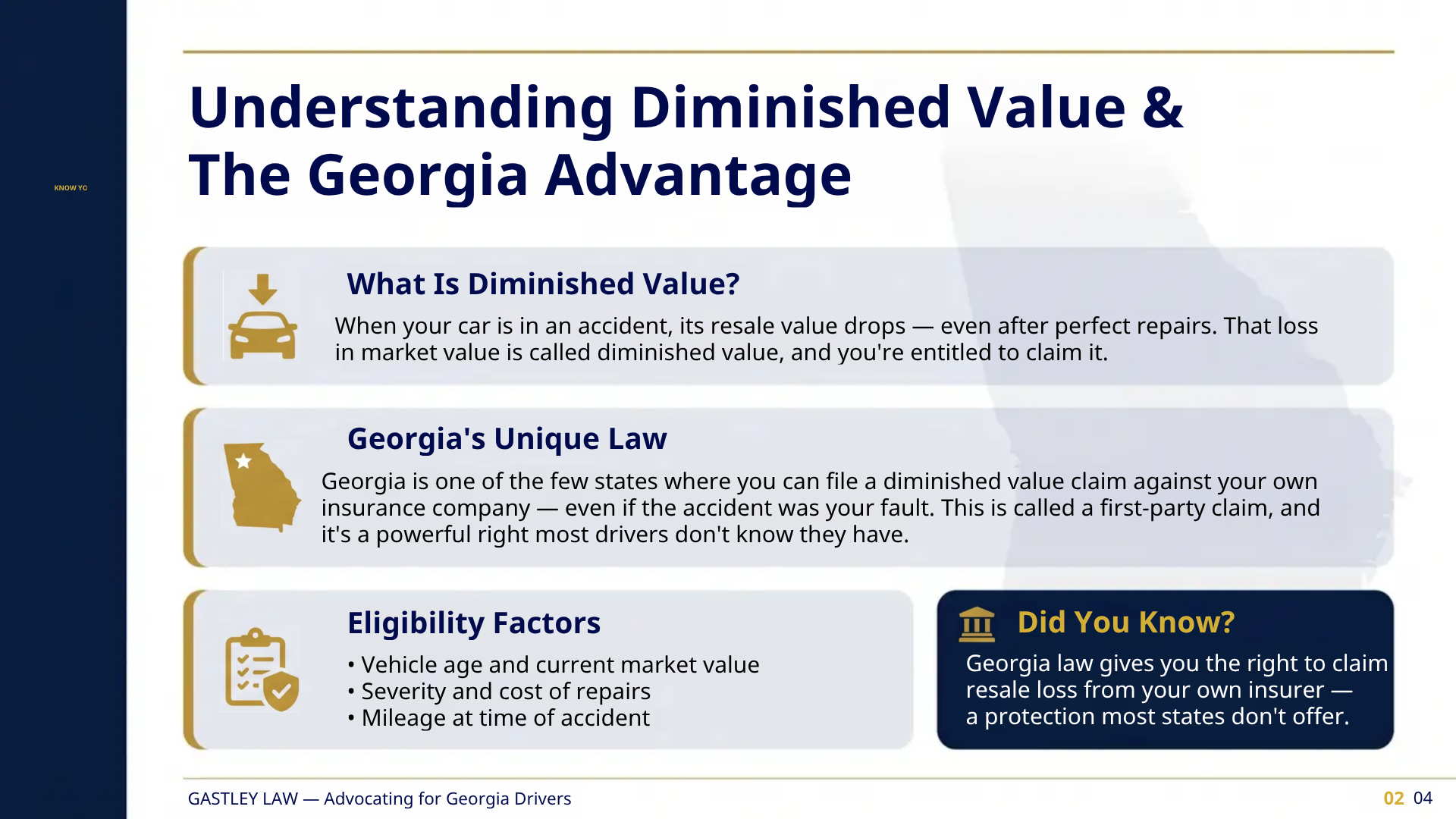

Think of it this way: even after your car has been perfectly repaired, it’s worth less than it was before the accident. Why? Because the collision is now part of its permanent record on vehicle history reports like CARFAX. When you decide to sell or trade it in, potential buyers will see that accident history and won’t be willing to pay top dollar. The difference between your car’s pre-accident value and its post-repair value is its diminished value. It’s a real, tangible loss, and you deserve to be compensated for it.

