Let’s talk about the financial damage that happens the moment of impact—the damage that doesn’t get fixed at the body shop. This is your car’s diminished value, the permanent loss in its market worth because of its new accident history. The at-fault driver’s insurance company is responsible for making you whole, and that includes paying for this loss. But they are counting on you not knowing your rights or being too intimidated to fight back. This guide demystifies the entire process, showing you exactly how to calculate your loss and file a small claims court diminished value claim to recover the money that is rightfully yours.

Let’s talk about a term the insurance company probably won’t bring up after an accident: diminished value. In simple terms, it’s the loss in your car’s market value after it’s been in a wreck. Even if a top-notch body shop restores your car to pristine condition, it now has an accident history. That history makes it less attractive to future buyers, and they will pay less for it compared to an identical car that’s never been damaged. This difference in value is real money that you’ve lost, and in Georgia, you have the right to claim it from the at-fault party’s insurance.

Think of it this way: you didn’t ask to be in an accident, and you shouldn’t be left with a car that’s worth less because of someone else’s mistake. The insurance company’s job is to make you whole again, and that includes compensating you for this loss in value. Understanding what diminished value is is the first step toward making sure you get the full compensation you deserve. It’s not just about fixing the dents; it’s about restoring the financial value you lost the moment the collision happened. Many people accept the repair check and assume that’s the end of it, not realizing they’re leaving hundreds or even thousands of dollars on the table.

When you go to sell or trade in your car, potential buyers will almost certainly pull a vehicle history report from a service like CARFAX. An accident on that report is a major red flag. Even with perfect repairs, a buyer will always choose the car with a clean history over one that’s been in a wreck, or they’ll expect a significant discount. This immediate drop in resale value is the core of your diminished value claim. The accident permanently taints your car’s record, and that stigma directly impacts what someone is willing to pay for it down the line. It’s an invisible form of damage that can cost you dearly when it’s time to sell.

