Hearing that your car is a “total loss” is bad enough, but seeing the lowball settlement offer that follows can feel like a slap in the face. You know what your car was worth—you remember its condition, the new tires you just bought, and how well you maintained it. The number on the screen doesn’t add up. This is the moment where you have to make a choice. So, do you have to accept the insurance offer on your totaled car? Absolutely not. That offer is simply the insurance company’s opening bid. You have the power to challenge their assessment, provide your own evidence, and negotiate for a fair amount. This isn’t about being difficult; it’s about advocating for yourself and ensuring you receive the full compensation you are legally owed.

If your repaired vehicle is worth less after the accident, review your options for a Georgia diminished value claim.

As Georgia’s top-rated law firm specializing in diminished value and other auto insurance claims, we are the experts when it comes to more about negotiating with insurance companies.

After a car accident, the last thing you want is to feel short-changed by the insurance company. So let’s get one thing straight: you do not have to accept the first settlement offer you receive for your totaled car. In fact, you probably shouldn’t. That initial offer is often just a starting point for a negotiation, not the final word on what your vehicle was worth.

It’s helpful to remember that insurance companies are for-profit businesses. Their primary goal is to protect their bottom line, which often means paying out as little as possible on claims. A low initial offer isn’t a personal reflection on you or your car; it’s simply a business tactic. They expect many people to accept it without question because the process can feel intimidating and stressful, especially when you just want to move on.

By politely rejecting the first offer, you are exercising your right to negotiate a fair settlement. This action keeps your claim open and signals to the insurance adjuster that you intend to do your own research. It opens the door for you to present a formal counteroffer, one that’s supported by solid evidence of your car’s true pre-accident value. This is a standard part of the claims process, and you have every right to advocate for the full compensation you deserve. Understanding your consumer rights is the first step toward ensuring you aren’t leaving money on the table.

After a car accident, hearing an insurance adjuster say your car is “totaled” can feel like the final word. But what does it really mean? It’s not just about how wrecked the car looks—it’s a financial calculation. An insurance company declares a car a total loss when the cost to repair it is more than what the car was worth right before the accident.

Think of it this way: the insurer is deciding if it’s cheaper to pay for the repairs or to just write you a check for the car’s value. Because this decision is based on numbers—numbers that can be debated—it’s important to understand how they arrive at their conclusion. Different states have different rules for this, and knowing the specifics for Georgia is your first step in making sure you get a fair deal.

When an insurance company evaluates your vehicle, they’re running a cost-benefit analysis. The main formula they use compares the cost of repairs to the car’s pre-accident value, often called its Actual Cash Value (ACV). Many states set a clear percentage for this. For instance, in some places, if the repair costs exceed 75% or 80% of the car’s value, it’s automatically deemed a total loss. This percentage is known as the Total Loss Threshold. The insurer will get repair estimates from their approved body shops and compare that figure to their valuation of your car to make the call.

Georgia does things a bit differently. Instead of using a fixed percentage, our state uses what’s known as the Total Loss Formula. Under Georgia law, your car is considered a total loss if the cost to repair it plus its salvage value (what it’s worth as scrap) is greater than or equal to its pre-accident value. This gives the insurance company some flexibility, but it also means their math needs to be accurate. If they underestimate your car’s pre-accident worth or overestimate its salvage value, it could lead to an unfair total loss declaration or a lowball settlement offer. Understanding this formula is crucial when you’re dealing with a property damage claim.

When an insurance company tells you your car is a total loss, their next step is to present you with a settlement offer. But where does that number come from? It’s not random. Insurers use a specific process to determine what your car was worth moments before the crash. Understanding this process is your first step toward making sure their offer is fair. They have their own methods and tools, but their valuation is a starting point for a conversation, not the final word. Let’s pull back the curtain on how they come up with their number so you can be prepared to respond.

