Insurance companies are experts at protecting their bottom line, which can often result in lowball offers for your property damage or diminished value claim. But you have rights and tools at your disposal. The appraisal clause is one of the most effective ways to level the playing field. It allows you to take the power back from the insurance adjuster and place the valuation dispute into the hands of competent, independent appraisers. When you formally invoke appraisal clause, you are enforcing a contractual right to a fair and unbiased assessment of your loss. We are Atlanta’s top rated Diminished Value Claim experts, and we put together this guide will show you how to use this process to your advantage and fight for the full compensation you are owed.

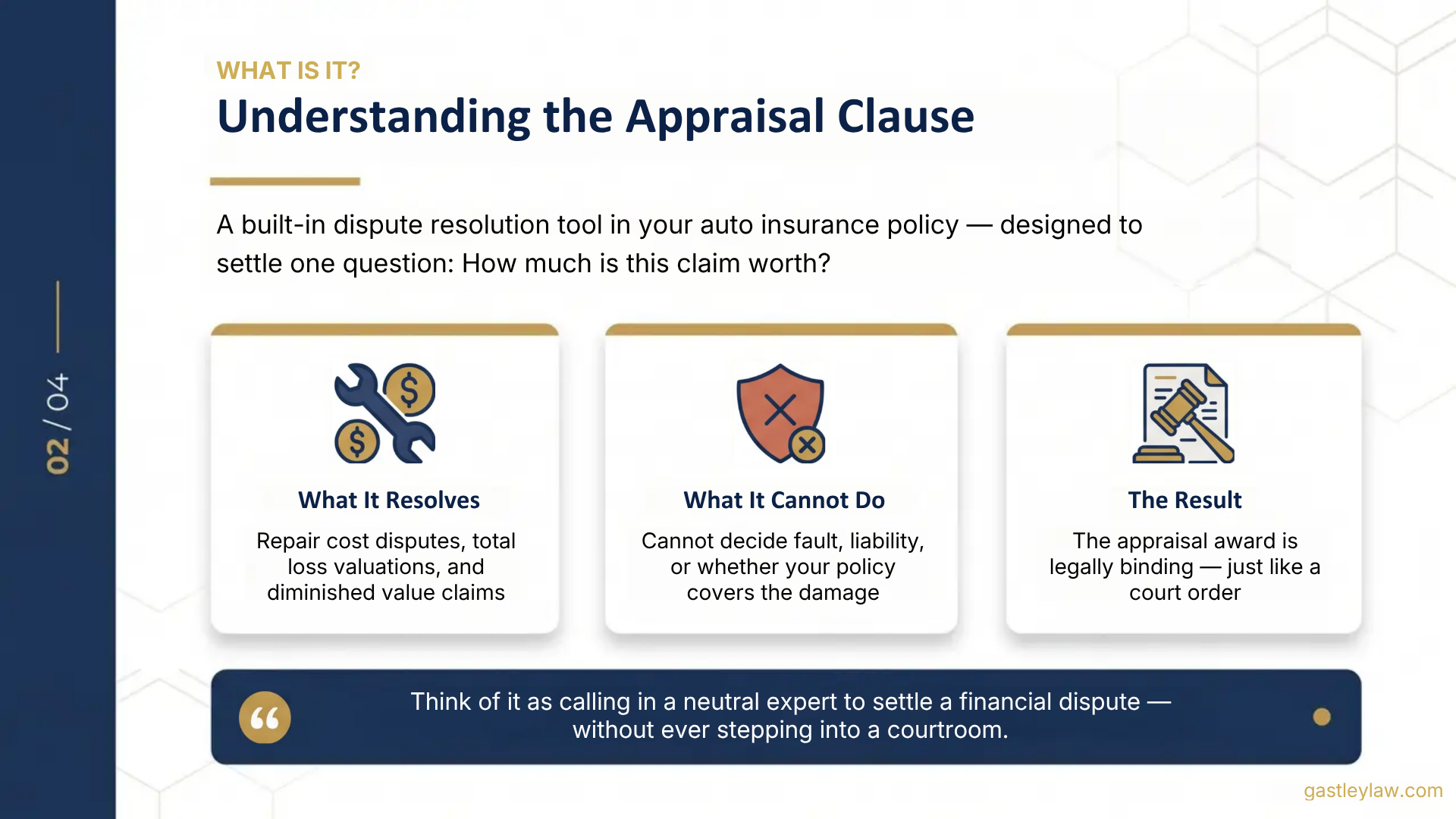

When you and your insurance company can’t agree on the cost of your car’s repairs or its value, it can feel like you’ve hit a wall. That’s where the appraisal clause comes in. Think of it as a dispute resolution tool built directly into your auto insurance policy. It’s designed to provide a fair, expert-driven answer to one specific question: How much is this claim worth? Invoking this clause kicks off a formal process where each side hires an independent appraiser to assess the damages and agree on a final amount, without having to go to court.

The appraisal clause has a very specific job: it’s used to settle disagreements about the amount of a loss. If you believe your car repairs will cost $8,000 but your insurer is only offering $5,000, appraisal is the perfect tool to resolve that dollar-figure dispute. However, its power is limited. Appraisers cannot decide who is at fault for an accident (liability), or whether your policy covers the damage in the first place (coverage). Their only role is to determine the value of the damage. It’s also important to know that the outcome of an appraisal is typically final and legally binding, which means you can’t easily challenge the decision later.

Choosing between appraisal and a lawsuit is a big decision. The appraisal process is often much quicker and less expensive than a full lawsuit, saving you time and legal fees. Instead of judges and juries, you have impartial industry experts evaluating your vehicle’s damage. The final decision, called the “award,” is just as binding as a court order. The main trade-off is control. Once you hand the dispute over to the appraisers and an umpire (a neutral third party), the final number is out of your hands. A lawsuit, while longer and more costly, allows for a broader examination of your case, including potential bad faith claims against the insurer.