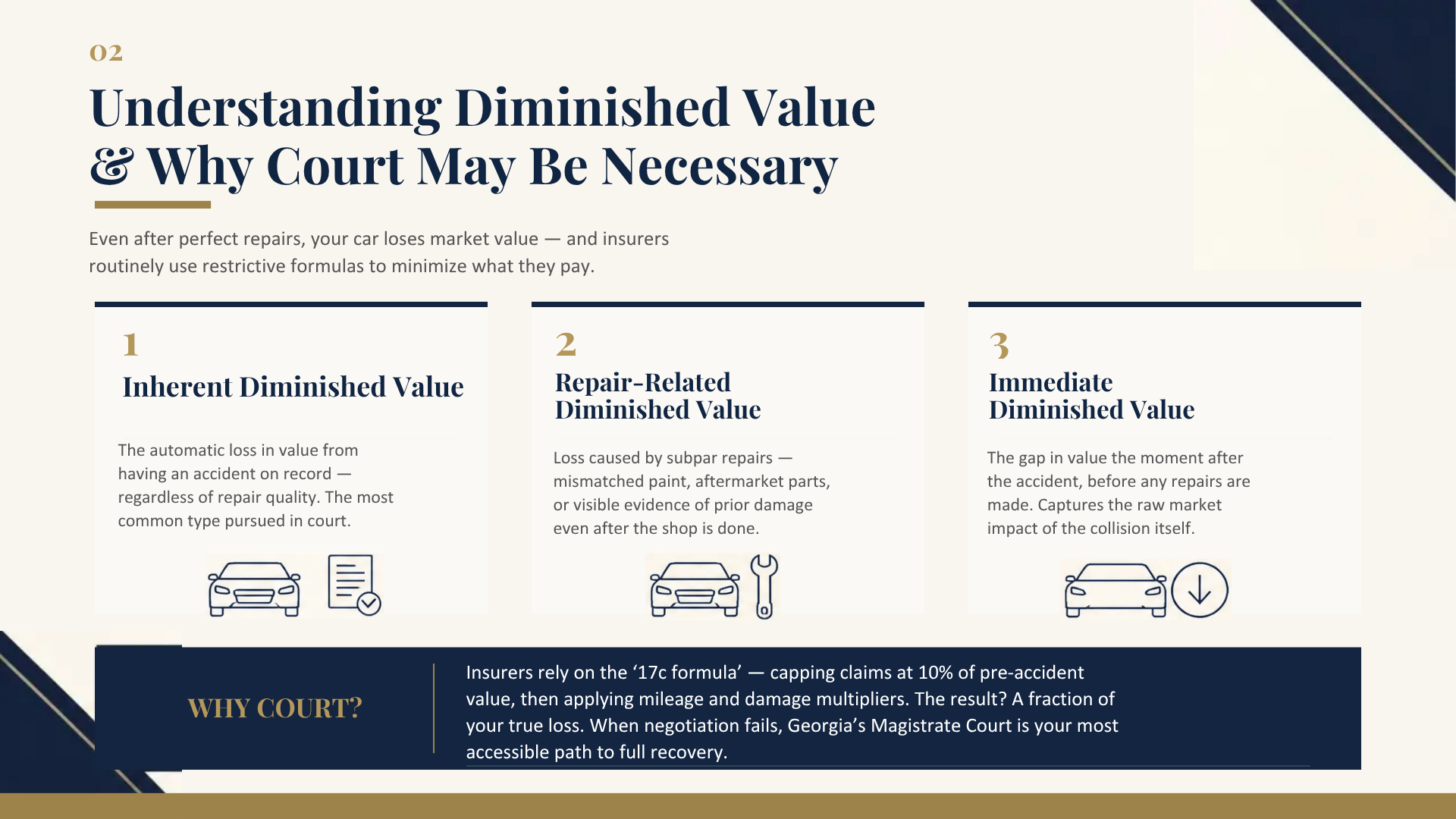

Diminished value isn’t a one-size-fits-all concept. It generally falls into three categories, and knowing the difference helps you understand your claim.

Most property damage claims focus on inherent diminished value, as it’s the most direct and undeniable financial loss you suffer.

Figuring out your car’s diminished value isn’t about guesswork; it’s about proving a concrete financial loss. After an accident, your car is simply worth less, even after perfect repairs. The challenge is putting an accurate dollar amount on that loss. Insurance companies have their preferred methods, which often favor them, not you. But understanding how these calculations work—and knowing what other factors are at play—is the first step toward building a strong claim and getting the money you’re owed.

The goal is to show the difference between your car’s market value before the accident and its value after the repairs are done. An accident history permanently attaches to your vehicle’s record, and any informed buyer will pay less for it compared to an identical car with a clean history. This is the value you’ve lost, and you have a right to be compensated for it. Let’s walk through the common formula insurers use and, more importantly, the real-world factors that truly determine your car’s lost value.

Insurance companies in Georgia often lean on a calculation known as the “17c formula.” It’s important to know how it works because this is likely the first number they’ll throw at you. First, they determine your car’s pre-accident value using a guide like Kelley Blue Book. Then, they cap the maximum diminished value at 10% of that amount. Finally, they apply a “damage multiplier” (from 0.00 to 1.00) based on the severity of the damage and a “mileage multiplier” to reduce the payout further. This formula almost always results in a lowball offer, as it’s designed with built-in limits that protect the insurance company’s bottom line, not your car’s actual market value.

While the insurance company is focused on their formula, the real world looks at a car’s value differently. Several key factors determine what diminished value is in a practical sense. The make, model, age, and mileage of your vehicle play a huge role. A newer, luxury vehicle will lose significantly more value than an older, high-mileage car. The severity and type of damage are also critical—a car with structural frame damage will suffer a much greater loss in value than one with minor cosmetic issues, even if the repairs look flawless. The simple fact that your car now has an accident history is the biggest factor of all, and it’s what a potential buyer will focus on.

Because the 17c formula is so restrictive, your strongest piece of evidence is an independent appraisal from a certified expert. A professional appraiser doesn’t rely on a rigid formula. Instead, they conduct a detailed analysis of your vehicle and the current market. They compare your repaired car to similar vehicles that have never been in an accident to establish a true, fair market value. This appraisal report provides the unbiased, expert documentation you need to challenge the insurance company’s low offer. It transforms your claim from your opinion into a fact-based argument, which is essential for negotiations or if you end up in court.

Deciding where to file your diminished value claim is a big step. While a full-blown lawsuit has its place, small claims court is often a more direct and less intimidating path for many people. It’s designed to be a simpler legal process, allowing you to present your case without getting tangled in complex procedures. Think of it as a more streamlined way to get a judge to hear your side of the story and make a binding decision.