Insurance companies don’t pay to replace your car with a brand-new one. Instead, they pay what’s called the “Actual Cash Value,” or ACV. Think of ACV as the fair market price for your car right before the accident happened. This value considers depreciation, meaning it accounts for your car’s age, mileage, and general wear and tear. It’s not what you originally paid for the vehicle or what you still owe on your loan. The adjuster’s goal is to find what a willing buyer would have paid for your exact car in its pre-accident condition. This concept is different from diminished value, which applies when your car is repaired but has lost market value.

Most major insurance companies don’t just guess the ACV. They hire third-party companies that specialize in vehicle valuations. One of the most common services you’ll see is CCC Intelligent Solutions (formerly CCC ONE). This company generates a detailed report—often 20 pages or more—that compares your car to similar vehicles recently sold in your area. The report breaks down how they adjusted the value based on your car’s specific features, mileage, and condition. You have the right to ask for a full copy of this report, and you absolutely should. It’s the key to understanding exactly how they landed on their offer. If the report seems confusing, you can always contact us to review it with you.

An insurer’s valuation report will look at several factors to determine your car’s ACV. They’ll consider the make, model, age, and mileage, as well as its overall condition. They might even make “condition adjustments,” deducting money for things like old tires, stained upholstery, or previous, unrepaired damage. Unfortunately, special custom parts like a high-end sound system or custom wheels might not be included unless you had special coverage. It’s important to remember that insurance companies often try to devalue claims to save money. If their assessment seems low, our team can help you challenge it by providing a more accurate picture of your car’s true worth through our property damage claim services.

After a car accident, getting a settlement offer can feel like a relief—until you see the number. If your gut tells you the insurance company’s offer is too low, you’re probably right. The good news is that their first offer is rarely their final offer. You absolutely have the right to question their valuation and negotiate for a fair amount that truly reflects what your car was worth.

Think of their initial offer as the starting point of a conversation, not the end of it. Insurance companies are businesses, and their goal is to resolve claims for the lowest amount possible. They expect you to push back, but many people don’t know they can. By understanding your rights and their tactics, you can enter the negotiation process with confidence and a clear strategy.

Let’s get one thing straight: you are never obligated to accept the first settlement offer for your totaled car. It’s crucial to remember that an insurance adjuster’s initial figure is just that—an offer. Insurance companies often start with a low number, hoping you’ll accept it quickly without asking questions. This is a standard industry practice.

You have the legal right to reject an offer that you believe is unfair and present a counter-offer. The entire process is a negotiation, and you are an active participant. Don’t let the adjuster make you feel rushed or pressured. Taking the time to review their valuation, gather your own evidence, and advocate for yourself is a protected part of the claims process. This is where having an expert handle your property damage claim can make all the difference.

