So, the insurance company declared your car a total loss, and their offer is nowhere near what you need to buy a replacement. What do you do now? While it’s easy to feel overwhelmed, you have more power in this situation than you think. The single most important step you can take is to get your own independent total loss appraisal. This process provides you with a detailed, evidence-based report from an unbiased expert that proves your car’s true pre-accident value. This report becomes your most powerful piece of evidence, giving you the leverage you need to effectively negotiate with the insurance adjuster. It’s the key to challenging a lowball offer and securing the fair settlement you deserve.

When an insurance company declares your car a total loss, their next step is to offer you a settlement. But how do you know if their offer is fair? That’s where a total loss appraisal comes in. Think of it as a professional second opinion on your car’s value, conducted by an unbiased expert. An independent appraiser evaluates your vehicle’s pre-accident condition, features, and mileage to determine what it was truly worth right before the crash. This process is your most powerful tool for challenging a lowball offer from an insurer.

Without an independent appraisal, you’re essentially taking the insurance adjuster’s word for what your car was worth. Their valuation reports can be based on outdated data or comps that don’t accurately reflect your vehicle’s condition or the local market. An appraisal provides a detailed, evidence-based report you can use to negotiate a better payout. It shifts the power back into your hands by arming you with credible proof of your car’s value. This ensures the settlement reflects your car’s actual market value, not just the amount that’s most convenient for the insurance company. It’s about making sure you get the money you need to actually replace your vehicle and move forward.

The appraisal process is pretty straightforward. You hire an independent, certified appraiser who specializes in vehicle valuation. They will conduct a thorough inspection of your car, considering everything from its mileage and maintenance history to any custom upgrades you’ve made. They also research the current market, looking at what similar vehicles are selling for in your area. The result is a comprehensive report that outlines your car’s pre-accident value. Many insurance policies include an “Appraisal Clause,” which gives you the right to get your own appraisal if you dispute the insurer’s offer. While it typically costs around $500, this investment can lead to a significantly higher settlement. Gastley Law can guide you through all of our legal services to ensure you get what you’re owed.

An insurance company will declare a car a “total loss” when the cost to repair it is more than the vehicle is worth. Each state has a specific threshold for this, but it’s generally when repair costs reach a certain percentage of the car’s value. A car can also be totaled if the damage is so severe that it can’t be safely repaired, regardless of the cost. Another scenario is theft. If your car is stolen and not recovered within a certain period (usually 30 days), the insurer will typically declare it a total loss and pay out the claim. Understanding what diminished value is can also be helpful, as it relates to a car’s loss in value after an accident, even if it isn’t totaled.