However, it’s not the right fit for every situation. The key is understanding if the specifics of your case align with what small claims court is designed to handle. This involves looking at the value of your claim, knowing the local rules, and making sure you’re pointing your legal finger at the right person. Getting these details right from the start can make all the difference between a frustrating experience and a successful outcome.

Small claims court is your best bet when the amount of money you’ve lost falls within a specific limit set by the state. If your professional appraisal shows your car’s diminished value is below that threshold, this is likely the most efficient route. The process is intentionally less formal than higher courts, which means you can often resolve your case faster and with fewer expenses. You don’t typically need a lawyer to represent you, which saves on legal fees. It’s an excellent option for straightforward claims where you have clear evidence and just need a neutral third party to make a final call.

Here in Georgia, the small claims court—officially known as Magistrate Court—has a monetary limit of $15,000. This is great news for many diminished value claims, as it’s a relatively high ceiling compared to other states. If your car lost $15,000 or less in value after an accident, you can file your case here. This allows you to seek fair compensation without the cost and complexity of a Superior or State Court lawsuit. Understanding these local court rules is the first step in building a solid strategy for your claim.

Georgia Magistrate Court limit: Georgia Magistrate Court generally handles civil claims of $15,000 or less. Review the official Georgia Courts Magistrate Court resource for court information and forms, and verify venue, current forms, and filing fees with the relevant court before filing.

This is a critical detail that trips many people up: you don’t sue the insurance company. You file the lawsuit against the at-fault driver—the person who actually caused the accident. Their insurance company has a duty to defend them and pay for covered claims, but your legal dispute is with the individual policyholder. If a commercial vehicle was involved, you would typically sue both the driver and the company they work for. Naming the correct defendant is a non-negotiable step for your case to proceed, and getting it right ensures you’re targeting the legally responsible party for your property damage claim.

Winning a diminished value claim is all about showing, not just telling. The stronger your evidence, the harder it is for the insurance company to argue with your number. Think of yourself as a detective building an open-and-shut case. Your job is to collect clear, undeniable proof that the accident caused a specific financial loss. This means gathering documents that tell the complete story of your car’s value—before the crash, during the repairs, and after it’s been fixed.

A solid paper trail is your best friend in small claims court. It removes guesswork and replaces it with facts. When you can present a judge with a logical progression of evidence, from pre-accident value reports to a professional appraisal, you build a compelling argument that is difficult to refute. Let’s walk through the essential pieces of evidence you’ll need to collect to build a powerful claim.

First things first, you need to establish what your car was worth moments before the accident. This is your baseline. Your goal is to paint a clear picture of a well-maintained vehicle that held a specific market value. Start by getting a value report from a reputable source like Kelley Blue Book or NADAguides. Be sure to print this out, noting the car’s condition, mileage, and options accurately. If you have recent maintenance records or the original bill of sale, add those to your file. This paperwork helps prove your car’s pre-accident condition and solidifies your understanding of what diminished value is—the drop from this specific starting point.

After the accident, every document from the body shop is a crucial piece of your evidence puzzle. Keep absolutely everything. This includes the initial estimate, any supplemental repair orders (which often happen when more damage is found), and the final, itemized invoice. This invoice is especially important because it details exactly which parts were repaired versus replaced and the total labor costs. Don’t forget to take your own photos of the damage before the repairs begin. A clear visual record of the impact can be incredibly powerful when paired with the technical details of the repair bill.

Now, you need to show how the market treats cars with an accident history. The best way to do this is with real-world examples. Search for used car listings for vehicles that are the same make, model, year, and trim as yours. Print out a few examples of cars with clean histories and similar mileage, and then find a few with reported accidents. The price difference is a tangible demonstration of diminished value. You can also visit a couple of dealerships and ask for a written trade-in quote, making sure you tell them about the accident. A lower offer that specifically notes the accident history is powerful proof.

While the evidence you gather is essential, a report from a certified appraiser is often the key to winning your case. This is an unbiased, expert opinion that insurance companies and judges take seriously. A professional appraiser will conduct a thorough inspection of your vehicle and its repair records, then use industry-standard methodologies to calculate the exact amount of value it has lost. This report transforms your claim from an educated guess into a documented, expert-backed figure. If you’re serious about getting what you’re owed, investing in a professional appraisal gives your claim the credibility it needs to succeed. If you need help finding a reputable appraiser, you can always contact us for guidance.