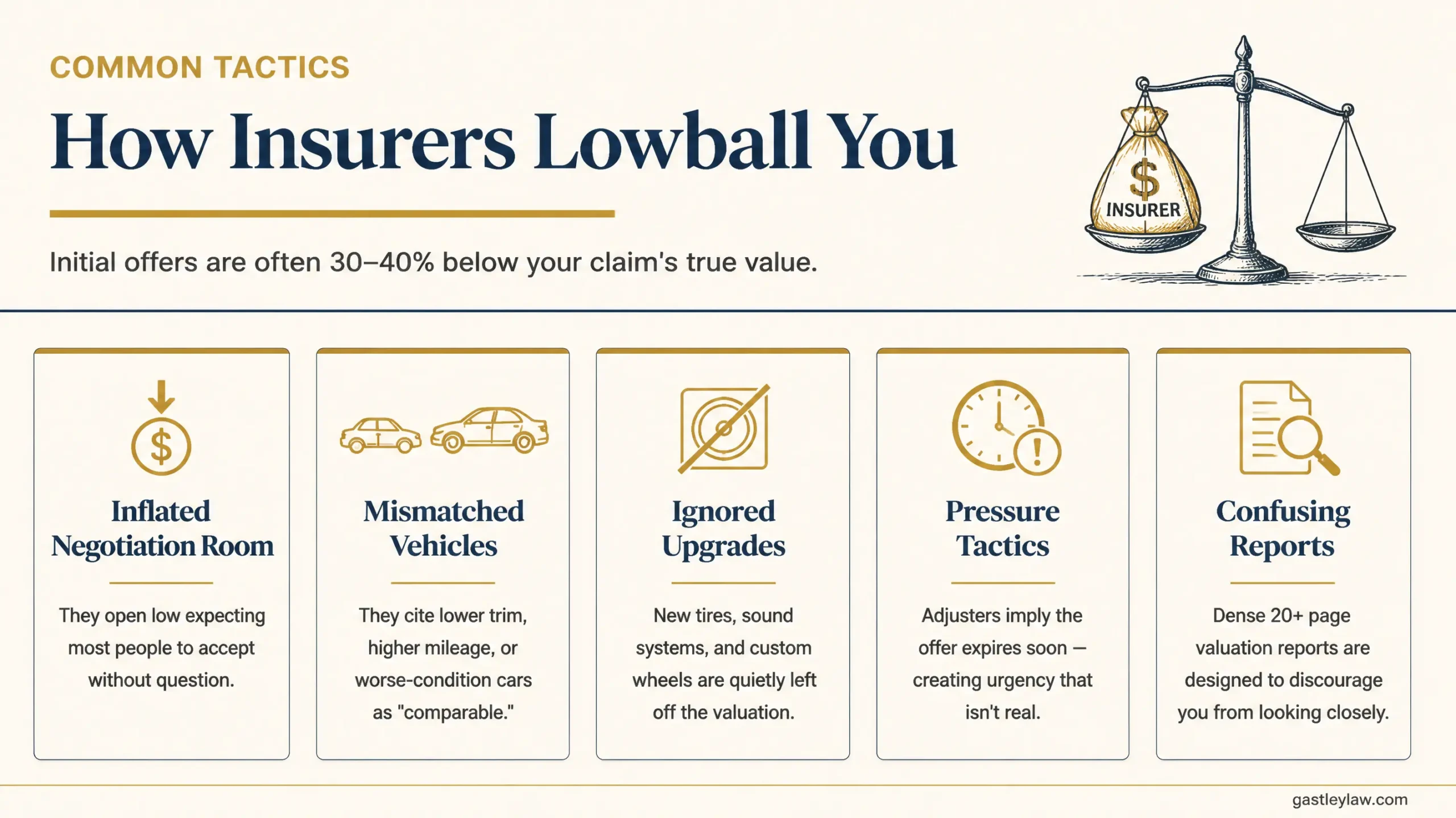

Insurance companies use specific strategies to minimize what they pay out. One of the most common is simply presenting an initial offer that is significantly less than your claim’s actual value—sometimes 30% to 40% lower. They do this intentionally to create “negotiation room,” fully expecting that you might negotiate for a higher amount. If you accept the first offer, they save a substantial amount of money.

Another tactic is using valuation reports that rely on inappropriate “comparable” vehicles that may be a lower trim level, have higher mileage, or are in poorer condition than your car was before the accident. They might also undervalue recent upgrades you’ve made, like new tires or a stereo system. Understanding these tactics is the first step in building a strong case to challenge their assessment.

When an insurance company gives you a low settlement offer, it can feel like a final verdict. But it’s not—it’s the start of a negotiation. The best way to enter that negotiation is with a folder full of proof that your car was worth more than they claim. Think of it like building a case for your car’s true value. The more organized and detailed your evidence is, the harder it will be for the adjuster to dismiss your counter-offer. Taking the time to gather these documents shows you’re serious and prepared to fight for what you’re owed. This preparation is crucial whether you’re handling the negotiation yourself or preparing to work with a legal expert on your property damage claim. It puts you in the driver’s seat and turns the conversation from what they think your car is worth to what you can prove it’s worth.

If you and the insurance company are far apart on the numbers, or if you simply feel their assessment is unfair, don’t be afraid to get a second opinion. You can hire an independent, neutral appraiser to evaluate your vehicle’s pre-accident value. This expert assessment provides powerful leverage in your negotiations because it comes from an unbiased third party. Presenting an independent appraisal to the adjuster shows that you’ve done your homework and have a professional valuation to back up your claim. It’s a clear signal that you won’t accept an offer that doesn’t reflect your car’s actual worth.