How Allstate Typically Handles These Claims

The good news is that Allstate generally pays diminished value claims in Georgia. The challenge, however, is that the amount they offer can vary wildly. It’s up to you, the vehicle owner, to prove how much value your car has actually lost. Allstate won’t just hand over a check for the full amount without some pushback. Their first offer is almost always just a starting point for negotiations, not their final answer. They expect you to provide evidence that justifies a higher payout, so being prepared is key to getting what you’re owed.

Decoding the 17c Formula and Initial Offers

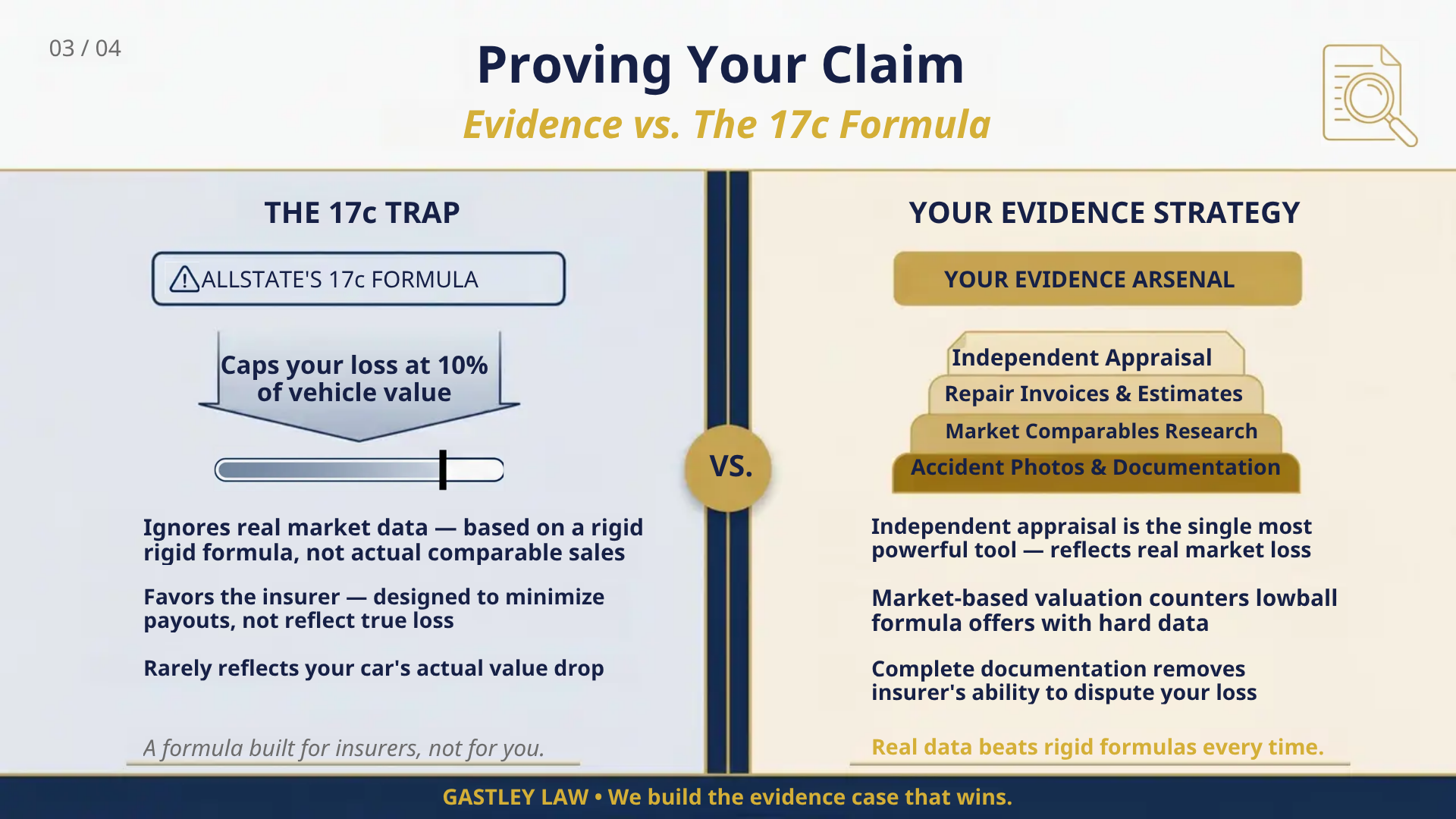

So, how does Allstate come up with that initial low offer? They often use a standard calculation known as the “17c formula.” This formula was created by insurance companies and, not surprisingly, it tends to favor them. It starts by capping the maximum potential loss at 10% of the car’s pre-accident value and then applies other modifiers that can unfairly reduce the final number. Because this method doesn’t reflect what real buyers in the market would pay, it almost always results in a lowball offer. Understanding this helps you see why their first number isn’t the real value and why you need expert help to fight for fair compensation.

Can You File a Diminished Value Claim with Allstate?

Yes, you absolutely can file a diminished value claim with Allstate, but it’s not an automatic process. Before you even start gathering paperwork, you need to make sure your situation meets a few key requirements. Think of it as a preliminary checklist. Allstate will look at who was at fault in the accident, the condition of your vehicle before the crash, and whether you’re filing within the legal time frame.

It’s important to remember that insurance companies are businesses, and they often look for reasons to minimize payouts. By confirming your eligibility on these key points, you’re not just checking boxes; you’re building the foundation for a strong case. Understanding these factors upfront will save you a lot of time and frustration and shows the insurance adjuster that you know what you’re doing. Let’s walk through exactly