Taking an insurance company to court might sound like a huge undertaking, but when you break it down, it’s a series of manageable steps. Filing in small claims court is designed to be a more straightforward process than a traditional lawsuit. Your main job is to build a clear, logical case supported by solid evidence. Think of it as telling a story to the judge, with your documents and photos as the proof. Let’s walk through exactly what you need to do to get your claim filed correctly.

This is where you build the foundation of your case. The judge can’t just take your word for it—you have to prove how much value your car lost because of the accident. Start by gathering everything that shows your car’s value before the crash, using resources like Kelley Blue Book. You’ll also need all your accident-related documents, including the police report and photos of the damage. Most importantly, you need a professional diminished value appraisal. This report, prepared by an expert, is the strongest piece of evidence you can have to show the court exactly how much money you’re owed.

Every state has a strict time limit for filing a lawsuit, known as the statute of limitations. In Georgia, you have four years from the date of the accident to file a claim for property damage. If you miss this deadline, you lose your right to sue, no matter how strong your case is. You’ll also need to pay a filing fee, which varies by county. The best way to find the exact cost and get the right forms is to visit the website for your local magistrate court, which is what Georgia calls its small claims court. You can find your local court through the official Georgia Magistrate Courts directory.

Once you file your claim, you have to formally notify the person or company you are suing. This is called “serving” them, and you can’t just drop the papers in the mail. You’ll need to have the sheriff’s department or a private process server deliver the documents. If you’re suing an insurance company, you can’t just serve any employee; you have to serve their official “registered agent.” You can find the name and address for any company’s registered agent by doing a quick business search on the Georgia Secretary of State’s website. This ensures your lawsuit is delivered to the right person and your case can move forward.

Walking into a courtroom can feel intimidating, but small claims court is designed to be more accessible than a major trial. The judge’s goal is to hear both sides of the story and make a fair decision based on the evidence presented. This is your opportunity to explain, in your own words, why you are owed compensation for your car’s lost value.

Your job is to present a clear, logical case supported by the evidence you’ve gathered. You don’t need to be a legal expert, but you do need to be prepared. The insurance company will send a representative who does this for a living, so having your facts straight is non-negotiable. They will try to poke holes in your argument, but a well-organized case built on solid proof is your best defense. Think of it as telling a story to the judge—the story of your car’s value before the accident, how the accident impacted it, and what you’re owed as a result.

If you decide to sue, you need strong evidence to show exactly how much money your car lost in value and why you deserve that amount. Before your court date, organize all your documents into a binder or folder with clear labels. This includes your appraisal report, repair invoices, photos, and any communications with the insurance company. Practice explaining your case out loud from start to finish. This will help you feel more confident and ensure you don’t forget any key points. Also, remember that small claims courts have a limit on how much money you can ask for. In Georgia, Magistrate Court generally handles civil claims of $15,000 or less, so confirm venue, current forms, and filing fees with the relevant court before filing. Understanding the basics of diminished value is the first step to building a solid case.

When it’s your turn to speak, your goal is to be clear and concise. The judge is busy, so get straight to the point. Start by explaining what happened and how much diminished value you are claiming. Then, walk the judge through your evidence. You’ll need proof like your professional appraisal, sales prices of similar cars (some with accident histories, some without), and quotes from dealers showing they would offer less for your car because of the accident. It’s also incredibly helpful to have photos of your car from before the accident and a log of your maintenance records to prove it was in great condition. Present your evidence calmly and stick to the facts. Let your documentation do the heavy lifting.

Be prepared for the insurance company’s defense. They handle these claims every day and have a standard playbook. A common argument is that since your car was repaired, it’s now “good as new.” This completely ignores the reality that a car with an accident history is worth less to a potential buyer. Insurance companies often try to deny these claims outright or offer pennies on the dollar, hoping you’ll just give up. They might question your appraiser’s methods or present their own, much lower valuation. Don’t get flustered. Stick to your evidence and calmly explain why their assessment doesn’t reflect the real-world market. Fighting these lowball offers is exactly what our legal services are designed for.

Filing a diminished value claim in small claims court might seem like a simple, step-by-step process, but it comes with its own set of hurdles. Once you’ve submitted your paperwork, you’re entering the insurance company’s territory, and they have a well-practiced playbook designed to protect their bottom line. They handle thousands of these claims and know exactly which arguments can intimidate or confuse people who are new to the process.