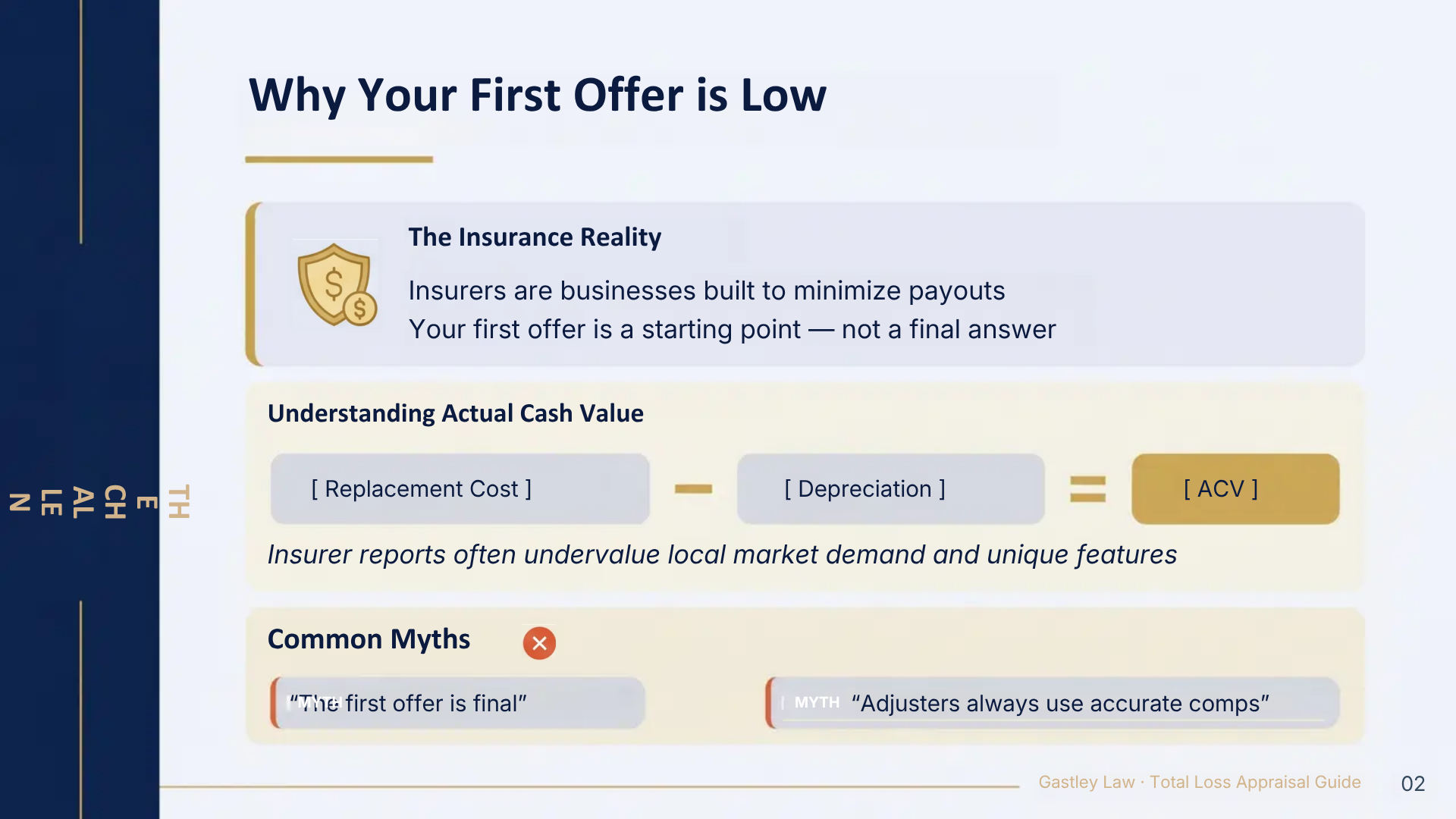

When you get a settlement offer, it’s almost always based on your car’s Actual Cash Value (ACV). ACV is the amount it would cost to replace your vehicle with a similar one, minus depreciation. Depreciation accounts for wear and tear, age, and mileage. So, the ACV is what your exact car was worth the moment before the accident, not what a brand-new one would cost. Replacement Cost, on the other hand, is the price of a new, comparable vehicle without any deduction for depreciation. This type of coverage is less common and usually costs more. Because most policies use ACV, the initial offer from an insurer can feel surprisingly low. If you believe the ACV offer is unfair, it’s time to get an independent appraisal and contact us for help.

When your insurance company declares your car a total loss, their first settlement offer can feel like a final decision. But it’s really just the start of a conversation, and you don’t have to accept a number that feels too low. An independent total loss appraisal is your most powerful tool for turning that conversation in your favor. Think of it as a second opinion from an unbiased expert who works for you, not the insurance company.

Getting your own appraisal shifts the dynamic. Instead of just questioning the insurer’s valuation, you’re presenting them with a detailed, evidence-based report that reflects your vehicle’s true market value. This simple step is often the key to ensuring you have the funds you actually need to replace your car and get back on the road. It’s about making sure you’re treated fairly and receive the full compensation you’re entitled to after an accident.

Insurance companies are businesses, and their goal is often to pay out as little as possible on claims. They typically use valuation reports from third-party companies that may not accurately capture your car’s unique condition, features, or local market value. This can lead to a settlement offer that falls short of what you need to buy a comparable vehicle. An independent appraiser provides an objective valuation based on a thorough inspection and real-world data. This report serves as your defense against an unfair offer and helps establish a more accurate baseline for what your property damage claim is truly worth.