what you need to confirm to see if you have a valid claim for your vehicle’s diminished value. This initial step is crucial because it sets the tone for your entire claim and helps you anticipate the questions and potential pushback you might receive from the adjuster. Getting your facts straight from the start is the best way to prepare for a successful negotiation.

Check Your Eligibility and Fault Requirements

The first thing to figure out is who caused the accident. In most states, you can only file a diminished value claim against the at-fault driver’s insurance policy, which is known as a third-party claim. If you were the one at fault, you typically can’t file a claim with your own insurer.

However, Georgia has a unique rule that works in your favor. Here, you are legally entitled to claim diminished value from your own insurance company, even if you were at fault, as long as you have collision coverage. This is called a first-party claim, and it’s a critical distinction that many Georgia drivers don’t know about. So, whether the other driver was responsible or you were, you likely have a path to file a claim with Allstate.

Does Your Vehicle’s Age, Mileage, and Damage Qualify?

Not every car or every accident will qualify for a diminished value claim. Allstate will assess whether the damage was significant enough to actually lower your car’s resale value. Minor cosmetic issues like small scratches or a tiny dent that’s easily fixed probably won’t be enough. The damage needs to be substantial enough to show up on a vehicle history report like CarFax.

Your vehicle’s age and mileage also play a big role. Newer cars with fewer miles stand to lose the most value after an accident, making them strong candidates for a claim. An older vehicle with high mileage has already depreciated quite a bit, so the loss in value after a wreck will be much smaller, and Allstate may argue it’s negligible.

Know Your Deadline for Filing a Claim

Every state has a law called the statute of limitations, which sets a strict deadline for filing legal claims. If you miss this window, you lose your right to pursue compensation, no matter how strong your case is. You can’t afford to wait.