Knowing when to play your cards is half the battle. The appraisal clause isn’t for every disagreement with your insurer, but it’s a powerful tool when you’re at a standstill over the dollar amount of your claim. Think of it as calling in a neutral expert to settle a financial dispute. If you and the insurance adjuster are miles apart on the value of your damages, it might be the right time to formally invoke this part of your policy. This process is specifically designed to resolve disagreements about the value of your loss, providing a structured path forward when negotiations have stalled.

This is one of the most common reasons to use the appraisal clause. You’ve taken your car to a trusted body shop and received a detailed estimate for quality repairs. Then, the insurance company’s adjuster comes back with a much lower number, often suggesting cheaper parts or a faster repair process. When there’s a significant gap between your mechanic’s professional opinion and the insurer’s offer, you’re not just stuck. The appraisal clause allows you to bring in an independent expert to assess the necessary property damage repairs and determine a fair cost, breaking the stalemate.

If your car is declared a total loss, the insurance company is supposed to pay you its Actual Cash Value (ACV). The problem is, their idea of your car’s value might not match reality. Insurers often use valuation reports that can undervalue your vehicle, leaving you with a check that isn’t enough to buy a comparable replacement. If you’ve done your research and believe their total loss offer is unfairly low, the appraisal clause is your next step. It creates a formal process for two independent appraisers to determine the true market value of your car just before the accident.

Even after the best repairs, a car with an accident history is worth less than one without. This loss in resale value is called diminished value, and you’re entitled to compensation for it. Unfortunately, insurance companies are notorious for making lowball offers or denying these claims altogether. The appraisal clause is an excellent way to fight back. It allows an unbiased expert to assess exactly how much value your car has lost due to the accident. This is especially critical for newer or high-value vehicles, where the diminished value can be substantial.