One of the most effective ways to counter a low offer is to show the adjuster what similar cars are actually selling for in your local market. You need to prove your car is worth more than their database says it is. Start by researching recent sales of vehicles that match your car’s make, model, year, mileage, and overall condition. Look at listings from local dealerships, private sellers on sites like Autotrader or Facebook Marketplace, and even classified ads. Save screenshots and printouts of these “comps” to create a portfolio of evidence. This real-world market data is much more compelling than the generic figures an insurer might use.

Was your car in pristine condition before the accident? You need to prove it. The insurance company’s valuation often assumes average wear and tear, so it’s up to you to show them otherwise. Go through your phone and find photos of your car from before the crash, especially any that highlight its clean interior, scratch-free paint, or special features. If you don’t have photos, see if friends or family members do. This visual evidence helps paint a clear picture of a well-maintained vehicle, justifying a higher value than the standard depreciation models might suggest.

If you recently invested in your car, you deserve to have that value reflected in your settlement. Dig up all your receipts and service records for any significant work done on the vehicle. This includes major repairs, new tires, a new battery, engine work, or any custom upgrades like a new sound system or rims. Providing the adjuster with a detailed maintenance history and proof of recent upgrades demonstrates that your car was in excellent working order and had a higher value than a similar vehicle without that investment. Every receipt you can provide adds another piece of concrete evidence to your case.

Getting a lowball offer from an insurance company can feel defeating, but it’s rarely the final word. Think of it as the start of a conversation. With the right preparation and a clear strategy, you can effectively challenge their initial number and work toward a settlement that truly reflects what your car was worth. The key is to stay organized, communicate clearly, and back up your claims with solid evidence. Let’s walk through the steps to take control of the negotiation process.