In Georgia, you have four years from the date of the accident to file a property damage claim, which includes diminished value. While four years might sound like a long time, it’s always best to act quickly. Evidence can be lost, and details can become fuzzy over time. Starting the process sooner rather than later ensures you have everything you need and puts you in a better position to negotiate. If you’re approaching the deadline, it’s a good idea to contact us right away.

What Paperwork Do You Need to File Your Claim?

Before you send a demand or respond to an Allstate offer, organize the records that prove the accident, repairs, and market-value loss. A stronger claim package usually includes:

- Final repair invoice

- Repair estimate and supplement history

- Accident report

- Photos of vehicle damage and completed repairs

- Vehicle history report

- Mileage, trim, options, and pre-loss value support

- Allstate claim number and written offer or denial

- Independent diminished value appraisal, if available

When you file a diminished value claim, you’re essentially telling the insurance company, “My car is worth less now because of this accident, and you need to compensate me for that loss.” To make them listen, you need to back up your words with solid proof. Think of yourself as building a case; the stronger your evidence, the harder it is for an adjuster to argue with you. Getting your documents in order from the very beginning is the best way to set yourself up for a successful claim. It shows you’re serious and prepared. Understanding what diminished value is is the first step, but proving it requires the right paperwork. Let’s walk through exactly what you need to collect to build an undeniable claim.

Gather Your Repair Records and Invoices

After an accident, the repair shop will generate a lot of paperwork. Keep every single piece of it. The most important document is the final, itemized repair invoice. This list details every part that was replaced and every hour of labor that went into fixing your car. It’s concrete proof of the accident’s severity. A long, detailed invoice shows the insurance company that the damage wasn’t just a minor scratch; it was significant enough to require extensive work. This documentation is the foundation of your claim, as it directly connects the accident to the physical repairs that now mar your vehicle’s history.

Prove Your Vehicle’s Pre-Accident Value

To show your car has lost value, you first have to establish what it was worth right before the crash. While online tools like Kelley Blue Book are a decent starting point, they aren’t enough to convince an adjuster. You need to do a little market research. Look for cars for sale in your area that are the same make, model, year, and trim as yours, with similar mileage and condition. Save screenshots of these listings. This real-world evidence shows the adjuster the actual market value of a comparable vehicle without an accident history, creating a clear baseline for your claim.

Collect the Accident Report and Photos

The official police report is a critical piece of evidence. It’s an objective, third-party account of the accident that typically states who was at fault. Make sure you get a copy as soon as it’s available. In addition, photos are incredibly powerful. You’ll want pictures of the damage to your car right after the accident, before any repairs have been made. These images show the true extent of the impact. It’s also helpful to have photos of the car after it has been repaired. While it might look good as new, these photos are part of the story that proves significant work was done.

Get a Professional Appraisal and Vehicle History Report

This is arguably the most important step you can take. A professional diminished value appraisal from an independent expert gives you a detailed report that calculates your car’s exact loss in value. This isn’t just your opinion; it’s a fact-based assessment from a specialist, which is very difficult for an insurance company to ignore. You should also get a vehicle history report, like a CarFax, to show that your car had a clean record before the accident. This proves the value loss is a direct result of this specific incident. Having an expert appraisal is your strongest tool, and our team can help you get one. If you need guidance, please contact us.

How Is Diminished Value Calculated?

Understanding how your car’s lost value is calculated is the key to getting a fair settlement. Insurance companies have their preferred methods, which often work in their favor, not yours. But you don’t have to accept their number at face value. The best approach involves using real-world data and expert analysis to prove what your car is truly worth now that it has an accident history. Let’s break down the common formula insurers use and the more accurate methods you should rely on.

Allstate Diminished Value Calculator: What It Can and Cannot Tell You

An Allstate diminished value calculator, or any online diminished value calculator, can give you a rough starting point. It may ask for the vehicle’s pre-accident value, mileage, age, and damage severity. The problem is that a calculator cannot fully measure Georgia market conditions, buyer hesitation after an accident history appears, repair quality, specialty trim, prior damage, or the details of Allstate’s written offer.