But knowing what to expect is your biggest advantage. Understanding their common tactics and the court’s requirements ahead of time can make all the difference between feeling overwhelmed and feeling in control. Think of this as your pre-game prep. By anticipating these challenges, you can build a much stronger case, stand your ground with confidence, and stay focused on getting the full compensation you’re owed. Let’s walk through the three biggest obstacles you’re likely to face.

Don’t be surprised when the insurance company tries to downplay or dismiss your claim. It’s their job to minimize payouts, so expect some resistance. A common line you’ll hear is that since your car was repaired, it’s now “good as new.” This argument completely ignores the market reality that a vehicle with an accident on its record is simply worth less to a potential buyer. They might deny your claim outright or come back with a lowball offer, hoping you’ll get frustrated and take whatever you can get. This is a standard tactic, not a reflection on your claim’s validity. Standing firm with solid evidence is your best defense against this pushback.

In any legal claim, the person bringing the case—that’s you—has what’s called the “burden of proof.” This just means it’s your job to prove that your car lost value and to show the court exactly how much. A gut feeling that your car is worth less won’t be enough. You need to present concrete evidence to back up your claim. This includes your professional appraisal report, all repair invoices, and documents showing your car’s excellent pre-accident condition. You should also gather sales listings for similar cars without an accident history to create a clear comparison. The more organized documentation you have, the more compelling your argument will be.

Small claims court is an excellent and accessible option for many, but it has its limits—specifically, a cap on the amount of money you can sue for. In Georgia, the maximum amount you can claim in magistrate court (which handles small claims) is $15,000. Before you file, you must make sure your total diminished value claim falls at or below this amount. If your professional appraisal shows a loss greater than $15,000, small claims court isn’t the right venue. You would either have to sue for a lower amount and give up the difference or pursue the claim in a higher court. If you find yourself in this situation, it’s a good idea to contact us to explore your best options.

Walking into a courtroom can feel intimidating, but being well-prepared is the best way to build your confidence. When you present your case, your goal is to clearly and calmly show the judge why you are owed money for your car’s diminished value. This isn’t about high-stakes drama; it’s about presenting a logical argument backed by solid facts. The judge is there to hear both sides, and a well-organized, respectful presentation will make your side much easier to understand and accept. Think of it as telling a straightforward story, with your evidence as the proof.

To win your case, you need to do more than just say your car is worth less; you have to prove it. If you decide to sue, you need strong evidence to show exactly how much money your car lost in value and why you deserve that amount. Gather all your documents and arrange them in a logical order, like in a binder with tabs. This will help you present your points clearly and answer any questions from the judge without fumbling for papers. Your evidence file should include your professional appraisal, repair invoices, and examples of what similar cars (with and without accident histories) are selling for. This documentation is the foundation of your entire diminished value claim.

You don’t need to memorize a speech, but you should practice explaining your case out loud. Run through the key points: what your car was worth before the accident, what happened, how the repairs were handled, and how you calculated the diminished value. Carefully documenting all communications and offers from the insurance company is also crucial. Rehearsing helps you organize your thoughts and ensures you don’t forget any important details when you’re standing in front of the judge. It also helps you stay focused and calm, allowing you to present your case with confidence. If you’re feeling overwhelmed, remember that our team is here to help you prepare.

How you conduct yourself in court matters. Always address the judge as “Your Honor,” stand when you speak, and never interrupt the judge or the other party. It’s important to know that in Georgia, lawyers are allowed in small claims court, so you might be up against a legal representative from the insurance company. Don’t let this intimidate you. Stick to your facts and present your evidence clearly. Being polite and respectful shows the court that you take the process seriously. This simple courtesy can go a long way in making a positive impression and ensuring the focus stays on the facts of your property damage case.

Filing a diminished value claim in small claims court can feel empowering, but it’s easy to make a simple mistake that could cost you the case. Insurance companies handle these claims every day and know what to look for. By being aware of the most common pitfalls, you can build a much stronger case and give yourself the best possible chance of getting the money you deserve. Think of it as learning the rules of the game before you play. A little preparation goes a long way in showing the court—and the insurance company—that you mean business.

The good news is that these mistakes are entirely avoidable. From gathering the right paperwork to understanding your claim’s true worth, a methodical approach is your greatest asset. Let’s walk through the three biggest errors people make so you can steer clear of them.