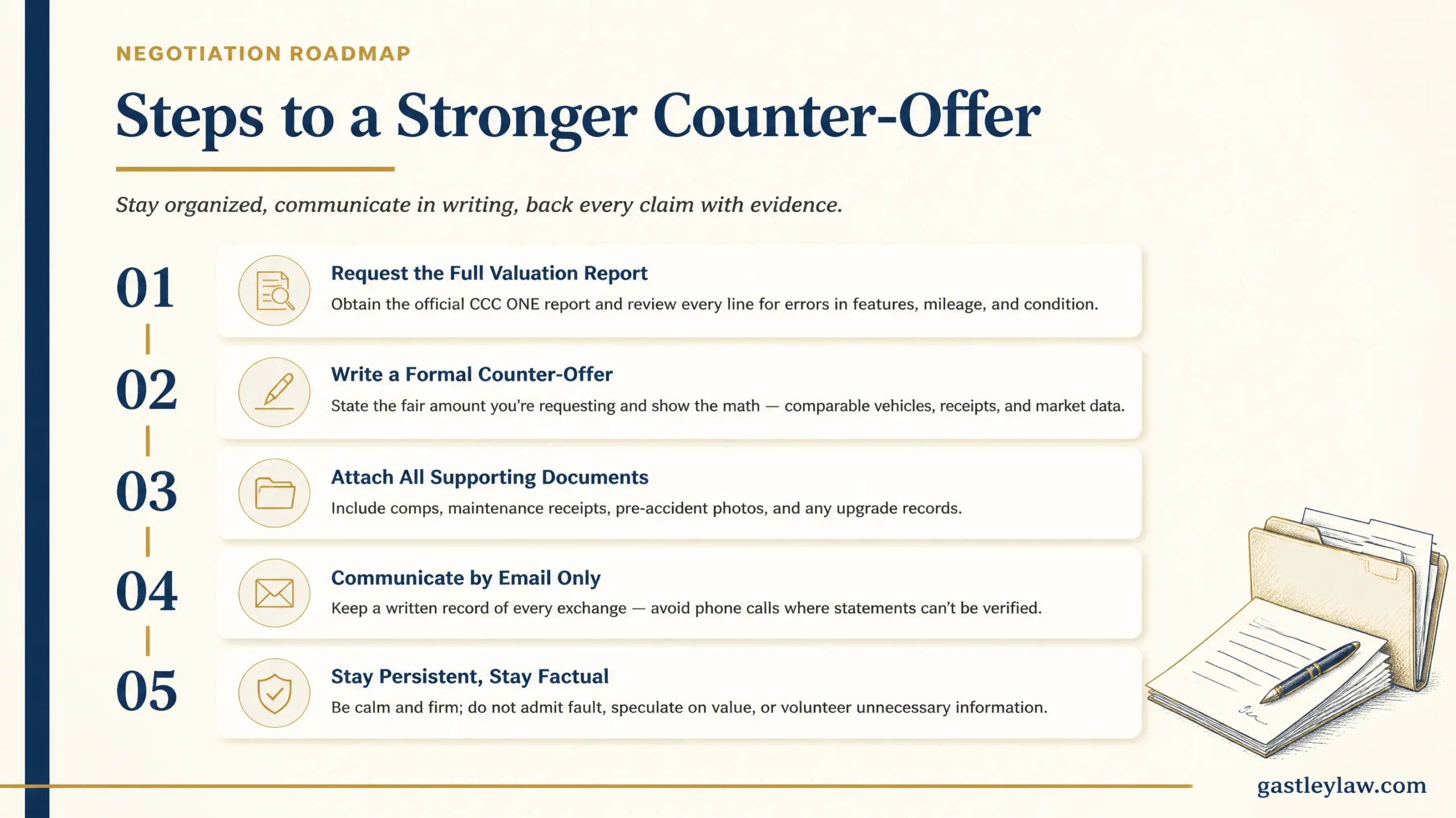

Before you can argue that an offer is too low, you need to understand exactly how the insurance company arrived at their number. Most major insurers use a third-party service, like CCC ONE, to generate a detailed valuation report. This document, often around 20 pages long, breaks down the specific data they used to calculate your car’s pre-accident value, including comparable vehicles in your area.

If the adjuster hasn’t already sent you this report, your first step is to ask for it. Politely request a complete copy of the valuation. This report is your roadmap; it shows you their methodology and highlights potential areas where they might have made a mistake, like missing key features of your car or using inaccurate comparisons. Understanding their logic is crucial for building your counter-argument and understanding the true diminished value of your vehicle.

Once you have the insurer’s report and have gathered your own evidence (like independent estimates and comparable vehicle listings), it’s time to present a counter-offer. Simply saying you want more money won’t work; you have to prove why your car is worth more.

Draft a formal letter or email to the adjuster. Clearly state the amount you believe is fair and methodically explain how you calculated it. Attach all your supporting documents—your research on similar cars for sale, receipts for recent upgrades, and detailed maintenance records. The goal is to present a logical, evidence-based case that makes it difficult for them to justify their original low offer. By providing comprehensive documentation, you show them you’ve done your homework and are serious about receiving fair compensation. Our firm provides legal representation to handle this entire process for you.

How you communicate with the insurance adjuster can significantly impact your negotiation. While it’s easy to get frustrated, maintaining a calm and professional tone is essential. Remember, the adjuster is just doing their job, but their job is to save their company money.

Keep your conversations focused on the facts of your claim. It’s best to communicate in writing, like email, so you have a record of everything that was said. Be careful with your words and avoid admitting fault or giving any information that could be used against you. Be persistent without being aggressive. If you feel like you’re being ignored or the adjuster is unwilling to negotiate fairly, it might be time to contact a lawyer to take over the conversation for you.

When that settlement offer from the insurance company finally lands in your inbox, it can feel like a huge relief. But before you rush to sign, it’s important to understand that your decision to accept or reject it is a major turning point. This choice determines whether you walk away with a fair settlement or leave money on the table. Let’s break down what each path means for you and your claim.