Use a calculator as a screening tool, not a final settlement number. If Allstate’s offer is based on a formula and seems low, compare it with the Georgia 17c diminished value formula, local market evidence, and an independent appraisal before deciding whether to accept.

The 17c Formula: What Is It?

Many insurance companies, including Allstate, use a calculation known as the “17c formula” to determine your car’s diminished value. While it sounds official, this formula is notorious for producing lowball offers. It starts by capping the maximum value your car can lose at 10% of its pre-accident value, which is an arbitrary limit. Then, it applies modifiers that reduce the payout even further based on the severity of the damage and your car’s mileage. This method often fails to reflect how real buyers in the market will view your vehicle’s accident history, leaving you with less than you deserve.

A Better Way: Market-Based Valuation

A much fairer way to calculate diminished value is to look at the actual market. Think like a potential buyer: how much less would you pay for a car that’s been in an accident compared to an identical one with a clean history? You can start by finding your car’s pre-accident value using resources like Kelley Blue Book. Then, take it a step further by researching local listings for vehicles of the same make, model, year, and condition. This real-world evidence provides a solid, market-based argument for your car’s loss in value that is much more compelling than an insurer’s internal formula.

Why a Professional Appraisal Is Your Best Bet

While market research is a great start, the single most powerful tool in your corner is a professional appraisal from an independent expert. This isn’t a quick estimate from an online calculator; it’s a detailed, certified report that provides a factual, unbiased assessment of your vehicle’s diminished value. An independent appraisal carries significant weight in negotiations because it’s hard for an adjuster to dispute. It serves as concrete proof of your financial loss and is often the key to overcoming a low initial offer. If you’re serious about getting fully compensated, we can help you take this crucial step.

How to File Your Diminished Value Claim with Allstate

Filing a diminished value claim can feel like a complicated puzzle, but it’s manageable when you break it down into clear steps. Think of this as your roadmap to getting the compensation you deserve. The key is to be organized, persistent, and prepared. Allstate handles these claims every day, so showing up with a well-documented case is the best way to get their attention and prove you’re serious. Let’s walk through exactly what you need to do.

Step 1: Notify Allstate and Open Your Claim

Your first move is to get in touch with the Allstate adjuster assigned to your case. You need to tell them, in no uncertain terms, that you intend to file a diminished value claim. Don’t wait for them to bring it up, because they won’t. This call officially puts your request on the record and starts the process. Be polite but firm in your intention. You can simply say, “I’m calling to formally open a diminished value claim for my vehicle.” They will likely ask for documentation to support your claim, which leads us to the next step.

Step 2: Submit All Your Documentation

This is where you build the foundation of your claim. Your goal is to provide undeniable proof that your car lost value because of the accident. Gather every piece of paper related to the incident and repairs, including the official police report, itemized repair invoices, and photos of the damage before and after the repairs. The single most important document you will submit is a professional, independent appraisal report. This report, prepared by an unbiased expert, is your strongest piece of evidence. It provides a credible, market-based assessment of your car’s lost value, making it much harder for the insurer to dispute. You can learn more about what diminished value is and why this proof is so critical.

Step 3: Communicate with the Adjuster (and Know the Timeline)

Once you submit your documents, the negotiation begins. Be prepared for the adjuster to come back with a low offer; it’s part of their job. Your job is to stand your ground. Respond to their offer by referring back to the facts and the total in your independent appraisal report. Keep your communication professional and focused. It’s also important to know your deadline. In Georgia, you generally have four years from the date of the accident to file a claim for property damage. While that sounds like a lot of time, it’s best to act quickly. If the back-and-forth becomes overwhelming, exploring your legal representation options can help you finish strong.

How Do You Negotiate an Allstate Diminished Value Offer?