It’s crucial to understand what the appraisal clause can and cannot do. This process is strictly for disputes over the amount of your loss. It can determine the cost of a repair, the value of your totaled car, or the amount of diminished value. However, it cannot resolve disagreements about your policy’s coverage. For example, appraisal can’t decide if your policy covers hail damage in the first place, but it can determine the cost to fix it if it is covered. If your insurer denies your claim based on a coverage issue, you’ll need to explore other options and should contact an attorney to review your policy.

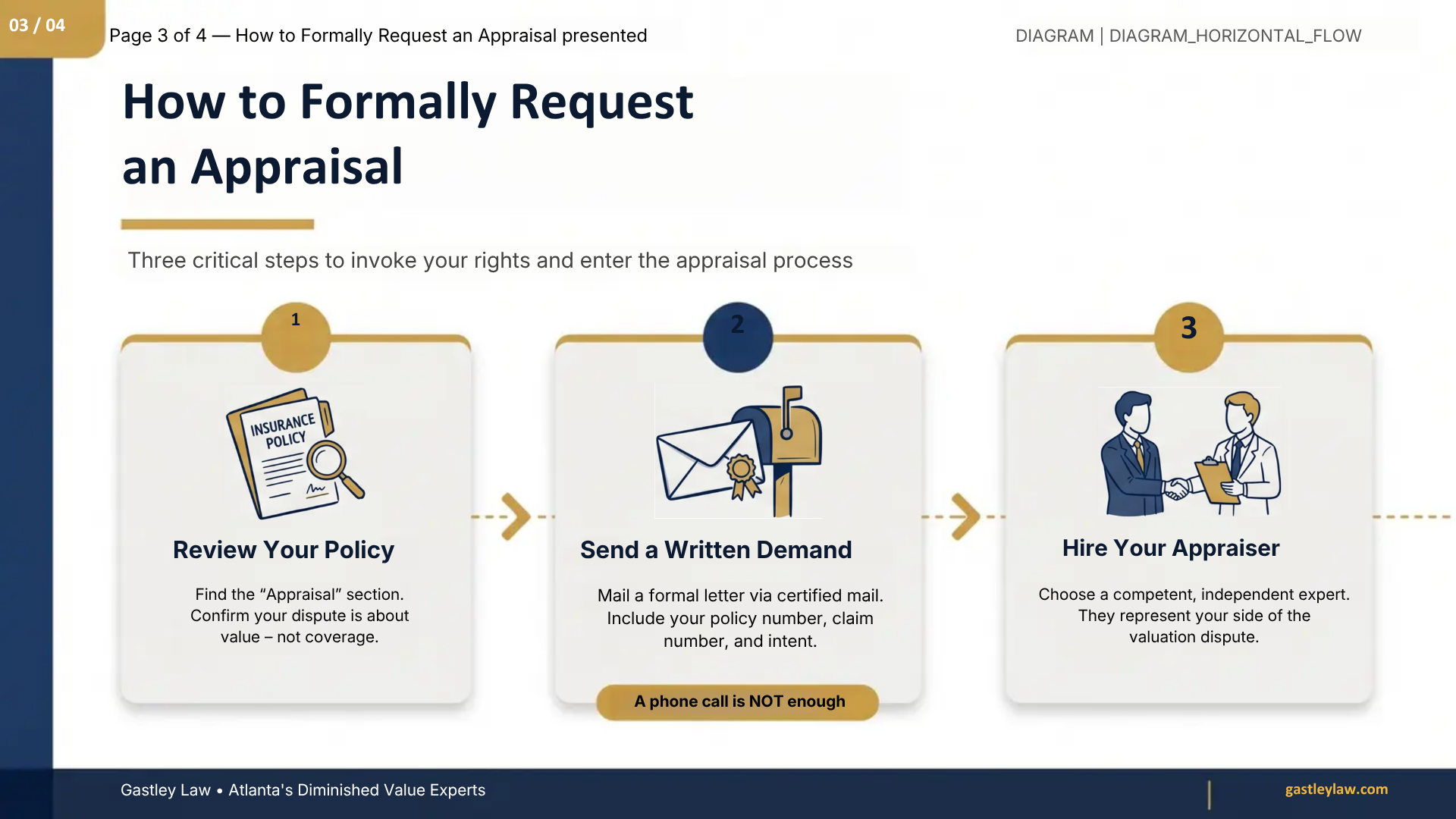

If you and the insurance company are at a standstill over the value of your vehicle’s damage or loss, invoking the appraisal clause is your next official step. This isn’t a casual phone call; it’s a formal process outlined in your policy that requires you to follow specific procedures. Think of it as calling in neutral experts to settle a financial disagreement when negotiations have failed. It’s a powerful tool for getting a fair assessment, but you have to kickstart the process correctly. Let’s walk through exactly how to do that, step by step, so you can feel confident you’re handling it the right way from the very beginning.

First, pull out your insurance policy documents (yes, the big packet of paper or the long PDF you probably haven’t looked at since you signed up). You’re looking for a section specifically titled “Appraisal.” Read this part carefully. It will explain your right to demand an appraisal if you disagree with the insurer’s assessment of the “amount of loss.” It’s important to confirm that your dispute is about valuation, like the cost of repairs or your car’s diminished value, and not about whether something is covered in the first place. The appraisal clause only settles disagreements over the dollar amount, not over coverage itself.

Your next move is to formally notify the insurance company that you are invoking the appraisal clause. You must do this in writing. A phone call or an email isn’t enough. Draft a letter that clearly states your intention to invoke the appraisal clause for your claim. Be sure to include your full name, policy number, and the claim number associated with the incident. It’s also a good idea to name your chosen appraiser in this letter if you already have one. Send this letter via certified mail with a return receipt requested. This gives you undeniable proof that the insurance company received your demand.

Now it’s time to select your champion for this process. You need to hire a competent, independent appraiser to represent your side. “Competent” means they have deep knowledge of vehicle repair costs and market values. “Independent” means they have no personal or financial stake in the outcome, ensuring their assessment is unbiased. This is not a job for a friend who knows a bit about cars; you need a true professional. You are responsible for paying for your appraiser’s services, so be sure to vet them thoroughly. Our team can often provide guidance on finding a qualified expert for your property damage claim.