You can’t win a diminished value claim on feelings alone. You need cold, hard proof. The burden is on you to show the court exactly how much value your car lost, and that requires a solid paper trail. Without it, your claim is just your word against the insurance company’s, and they have teams of people paid to dispute you. To build an undeniable case, you need to gather every piece of relevant information.

Start with your car’s pre-accident condition, using records from sources like Kelley Blue Book. Then, collect all accident-related documents, including the police report and photos of the damage. Finally, the most critical piece is a professional appraisal that clearly states your car’s diminished value. Having thorough documentation makes your claim clear, credible, and much more difficult for the insurer to fight.

After an accident, you have a limited window of time to take legal action. In Georgia, the statute of limitations for property damage is typically four years from the date of the accident. While that might sound like a lot of time, waiting can seriously complicate your case. Evidence can get lost, memories can fade, and the insurance company may argue that the delay hurt their ability to investigate.

It’s best to file your claim as soon as the repairs on your vehicle are complete. Acting quickly shows you’re serious and helps keep the details of the incident fresh. If you’re feeling overwhelmed or are worried about missing a critical deadline, it’s always a good idea to get in touch with a legal professional who can help you stay on track and ensure your paperwork is filed correctly and on time.

One of the biggest mistakes you can make is underestimating what you’re owed. Insurance adjusters are trained to offer the lowest possible settlement, and they’re counting on you not knowing the true diminished value of your car. If you accept their initial lowball offer, you could be leaving hundreds or even thousands of dollars on the table. Don’t fall into the trap of taking the first number they throw at you just to get it over with.

Before you even think about filing, you need a clear, objective calculation of your loss. This is why a professional appraisal is so important. An expert can determine the real post-repair market value of your vehicle, giving you a specific dollar amount to demand. Knowing your number gives you the confidence to reject unfair offers and fight for the full compensation our legal services are designed to help you secure.