Walking into a negotiation without evidence is like showing up to a test without studying. You can’t just tell the insurance adjuster you think their offer is unfair; you have to show them why. A total loss appraisal is your proof. It’s a professional document that outlines your vehicle’s specific condition, features, and recent upgrades, culminating in a clear, defensible value. Handing this report to the adjuster gives you immediate leverage. It forces them to address specific, factual points rather than relying on their own standardized, and often flawed, valuation methods. This puts you in a much stronger position to negotiate a better settlement.

Ultimately, the goal is to get a payout that makes you whole again. A professional appraisal is the most effective way to make that happen. It provides the documentation needed to justify a higher settlement, ensuring you have the money to purchase a similar car. Without it, you might be left covering the difference out of your own pocket. If you’re feeling overwhelmed or the insurance company is refusing to budge, it might be time to get some help. An experienced attorney can use your appraisal to advocate on your behalf and fight for the fair compensation you rightfully deserve.

When an insurance company declares your car a total loss, they are supposed to pay you its Actual Cash Value (ACV). In simple terms, that’s what your car was worth the moment before the accident. But how they arrive at that number is often where the problems start. It can feel like they just pulled a number out of thin air, especially when it’s far less than what you know it will cost to buy a similar car. Insurers typically use valuation reports from third-party companies like CCC and Mitchell, and these reports can be inaccurate, undervaluing your vehicle and leaving you with a lowball offer. The entire dispute comes down to one thing: their valuation doesn’t match what your car was really worth. Knowing exactly what factors determine your car’s value is the first step in protecting yourself. It gives you the knowledge to identify an unfair offer and the confidence to push back for the compensation you rightfully deserve. From its specific features to the local market, several pieces come together to build its true value.

First, the basics: the insurance adjuster will look at your car’s year, make, model, and trim package. A higher-end trim level is worth more than a base model. But the pre-accident condition of your car is just as important. Was it in pristine shape with a spotless interior and a well-maintained engine? Or did it have existing dings, scratches, and high wear and tear? Be honest about the condition, but don’t let an adjuster undervalue a well-cared-for vehicle. Your maintenance records can be powerful proof here, showing that you invested in keeping the car in great shape, which adds to its overall value.

This is where most disagreements happen. The insurer’s valuation is supposed to reflect the current market value, meaning what a willing buyer would have paid for your car right before the crash. To figure this out, adjusters use valuation reports that pull data on “comps,” or comparable vehicles recently sold in your area. The problem is, the comps they choose might not be a true match. They might use vehicles with fewer features, a less desirable color, or from a dealership far away. This is a common tactic that leads to a lower diminished value and a settlement that doesn’t cover your loss.

Two of the biggest factors in any car’s value are its mileage and location. It’s simple: a car with 50,000 miles is worth more than the exact same model with 150,000 miles. Lower mileage suggests less wear and a longer remaining lifespan. Location matters because car values fluctuate based on regional demand. A 4×4 truck might be more valuable in a mountainous or snowy area, while a convertible might fetch a higher price in a sunny state. The insurance company should be using comps from your specific local market, not from a hundred miles away where prices might be lower.

Did you invest in custom wheels, a premium sound system, or a new suspension? These aftermarket upgrades can add significant value to your vehicle, but insurers often overlook them. It’s crucial to provide receipts and documentation for any modifications you’ve made. While a standard policy may have limits on coverage for custom parts, they should still be factored into the overall valuation. If your car had thousands of dollars in upgrades, it was objectively worth more than a stock model. This is another area where having a professional advocate can help ensure you get credit for the money you invested in your car.

After an accident, the insurance company will have its own appraiser determine your car’s value, but their goal is often to pay out as little as possible. Hiring your own independent appraiser is your best move for getting a fair, unbiased valuation. Think of them as an expert in your corner, dedicated to assessing the true value of your vehicle without any pressure from the insurer. Their only loyalty is to the facts and the market data, not to an insurance company’s bottom line.

But a quick search will show you there are a lot of appraisers out there, and they aren’t all created equal. Finding the right one is key to building a strong case for the compensation you deserve. A detailed, professional report from a credible appraiser is a powerful tool that can completely change the course of your negotiations. It’s not just about getting a second opinion; it’s about getting an expert valuation that the insurance company can’t easily dismiss. Here’s what you should look for to make sure you’re hiring a true professional who can help your claim.