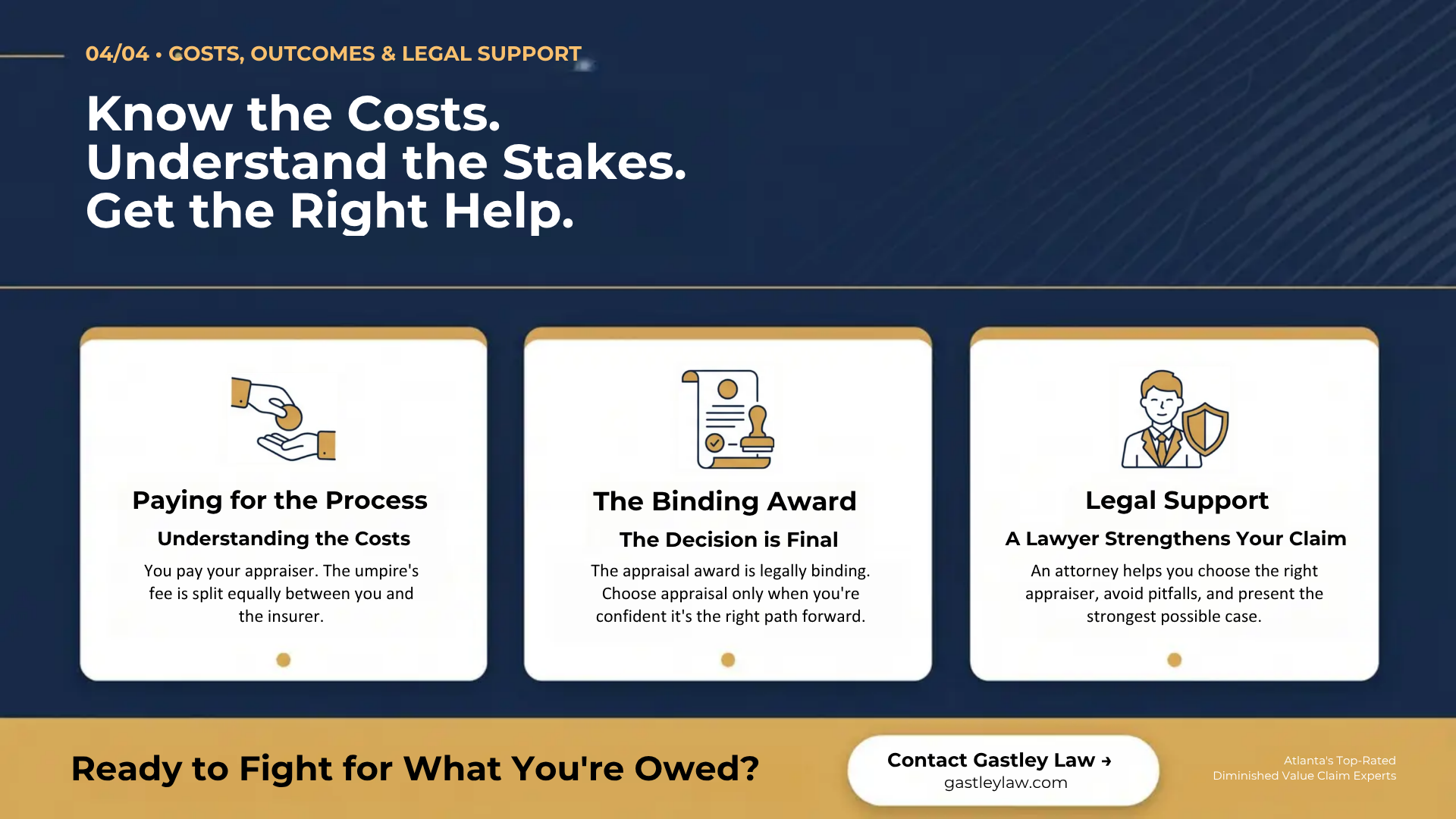

It’s important to set realistic expectations for how long this process can take. Invoking the appraisal clause doesn’t lead to an overnight solution. It can take several weeks or even months just for both sides to select their appraisers and for those appraisers to agree on a neutral third party, called an umpire. You’ll also need to be prepared for the costs. As mentioned, you pay for your own appraiser, the insurance company pays for theirs, and you both split the cost of the umpire’s fee. Keep all your paperwork organized and be ready for a bit of a wait.

Once you decide to invoke the appraisal clause, it’s helpful to know what comes next. The process involves some financial costs and requires you to take an active role. Let’s walk through what you can expect, so you can feel prepared and confident every step of the way. Understanding these key responsibilities will help you manage the process effectively and work toward the fair settlement you deserve.

The first thing to know is that you are responsible for hiring and paying for your own appraiser. Think of this as an investment in your claim. While it is an out-of-pocket expense, a qualified, independent appraiser is your expert advocate. They have the specific knowledge to accurately assess your vehicle’s value and build a strong argument against the insurer’s low offer. Choosing a reputable professional is one of the most important decisions you’ll make in this process, as their expertise directly influences the outcome.

If your appraiser and the insurance company’s appraiser can’t agree on a value, a neutral third party called an umpire steps in to make the final decision. The good news is you don’t have to cover this cost alone. The standard practice is that each side pays for their own appraiser, and you split the cost of the umpire with the insurance company. This cost-sharing structure is designed to keep the process impartial, ensuring that the final decision-maker isn’t financially tied to one side or the other.

Your appraiser will be your champion, but they need the right tools to fight for you. That’s where your evidence comes in. Your job is to gather all relevant paperwork, including repair estimates, photos of the damage, and any records that show your car’s condition and value. For a diminished value claim, this documentation is especially important. Your appraiser and the insurer’s appraiser will review this evidence to agree on a fair value, so the more thorough you are, the stronger your case will be.