Once you’ve filed your claim, the negotiation process begins. Ask Allstate to explain the calculation in writing, compare the offer against appraisal and market evidence, submit a concise demand package, track every deadline, and escalate when the numbers do not reflect the vehicle’s real post-repair value. If an insurance settlement offer is too low, preparation and documentation matter.

Start with a Professional Appraisal

Think of a professional appraisal as your most powerful tool in this negotiation. An independent appraisal provides a detailed, factual report on your car’s lost value, making it incredibly difficult for Allstate to justify a lowball offer. This isn’t just your opinion against theirs; it’s an expert valuation based on market data. This report will serve as the foundation for your entire negotiation, giving you a specific, defensible number to work toward. Before you even speak with an adjuster about a settlement, having this document in hand shows you are serious about receiving a fair diminished value payment.

Counter Their First (Low) Offer

Allstate will likely present an initial offer calculated using an internal method known as the “17c formula.” This formula is notorious for producing low figures because it doesn’t accurately reflect how real buyers perceive a car with an accident history. When you receive this offer, don’t get discouraged. Expect it, and be ready to counter. Your response should be simple: present your independent appraisal report. This shifts the focus from their internal formula to a real-world assessment of your vehicle’s loss in value. Politely state that their offer is unacceptable and that your counteroffer is based on your professional appraisal.

Use Facts and Persistence to Your Advantage

Insurance adjusters are trained to keep payouts as low as possible. Your job is to remain calm, stick to the facts, and be persistent. Refer back to your appraisal report during every conversation. If the adjuster dismisses your evidence, ask them to provide a detailed, written explanation for their valuation. If you hit a wall and the adjuster refuses to offer a fair amount, you have options. You can ask to speak with a manager or file a complaint with the Georgia Department of Insurance. If negotiations stall completely, it may be time to seek legal representation to handle the communication and fight for the full amount you are owed.

When Should You Contact a Georgia Diminished Value Lawyer?

You should consider contacting a Georgia diminished value lawyer when Allstate’s offer seems low, the adjuster will not explain the calculation, the claim is denied, the claim keeps getting delayed, or you are unsure whether fault or coverage affects your options. A lawyer can help review the policy issues, organize the evidence, communicate a demand, and evaluate whether negotiation, an appraisal-clause dispute, or litigation makes sense.

Gastley Law focuses on Georgia diminished value and property damage claims. If you are dealing with an Allstate low offer or denial, contact Gastley Law to discuss the next step for your claim.

Why Might Allstate Deny Your Claim?

Receiving a denial letter from Allstate can feel like a major setback, but it’s often just the start of the negotiation process. Insurance companies are businesses, and their goal is to pay out as little as possible. A denial isn’t always the final word; sometimes, it’s a strategy to see if you’ll simply give up. Understanding the common reasons they deny diminished value claims is the first step to building a stronger case and fighting back for the compensation you deserve. From a vehicle’s prior history to missing paperwork, their reasons can seem valid on the surface, but they don’t always hold up under scrutiny.

Red Flag: A Previous Accident History

One of the first things an adjuster will look for is your vehicle’s history. If your car has been in a previous accident, Allstate may argue that its value was already diminished and deny your new claim. Their logic is that the prior damage is the true source of the car’s lost value, not the most recent accident. For example, they might point to a significant repair from years ago and claim that any current loss in market value is tied to that old event. However, this argument overlooks the fact that a new, separate accident causes a fresh instance of diminished value, adding another negative event to your vehicle’s history report.

The Problem with Insufficient Documentation

A diminished value claim is only as strong as the evidence you provide. If your submission is missing key documents, Allstate has an easy reason to issue a denial. The burden of proof is on you to show that your vehicle lost value because of the accident. To do this, you need a complete file with an official police report, detailed repair invoices, clear photos of the damage before and after repairs, and a comprehensive vehicle history report. Without this paper trail, the adjuster can simply state that you haven’t provided enough proof to support your claim, stopping you in your tracks before you even get to negotiate.