Think of an insurance settlement as a final agreement. Once you sign the release form and cash the check, the case is officially closed. You are legally agreeing that the amount you received is full and final payment for your vehicle’s damages. This means you can’t go back and ask for more money later, even if you discover the repairs will cost more than expected or realize the initial offer was far below your car’s actual worth. Insurance companies often start with a low offer, hoping you’ll take the quick cash without questioning it. Accepting that first offer closes the door on any future negotiations for that claim.

While you shouldn’t feel pressured to accept an offer immediately, you also can’t wait forever. Insurance offers usually come with an expiration date, so be sure to note when it is. More importantly, Georgia has a legal deadline, known as the statute of limitations, for filing a lawsuit over property damage. Negotiations with the insurance adjuster do not pause this legal clock. Some insurers might even drag out the process, hoping you’ll miss the deadline to take legal action. If you’re feeling overwhelmed by timelines and want to understand your options, it’s a good idea to contact a legal professional to make sure your rights are protected.

Rejecting an offer isn’t a dead end—it’s the start of the negotiation process. By formally rejecting a lowball offer, you are telling the insurance company that you know your claim is worth more and you’re prepared to prove it. This keeps your claim active and preserves your right to fight for a fair amount. Remember, initial offers are often just a starting point and can be significantly less than what you’re truly owed. Rejecting the offer opens the door to present your own evidence, make a counter-offer, and work toward a settlement that actually covers your losses. This is a critical step in getting the compensation you deserve for your property damage claim.

Dealing with an accident is overwhelming enough without a tough negotiation. Insurance adjusters are trained to settle claims for the lowest amount possible—it’s their job. But it’s your right to push back and fight for your vehicle’s full value. The process can feel intimidating, but you can hold your ground by avoiding a few common missteps. Knowing what to watch for puts you in a stronger position to secure a fair settlement and avoid leaving money on the table.

Think of the insurance company’s first offer as a starting point, not the final word. It’s almost always on the low end because insurance is a business. Before accepting, you need to do your own homework. Research what cars just like yours—same make, model, year, and condition—are selling for in your area. Look at online listings and dealership prices to get a clear picture of your car’s true market value. Remember, you have the right to negotiate with the insurance company if your car is a total loss. Don’t let them dictate the value without verifying it yourself.

An insurance company can’t just pull a number out of thin air. They must pay the “Actual Cash Value” (ACV) of your car, which is what it was worth moments before the accident. They use detailed valuation reports from third-party companies like CCC ONE to do this. These reports can be confusing, but they contain all the data behind the offer. Always ask for a copy of this report. Go through it line by line to understand the basis for their offer and check for any inaccuracies about your car’s features, mileage, or condition.

You might feel a sense of urgency from the adjuster to accept an offer quickly. They may call frequently or imply the offer is time-sensitive. This is a common tactic designed to make you settle for less. You don’t have to accept their first offer, and saying “no” doesn’t end your claim. In fact, rejecting a lowball offer is what begins a negotiation process to get you a better payment. Take the time you need to review the offer, gather your evidence, and prepare a counter-offer. Don’t let anyone rush you into a decision you might regret.

Negotiating with an insurance adjuster can feel like an uphill battle. You’ve gathered your evidence and made your case, but what happens when they refuse to offer a fair settlement? While you have the right to handle the negotiation yourself, there are times when bringing in a professional is the smartest move you can make. An experienced attorney can level the playing field, taking the pressure off you and showing the insurance company you mean business. They can also spot hidden issues in the settlement offer that you might miss, like incorrect calculations or overlooked vehicle features.

Think of it this way: insurance companies handle thousands of claims a day. They have teams of adjusters and lawyers whose main goal is to protect the company’s bottom line by paying out as little as possible. When you’re up against that kind of experience, having an expert in your corner can make all the difference. A lawyer who specializes in property damage and diminished value claims understands the tactics insurers use and knows how to counter them effectively. They can manage the complex communication, legal deadlines, and evidence gathering required to build a powerful case for the true value of your vehicle.