First things first, check for credentials. A certified appraiser isn’t just someone who knows a lot about cars; they’re a professional who has been trained and tested to meet specific industry standards. This certification shows that they follow a strict code of ethics and use accepted methods to determine a vehicle’s value. An insurer is far more likely to take an appraisal seriously when it comes from a certified professional. This simple check can make a huge difference in whether your report is seen as a valid piece of evidence or just another opinion. It’s a crucial part of understanding your car’s diminished value and total loss worth.

Experience is about more than just years in the business. You need an appraiser who has specific experience handling total loss and diminished value claims for consumer vehicles. Someone who primarily appraises exotic cars for auctions might not understand the nuances of negotiating with an insurance adjuster. Look for a licensed appraiser with a proven track record of creating professional reports based on real market data. They should know exactly what adjusters look for and how to present information in a way that is clear, compelling, and difficult to dispute. This kind of specialized experience is what provides you with an accurate valuation and strengthens your position.

Before you commit, do a little digging. What are past clients saying about them? Look for online reviews and testimonials. You want to find an appraiser who is not only knowledgeable but also professional and easy to work with. Positive feedback often highlights how an appraiser helped clients get the compensation they deserved, turning a stressful situation into a “pain-free” process. Don’t be afraid to ask for references, either. A reputable appraiser will be happy to connect you with past clients. If this process feels overwhelming, remember you don’t have to go it alone. You can always contact us for guidance.

Walking into an appraisal prepared is one of the most effective ways to secure a fair settlement. The insurance company has its own process for valuing your car, but that doesn’t mean you have to accept their number at face value. By doing a little homework, you can build a strong, evidence-based case for what your vehicle was actually worth before the accident. This preparation puts you in a much better position to challenge a low offer and shows the adjuster you mean business. Taking these steps demonstrates that you know your car’s true value and are ready to advocate for the compensation you deserve.

Your car’s history is a huge part of its value. Before the appraisal, pull together all the paperwork you can find that shows you took excellent care of your vehicle. This includes receipts for regular oil changes, tire rotations, and any significant repairs or upgrades. Did you recently buy new tires, install a new sound system, or get the brakes replaced? Find those invoices. This documentation proves your car was in great condition, which can directly counter an insurer’s attempt to undervalue it. These records help paint a clear picture of a well-maintained vehicle, which is essential for any diminished value claim. It’s your proof that your car was worth more than just an average vehicle of its kind.

A picture is worth a thousand words, especially in an insurance claim. Use your phone to take clear, detailed photos of the damage from every possible angle. Get close-ups of specific points of impact and wider shots to show the full extent of the damage. Just as important, find photos of your car from before the accident. Most of us have pictures of our cars from road trips, family events, or even just parked in the driveway. These “before” photos create a powerful side-by-side comparison that leaves no doubt about your car’s previous condition. This visual evidence is hard for an insurance adjuster to ignore and strengthens your argument for a fair payout.

This step is crucial. The insurance company will present you with a list of “comparable” vehicles, or “comps,” to justify their settlement offer. Often, these comps work in their favor; they might be base models, have higher mileage, or be located in cheaper markets. You can fight back by finding your own. Look at online listings for cars that are the same make, model, year, and trim as yours. Pay close attention to vehicles with similar mileage and features in your local area. Having a list of realistic, local comps gives you powerful leverage to challenge a lowball offer. If this research feels overwhelming, you can always get help from an expert to handle the process for you.

Getting an independent appraisal can feel like a big step, but knowing what’s coming makes the process much smoother. An appraiser works for you, not the insurance company, and their goal is to determine the true, fair market value of your vehicle before the accident. They act as your expert, providing a detailed, evidence-based report that reflects your car’s actual worth. This process is your best defense against the quick, often inaccurate valuations that insurance companies rely on to protect their bottom line.

Once you hire an appraiser, they will conduct a thorough inspection of your vehicle. They look beyond the surface-level damage to assess your car’s specific features, condition, mileage, and any aftermarket upgrades. Unlike the automated reports from companies like CCC or Mitchell that insurers often use, a professional appraiser researches current market prices for comparable vehicles in your area. They then compile their findings into a comprehensive report. The entire process, from inspection to final report, typically takes one to two weeks. Your appraiser should keep you updated along the way, ensuring you understand their valuation and how they reached it.