Understanding Policy Exclusions and Limitations

Insurance policies are filled with specific terms and conditions, and it’s easy to miss an important detail. One of the most common reasons for a diminished value denial is related to who was at fault. In Georgia, you can only file a diminished value claim against the at-fault driver’s insurance company (a third-party claim). If the accident was your fault, your own policy (a first-party claim) typically will not cover the loss in your vehicle’s value. It’s crucial to read your policy carefully or get expert help to understand these limitations before you file. If you’re unsure about your policy’s language, our team can help you understand your options for legal representation.

What to Do If Allstate Denies Your Claim

Receiving a denial letter from Allstate can feel like hitting a brick wall, but it’s not the end of the road. Insurance companies often deny claims or make lowball offers hoping you’ll simply give up. Don’t. You have several options for pushing back and fighting for the compensation you deserve. By taking a few strategic steps, you can challenge their decision and show them you’re serious about your claim. Think of their initial “no” as the start of a negotiation, not the final word. Here’s what you can do next.

Ask to Speak with a Supervisor

Your first move should be to escalate the issue within Allstate. The claims adjuster you’ve been dealing with has limited authority, but their manager often has more flexibility to approve a higher settlement. When you call, calmly state that you are not satisfied with the decision and would like to speak with a supervisor to review your claim. This simple step can sometimes resolve the issue without any further hassle. A manager can re-evaluate the evidence you’ve provided and may overturn the initial denial or increase the offer to avoid a more formal dispute.

File a Complaint with the Department of Insurance

If speaking with a supervisor doesn’t work, your next step is to get an outside authority involved. Every state has a department that regulates insurance companies, and in Georgia, you can file a complaint with the Office of Commissioner of Insurance and Safety Fire. This action gets your case in front of regulators who will investigate whether Allstate handled your claim fairly. The insurer is required to respond to the department, which often prompts them to take a second, more serious look at your case and present a better offer to avoid regulatory scrutiny.

Consider the Appraisal Clause or Legal Action

If you’re still at a standstill, check the at-fault driver’s policy for an “appraisal clause.” This provision allows both you and Allstate to hire independent appraisers. If they can’t agree on the diminished value amount, a neutral third-party umpire makes the final call. This can be a powerful tool for getting a fair valuation. If the policy doesn’t have this clause or if Allstate refuses to cooperate, it may be time to consider legal action. At this stage, having an experienced attorney who specializes in property damage claims can make all the difference in getting the full amount you’re owed.

Related Articles

- State Farm diminished value claim

- GEICO diminished value claim

- Progressive diminished value claim

- AAA diminished value claim

- Georgia 17c diminished value formula

- What to do when an insurance settlement offer is too low

FAQs About Allstate Diminished Value Claims

Will Allstate pay diminished value in Georgia?

Allstate may pay diminished value in Georgia when the facts, coverage, documentation, and valuation support the claim. Payment is not automatic. You still need evidence showing that the vehicle lost market value after the accident and repairs.

Does Allstate use the 17c formula?

Allstate may use an internal calculation or formula-based approach when evaluating diminished value. If the number seems low, compare it against market evidence, the Georgia 17c diminished value formula, and an independent appraisal.

What if Allstate’s diminished value offer is too low?

Ask for the calculation in writing, review the assumptions, gather repair and market evidence, and submit a concise counter-demand. If negotiations stall, legal help may be appropriate.

Do I need an appraisal for an Allstate diminished value claim?

An appraisal is not always required, but it can be one of the strongest pieces of evidence when Allstate disputes the amount of value loss or makes a low offer.

Can I file if I was partly or fully at fault?

Georgia drivers may have first-party or third-party paths depending on the facts of the accident and the policy language. Do not assume you have no claim just because fault is disputed. Review the coverage and get advice if the answer is unclear.