You don’t have to accept the first offer an insurance company gives you, especially if it feels unfairly low. But knowing when to stop negotiating on your own and call for backup is key. Before you reject any settlement, it’s wise to speak with an attorney who can assess if the offer is reasonable.

It’s probably time to get in touch with a lawyer if:

Insurance companies often start with offers that are 30-40% less than what your claim is actually worth. Rejecting a lowball offer shows them you’re serious about getting fair compensation, and having an attorney reinforces that message. At Gastley Law, we take over the fight for you. We know how to properly value claims, interpret Georgia law, and negotiate from a position of strength.

Our team digs into the details of your case, building an evidence-based argument that insurers can’t ignore. We handle all communication with the adjuster, present a detailed counter-offer, and are fully prepared to take legal action if the company refuses to be fair. Our entire focus is on our services that ensure you receive the full amount you’re owed, taking the stress and guesswork out of the process for you.

After a car accident, the path to getting fair compensation can feel overwhelming, especially when you’re up against a big insurance company. But remember, you have more control than you think. The initial offer you receive is just that—an offer, not a final decision. It’s the start of a conversation. By understanding your rights and preparing your case, you can confidently push for the settlement you truly deserve. The key is to be patient, persistent, and prepared to stand up for the full value of your vehicle. Taking a strategic approach from this point forward can make a significant difference in the final payout you receive.

It’s crucial to understand that you do not have to accept the first offer an insurance company makes. In fact, you probably shouldn’t. Insurers are businesses, and their initial offers are often calculated to protect their bottom line, not to give you the maximum amount you’re owed. Think of it as their opening bid in a negotiation. By rejecting a lowball offer, you aren’t closing the door on your claim; you are simply signaling that you’re ready to negotiate for a better outcome. This keeps your claim active and preserves your legal right to pursue the full diminished value of your car.

Before you accept or reject any offer, take a step back. Insurance companies sometimes present their first offer as a final, take-it-or-leave-it deal to pressure you into a quick decision. Don’t fall for it. Research shows that initial settlement offers can be 30-40% lower than the actual value of a claim. The best way to make a final decision with confidence is to have an expert on your side. Speaking with an attorney before you respond to the insurer can give you a clear understanding of your claim’s true worth and a strategy for how to get it. A legal professional can review the details and help you determine if the offer is fair or if you should contact us to fight for more.

This is a tough situation, and unfortunately, it’s quite common. The insurance company is only responsible for paying your car’s Actual Cash Value (ACV), not the balance of your loan. If their offer is fair but still leaves you with a loan balance, you may need to cover the difference yourself unless you have GAP insurance. However, if their offer is unfairly low, negotiating for the true value of your car becomes even more critical to minimize or eliminate that gap.

Insurance adjusters might make it seem like you need to decide immediately, but you should take the time you need to do your research. While offers can have expiration dates, the more important deadline is Georgia’s statute of limitations for filing a lawsuit for property damage. The negotiation process doesn’t stop that clock, so it’s important to be mindful of the legal timeline while you work toward a fair settlement.

It’s a common worry, but you shouldn’t let it stop you from pursuing the full value of your claim. Insurance companies set rates based on risk factors, and an accident can certainly impact them. However, negotiating the payout for a single total loss claim is not typically a factor that would cause a rate increase on its own. You are simply holding the insurer to their end of the bargain to pay what your car was actually worth.

If you’ve presented a strong, evidence-based counter-offer and the adjuster still won’t offer a fair amount, you’ve reached a stalemate. At this point, they may be hoping you’ll just give up. This is often the best time to get a legal professional involved. An attorney can re-engage the negotiation with more authority and show the insurance company that you are prepared to take further action if they continue to negotiate in bad faith.

You absolutely have the right to negotiate on your own, and many people do so successfully. However, if the insurance company’s offer is significantly low, if they are using confusing tactics, or if you simply feel overwhelmed by the process, bringing in a lawyer can be a game-changer. An attorney levels the playing field and manages the entire process, taking the stress off your shoulders and fighting to get you the best possible outcome.