It’s important to be realistic about the timeline. The appraisal process isn’t always quick; it can sometimes take six months to over a year to complete. This is often due to scheduling, detailed evidence reviews, and back-and-forth negotiations. While waiting can be frustrating, remember that a thorough process is often necessary for a fair outcome. Having an experienced legal team on your side can help manage the process and keep things moving forward. If you have questions about your specific case, our team is here to help you understand your legal options.

Deciding whether to invoke the appraisal clause is a big step, and it’s smart to look at it from all angles. While it can be a powerful tool to get a fair settlement, it isn’t the right fit for every situation. Understanding the benefits and drawbacks helps you make an informed choice about how to handle your property damage claim. Let’s walk through what you can expect so you can feel confident in your decision.

One of the biggest advantages of the appraisal process is that it’s often much faster and less expensive than filing a lawsuit. Court battles can drag on for months or even years, but appraisal is designed to reach a resolution more efficiently. Instead of relying on judges or juries, your case is put in the hands of impartial experts who live and breathe vehicle valuations. This is especially helpful for complex financial losses, like a tricky diminished value calculation, because the people making the decision already understand the specific calculations involved. It takes the guesswork out of the equation and focuses on getting an accurate number from qualified professionals.

The appraisal clause has its limits. It can only be used to settle disagreements about the amount of your loss. It can’t be used to decide if something is covered by your policy in the first place. For example, if the insurance company agrees your car needs a new bumper but you disagree on the cost, appraisal can help. But if they deny coverage for the bumper entirely, appraisal isn’t the right tool. It’s also important to know that once an appraisal award is made, it’s typically final and legally binding. This is great if the outcome is in your favor, but it leaves little room for appeal if you’re unhappy with the result.

Let’s clear up a few common misconceptions. First, don’t assume the insurance company’s initial offer is a fair assessment of your car’s worth. Lowball offers are a common business tactic designed to save the insurer money. It’s your right to challenge an offer you believe is too low. Second, the process isn’t free. You are responsible for paying for your own appraiser, and the costs for the neutral third-party appraiser, called an umpire, are usually split between you and the insurance company. Knowing these costs upfront helps you prepare financially for the process. If you have questions about what to expect, it’s always a good idea to get in touch with an attorney first.

While the appraisal clause is a powerful tool, it’s not something you should jump into without a plan. The process is binding, and once a decision is made, it’s final. This is why having a professional in your corner can make all the difference. An experienced attorney can help you decide if invoking appraisal is the right move and guide you through each step to ensure you’re treated fairly. For valuation disputes involving repairs or diminished value, an experienced Atlanta diminished value attorney can help protect your interests and present a stronger claim. Think of it as bringing a seasoned expert to a negotiation where the other side already has a team of them.

Before you even think about sending that formal demand letter, your first call should be to an attorney. A quick consultation can help you understand the potential outcomes and whether the appraisal process is truly the best path for your specific situation. An attorney can review your policy and the insurer’s offer to give you a clear picture of what’s at stake. This initial conversation is a low-risk way to get professional advice before you commit to a binding process. It’s about making an informed decision, not just a fast one. Getting an expert opinion on your property damage claim is a crucial first step.

Hiring an attorney does more than just give you advice; it actively strengthens your position. An experienced lawyer knows the ins and outs of the appraisal process and can help you present your case in the most effective way. They can connect you with a qualified, impartial appraiser who has a deep understanding of vehicle values. This is especially important for complex situations like a diminished value claim, where proving the loss requires specific expertise. With a lawyer guiding you, you stand a much better chance of achieving a fair outcome against a well-prepared insurance company.