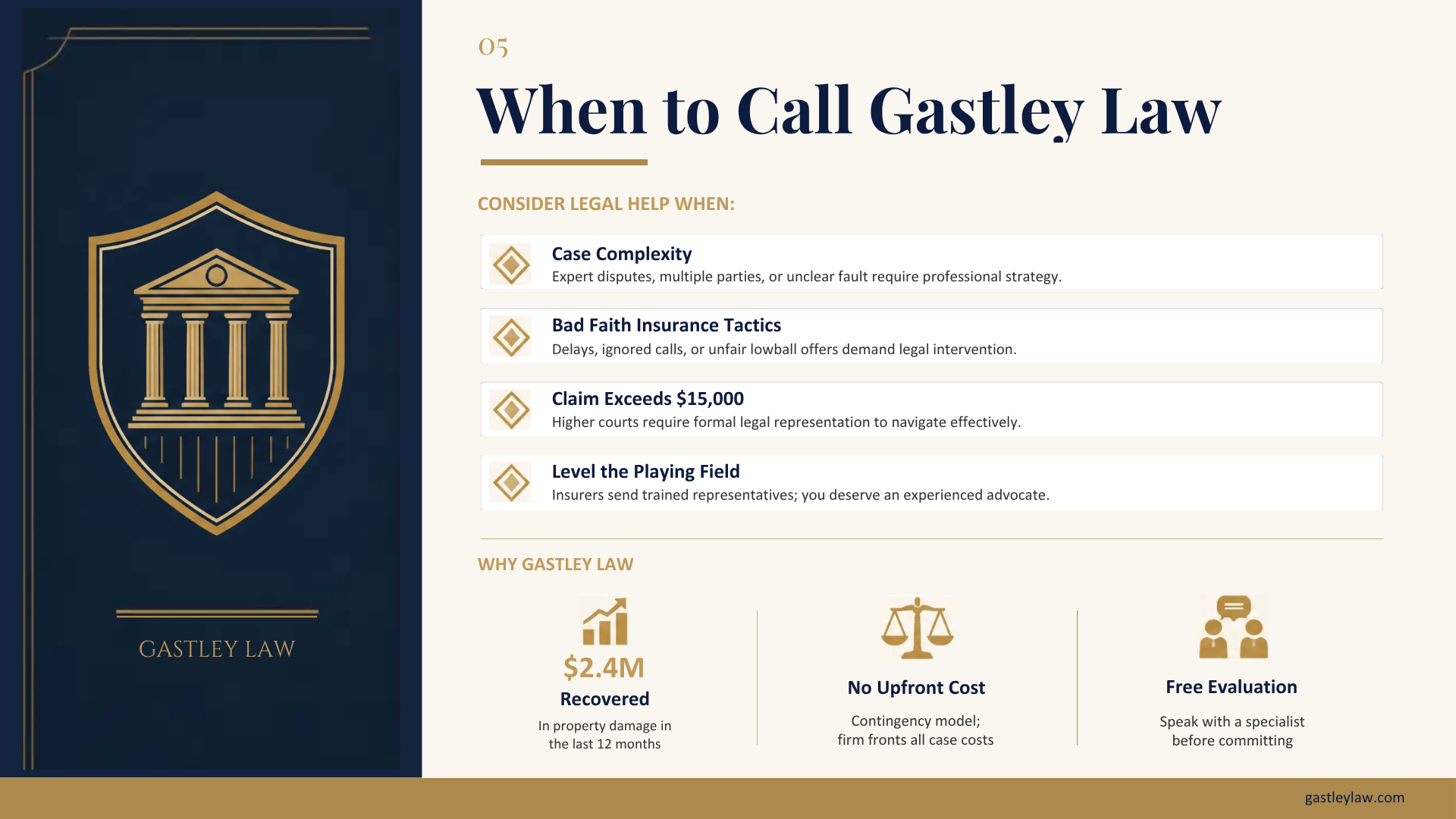

Georgia Magistrate Court is designed to be accessible, but handling a diminished value case without legal representation is not always the best fit. An attorney may be valuable when the proper defendant or venue is disputed, appraisal or repair evidence is challenged, an insurer raises defenses, or the value of the claim is uncertain. The goal is practical preparation, not a promise of a particular result.

A court-ready claim identifies the correct defendant and venue, organizes the appraisal, repair records, vehicle history, and insurer communications, and anticipates the defenses that may arise. When negotiation stalls, a demonstrated willingness to pursue a viable claim in court can give the insurer a reason to reassess its position. Litigation readiness can strengthen the process, but it does not guarantee a recovery or court outcome.

Gastley Law can evaluate whether diminished value legal representation makes sense, help identify the right parties and court, organize evidence, address insurer defenses, and prepare a viable claim for litigation. The firm can also explain the considerations involved in suing for diminished value and how the issues may differ from a small claims court property damage case.

Consider getting legal advice before filing if you are unsure whom to sue, which county is the proper venue, whether your evidence supports the amount claimed, how to respond to insurer defenses, or whether the claim belongs in Magistrate Court. Georgia vehicle owners can contact Gastley Law to discuss whether legal representation makes sense for their circumstances. This article provides general information only and does not guarantee eligibility, recovery, or any particular outcome.

Yes, absolutely. This is the core of most diminished value claims. Even if a top-tier body shop makes your car look brand new, it now has an accident on its vehicle history report. That permanent record makes it less desirable to any informed buyer, which directly lowers its resale value. You are claiming the financial loss caused by that stigma, not the quality of the repairs.

This is a common and frustrating tactic. Insurance companies sometimes hope that by delaying or ignoring you, you’ll simply give up. Your best next step is to send a formal demand letter that clearly states your case and includes a copy of your professional appraisal report. If they still don’t respond or negotiate fairly, filing a lawsuit in small claims court against the at-fault driver is often the move that gets their immediate attention.

Generally, no. In Georgia, diminished value is something you claim from the at-fault party’s insurance. Your own insurance policy is designed to pay for the physical repairs to your vehicle, but it typically does not cover the loss in market value. The right to claim diminished value rests with the person who was not at fault for the accident.

Not at all. Cashing the check for your car’s repairs closes out that specific part of your claim, but it doesn’t automatically waive your right to pursue diminished value. As long as you haven’t signed a final release form that settles all claims from the accident, you can still move forward. Just make sure you are still within Georgia’s four-year statute of limitations.

The number the insurance company provides is an offer, not a statement of fact. It’s almost always calculated using a self-serving formula that results in a low figure. A professional appraisal is an independent, unbiased valuation from an expert who analyzes the actual market, not a rigid formula. This report is your single most powerful piece of evidence to prove what you’re truly owed and to effectively challenge their lowball offer.

If the insurer refuses to take your evidence seriously, a Georgia diminished value attorney can evaluate the claim and help decide whether negotiation or court makes sense.