Hiring an independent appraiser is an investment in getting a fair settlement. You can generally expect the cost to be around $500. This fee covers the appraiser’s time for the detailed inspection, market research, and the creation of the formal report. In some cases, your appraiser and the insurance company’s appraiser may not be able to agree on a value. When this happens, a neutral third-party expert, called an “umpire,” is brought in to make a final decision. The cost for the umpire is typically split between you and the insurance company, so it’s a potential extra expense to keep in mind.

Your appraisal report is more than just a document; it’s your most powerful negotiation tool. Once you have it, you can formally submit it to the insurance company as evidence to counter their lowball offer. The report provides a detailed, professional basis for your claim and shows the insurer that you’ve done your homework. You can use it to challenge a low settlement offer and demand the full amount you are owed. Don’t be afraid to stand firm. The facts are on your side, and this report gives you the leverage you need to negotiate effectively.

It’s incredibly frustrating to get a low settlement offer after your car has been totaled. You might feel stuck, but it’s important to remember that the insurance company’s initial offer is just that: a starting point. You don’t have to accept an unfair valuation. You have the right to question their assessment and fight for the full amount you’re owed. By understanding your policy, gathering the right evidence, and knowing how to negotiate, you can take control of the situation and work toward a fair resolution.

Tucked away in your auto insurance policy is a powerful tool you might not know about: the appraisal clause. This provision gives you the right to get an independent appraisal if you disagree with the insurance company’s valuation of your totaled vehicle. Invoking this clause means you hire your own certified appraiser, and the insurance company hires theirs. The two appraisers then work to agree on a value. If they can’t reach an agreement, they will select a neutral third-party appraiser, or an umpire, to make a final, binding decision. This process takes the power out of the insurer’s hands and ensures an unbiased valuation.

Insurance companies are businesses, and their first goal is often to minimize payouts. They frequently use valuation reports from third-party companies that may not accurately reflect your car’s true worth, leading to a lowball offer. Their settlement is based on your car’s Actual Cash Value (ACV), which is what it was worth the moment before the crash. This is calculated by finding the replacement cost and subtracting depreciation. However, their calculation isn’t the final word. You can challenge their ACV by presenting your own evidence that proves your vehicle was worth more than they claim.

Never accept the first offer. Think of it as the opening bid in a negotiation. To counter effectively, you need to build a strong case. Start by gathering your own evidence. Research recent sales of cars with the same make, model, year, and condition in your local area. Print out these listings to use as comparable sales, or “comps.” Get quotes from dealerships and, most importantly, get a report from an independent appraiser. When you communicate with the adjuster, present your evidence clearly and confidently. If you need help navigating this process, our team at Gastley Law is here to handle the property damage claims for you.

When your car is declared a total loss, you’re suddenly thrown into a process filled with confusing terms and procedures. Insurance companies have their own goals, which don’t always align with yours, and this can lead to a lot of misinformation. Let’s clear up a few common myths you might encounter so you can approach your claim with confidence. Knowing the truth is the first step toward getting the fair settlement you’re entitled to.

It’s tempting to accept the first offer and move on, but you should know that first offers are almost always low. Insurance companies are businesses, and their goal is to resolve claims as quickly and inexpensively as possible. They often make an initial settlement offer that’s less than what your claim is truly worth, hoping you’ll take it without asking questions. Accepting that first number means you could be leaving hundreds or even thousands of dollars on the table. It’s always wise to pause, review the offer carefully, and remember that this is just the starting point of a negotiation. Our legal representation is designed to challenge these initial lowball offers.

The entire dispute over a total loss settlement often comes down to one thing: the insurer’s valuation, or Actual Cash Value (ACV). This figure is supposed to represent what your car was worth moments before the crash. To determine this, adjusters use “comps,” which are comparable vehicles for sale in the market. The problem is that their reports are frequently filled with comps that work in their favor. They might use base models instead of your upgraded trim, cars with much higher mileage, or listings from cheaper markets hundreds of miles away. This is a common tactic used to justify a lower vehicle value and, ultimately, a smaller payout for you.