Throughout the appraisal process, your primary goal is to protect your rights, and a lawyer is your best advocate for doing just that. They ensure that every decision made aligns with your best interests and that the insurance company follows the rules. While the appraisal process can be a straightforward way to settle a dispute, there are potential pitfalls. A lawyer helps you avoid them. They review all paperwork, manage communications, and make sure the final agreement is fair and just. If you’re ready to get started or have questions, you can always contact our team for guidance.

Deciding to invoke the appraisal clause is a significant step in your insurance claim. It’s a powerful tool, but it isn’t the right fit for every situation. Before you send that formal demand letter, it’s crucial to weigh the potential outcomes and understand what the process truly involves. This isn’t just about getting a second opinion; it’s about entering a formal, binding process that will determine the final payout for your vehicle’s damages or value. Taking a moment to consider your specific circumstances, explore alternatives, and prepare properly can make all the difference in reaching a fair resolution.

The main benefit of the appraisal clause is that it can resolve a dispute over the dollar amount of your loss without a lengthy court battle. However, it’s important to know its limits. Appraisal is only appropriate when the disagreement is strictly about the amount of the loss, like the cost of repairs or your car’s diminished value. It cannot be used to settle disputes over whether something is covered by your policy in the first place. Another key point to remember is that the appraisal award is typically final and binding. This means if you’re unhappy with the outcome, you have very limited options to challenge it later, so you have to be confident it’s the right move.

Before committing to appraisal, consider if it’s truly necessary. If the difference between your estimate and the insurer’s offer is relatively small, the cost of hiring an appraiser and potentially an umpire might cancel out any extra money you receive. For many people, the best first step is to speak with an attorney who handles property damage claims. A lawyer can often negotiate a fair settlement directly with the insurance company on your behalf, saving you the time and expense of the formal appraisal process. They can also help you understand all your legal options and build the strongest possible case for the compensation you deserve from the start.

If you and your attorney decide that invoking appraisal is the best path forward, you need to follow the correct procedure. First, you must send a formal written demand to your insurer by certified mail, which creates a record that you sent it. This letter should clearly state your intent to invoke the appraisal clause and include your policy number, claim number, and the name of your chosen appraiser. Selecting the right appraiser is critical. You need an independent, impartial expert who is skilled in valuing vehicles and negotiating claims. Your attorney can help you find a qualified professional and guide you through all the necessary legal steps to protect your rights.

Yes, you can. The appraisal clause is part of your own insurance policy and deals with disagreements over the value of your property damage claim. It has nothing to do with who was at fault for the accident. If you file a claim under your own collision coverage and you believe your insurer’s offer for repairs or your car’s total loss value is too low, you have the right to invoke appraisal to get a fair assessment.

While the goal of invoking appraisal is to get a fair valuation that is often higher than an insurer’s lowball offer, there is no guarantee. The process is handled by independent experts who assess the value based on evidence. The final award could be higher, lower, or the same as the original offer. This is why it’s so important to have a strong case with solid documentation and to hire a competent appraiser who can effectively argue for your vehicle’s true value.

This is a very common part of the process and exactly why a neutral third party, called an umpire, is selected. If your appraiser and the insurance company’s appraiser reach a stalemate, they will submit their different assessments to the umpire. The umpire then reviews the evidence and arguments from both sides. A final decision, or “award,” is made when any two of the three parties (your appraiser, the insurer’s appraiser, or the umpire) agree on a specific dollar amount.

Finding the right appraiser is one of the most critical steps. You should look for a professional with extensive experience in auto body repair, damage estimation, and vehicle valuation. They should also be independent, meaning they don’t have a regular business relationship with your insurance company. A good place to start is by asking for recommendations from trusted mechanics or by seeking guidance from an attorney who specializes in property damage claims, as they often have a network of vetted experts.

If your policy includes an appraisal clause and your dispute is clearly about the amount of loss, your insurance company is contractually obligated to participate in the process. If they ignore your written demand or refuse to name their own appraiser, they may be acting in bad faith. In this situation, you should contact an attorney immediately. A lawyer can intervene on your behalf, compel the insurer to comply with the terms of the policy, and protect your rights.