You never have to accept the insurance company’s first offer, or any offer that you believe is unfair. You have the right to negotiate for a better settlement, and in fact, most insurance adjusters expect you to. If you don’t agree with their valuation, you can and should push back with your own evidence, like an independent appraisal report and your own research on comparable vehicles. Don’t let the insurer pressure you into a quick decision. If you feel overwhelmed or that the insurance company isn’t treating you fairly, it might be time to get in touch with an expert who can advocate on your behalf.

Handling a total loss claim can feel like a full-time job, and sometimes, despite your best efforts, you hit a wall. You’ve gathered your documents, done your research, and presented your case, but the insurance company just won’t budge. This is often the point where having a professional in your corner can make all the difference. While you can certainly handle many parts of the process yourself, certain situations call for legal expertise. Knowing the signs can help you decide when to pass the baton to an attorney who can fight for you.

The most obvious red flag is a dispute over your vehicle’s value. These disagreements happen because the insurer’s valuation, what they call the Actual Cash Value (ACV), often doesn’t match what your vehicle was actually worth right before the accident. If the insurance company’s offer seems shockingly low, or if they deny your claim without a clear and fair reason, it’s time to be concerned. Other warning signs include the adjuster using inappropriate comparable vehicles to justify their low offer, ignoring your evidence, or pressuring you into a quick decision. An unresponsive adjuster who dodges your calls and emails is also a major red flag. These tactics are designed to wear you down, but you don’t have to accept them.

If you don’t agree with the insurance company’s offer, you can try to negotiate for more money, but this is where a lawyer’s experience becomes invaluable. An attorney does more than just negotiate; they build a comprehensive case to prove your car’s true value. They can counter the insurer’s lowball appraisal with a detailed report from a trusted independent appraiser and compile all the necessary evidence to support a higher payout. A lawyer specializing in property damage claims knows exactly what documentation is needed and how to present it in a formal demand letter. This professional approach signals to the insurer that you are serious about getting a fair settlement.

Beyond the financial outcome, having a lawyer levels the playing field. Insurance companies have teams of adjusters and lawyers working to protect their bottom line. An attorney acts as your personal advocate, ensuring your rights are protected throughout the process. They understand the insurance company’s tactics and know how to properly value your claim. This takes the stress and burden off your shoulders. You no longer have to spend hours on the phone or deciphering complex paperwork. Instead, you can focus on getting back to your life while a professional handles the fight for you. If you’re feeling overwhelmed or believe you’re being treated unfairly, that’s your cue to contact a professional who can step in and take over.

Yes, you almost always do. The insurance company’s appraiser works for them, and their valuation is often designed to save the company money. An independent appraiser works for you. Their job is to determine your car’s true market value based on its specific condition, features, and local sales data. Getting your own appraisal is the most effective way to counter a low offer with a credible, evidence-based report.

Think of it as an investment. While it feels like another expense, that $500 fee can often lead to a settlement that is thousands of dollars higher than the insurer’s initial offer. Without a professional report to back you up, you have very little leverage to negotiate. The appraisal provides the proof you need to justify a higher payout, so the cost is often recovered many times over in the final settlement.

The very first thing you should do is pause. Do not accept the offer or sign anything. Your next step is to politely inform the adjuster in writing, like in an email, that you do not accept their valuation and will be reviewing it. This gives you time to gather your own evidence, like maintenance records and research on comparable vehicles, without feeling pressured into a quick and unfair decision.

Insurers often overlook aftermarket parts or try to undervalue them. It’s your job to prove their value. Gather every receipt and photo you have for things like new tires, a custom stereo, or performance parts. While a standard policy might have limits, these upgrades absolutely contribute to your car’s pre-accident value. An independent appraiser will factor these into their report, giving you the documentation needed to fight for compensation for the money you invested.

You can certainly start the process on your own by gathering documents and getting an independent appraisal. However, if the insurance company refuses to negotiate in good faith, denies your claim unfairly, or uses delay tactics, it’s a good sign you need professional help. A lawyer can take over the communication, apply legal pressure, and manage the entire fight for you, which often leads to a better outcome and saves you a lot of stress.