That low settlement offer in your inbox isn’t a mistake; it’s a strategy. Insurance adjusters know you’re dealing with the stress of an accident and just want to move on. They make a quick, low offer hoping you’ll take the money and close the case before you realize what your claim is truly worth. They often ignore major costs like your car’s diminished value—the permanent loss in resale value after an accident. But you don’t have to accept their first number. Understanding how to dispute a car insurance claim settlement is the key to turning the tables. This article will give you the practical, step-by-step process for building a strong case and demanding the full compensation you are legally owed.

After a car accident, getting a settlement offer can feel like a relief—until you see the number. If it seems surprisingly low, you’re not wrong to be suspicious. Insurance companies are for-profit businesses, and their primary goal is to protect their bottom line. This means paying out as little as possible on claims. A low offer isn’t a personal attack; it’s just their standard opening move in a negotiation you might not have realized you were in.

They are banking on the fact that you’re likely stressed, unfamiliar with the claims process, and eager to put the accident behind you. They assume you’ll see their offer as a final decision and take it without asking questions. But that initial number is rarely the best they can do. It’s a starting point designed to save them money. Understanding why they start low is the first step toward pushing back and demanding the full amount you’re owed. With the right information and a clear strategy, you can challenge their initial assessment and work toward a number that truly covers all your losses, including your vehicle’s diminished value. Don’t let their business model prevent you from getting the fair compensation you deserve.

Insurance adjusters often use specific tactics to encourage a quick, low-cost settlement. One of the most common is the fast initial offer. They might contact you right after the accident with a check, hoping you’ll accept it before you’ve had a chance to get multiple repair estimates or fully understand the long-term impact on your car’s value. This quick closure tactic preys on your desire to resolve the situation quickly. They know that the longer you have to research and gather evidence, the more likely you are to realize their offer is inadequate. Don’t let their sense of urgency pressure you into making a decision that isn’t in your best interest.

You pay your premiums faithfully, assuming your policy will have your back when you need it. However, the insurance company’s interpretation of your policy can be very different from your own. Adjusters are trained to find reasons to limit the payout, often pointing to specific clauses or exclusions in the fine print. They may argue that certain repairs aren’t covered or that they will only pay for cheaper, aftermarket parts instead of original manufacturer equipment. This is where having specialized legal representation can make a significant difference, as an expert can interpret your policy correctly and hold the insurer accountable for what they promised to cover.

An unfair settlement offer is one that doesn’t make you whole again. The most obvious sign is an amount that won’t even cover your repair bills from a reputable body shop. But it goes deeper than that. A lowball offer often completely ignores your car’s diminished value—the loss in resale value your vehicle suffers simply because it now has an accident history. The offer might also fail to account for other costs, like a rental car while yours is in the shop. If the adjuster dismisses your estimates, pressures you to decide immediately, or provides no clear explanation for their math, you’re likely looking at an unfair offer.

When an insurance company gives you a lowball offer, your best defense is a strong offense—and that starts with solid paperwork. Think of yourself as a detective building a case where every photo, receipt, and report is a crucial piece of evidence. This documentation is what proves the true value of your claim and counters the insurer’s attempt to pay as little as possible. Getting organized from the very beginning sends a clear message: you’re serious and prepared to stand up for what you’re owed. A messy, incomplete file can lead to frustrating delays and a lower settlement, while a well-documented claim is much harder for them to dismiss or undervalue. It’s the foundation upon which you’ll build your entire dispute. Let’s walk through exactly what you need to collect to build an undeniable case and fight for the compensation you deserve.

Your phone is one of the most powerful tools you have after an accident. Use it to take clear, detailed photos and videos from every possible angle. Capture the damage to all vehicles involved, their positions on the road, any skid marks, and even the surrounding area, like traffic signs or weather conditions. This visual proof is incredibly difficult for an insurance adjuster to dispute. Don’t forget to also get a copy of the official police report, as it provides an objective account of the incident. If there were any witnesses, be sure to get their names and contact information. This collection of evidence helps create a full picture of what happened and supports your version of events.

Don’t automatically accept the insurance company’s initial damage estimate or their recommendation for a repair shop. They often work with shops that prioritize low costs, not necessarily quality. Instead, take your car to a trusted, independent mechanic or body shop for a thorough inspection. It’s a good idea to get at least two different estimates to establish a fair and accurate cost for repairs. Keep every single receipt and invoice related to your vehicle, including towing fees, rental car expenses, and the final repair bill. These documents are concrete proof of your out-of-pocket costs and are essential for getting fully reimbursed.

If you were injured in the accident, documenting your medical journey is just as important as documenting the vehicle damage. Keep a detailed file of every doctor’s visit, physical therapy session, prescription, and medical bill. Insurance companies often try to downplay injuries to reduce the payout for things like pain and suffering. Your medical records provide a clear timeline of your injuries and the treatment required, making it much harder for them to undervalue your claim. This documentation is critical for ensuring you receive fair compensation for both your physical and financial recovery.

Sometimes, the insurance company’s assessment just doesn’t line up with reality, especially when it comes to your car’s loss of value. Even after perfect repairs, a car with an accident history is worth less than one without. This is called diminished value, and you are entitled to be compensated for it. To prove your case, you’ll need an independent appraisal from a certified expert who can determine the exact amount of diminished value your vehicle has suffered. This unbiased report from a third-party professional carries significant weight and provides the leverage you need to demand a fair settlement.

Now that you have all this evidence, it’s time to get organized. Keep everything in a single, dedicated folder—either physical or digital. Create a communication log where you note the date, time, and details of every conversation you have with the insurance company, including the name of the person you spoke with. Save all emails and letters in one place. Having all your documents neatly organized makes it easy to find what you need when you need it. This simple step not only reduces your stress but also shows the adjuster you are methodical and prepared. If putting this all together feels overwhelming, that’s a sign it might be time to get some help.

Once you have all your documents in order, it’s time to build the argument for why you deserve a better settlement. This isn’t about being confrontational; it’s about being prepared. A strong, evidence-based case shows the insurance company that you’ve done your homework and you won’t be pushed into accepting an unfair offer. It shifts the power dynamic and puts you in a much better position to negotiate. Think of it as creating a clear, logical story of your accident and its true financial impact.

The insurance company’s initial offer is often based on their own calculation of your damages, which might not tell the whole story. To counter their number, you need to have your own. Start by adding up all the obvious costs, like repair estimates and medical bills. But don’t stop there. Your car’s value has likely dropped simply because it’s been in an accident, even after perfect repairs. This is called diminished value, and it’s a real loss you can claim. Insurance companies often undervalue or completely ignore these less tangible damages, so calculating them yourself is a critical step in proving your claim is worth more than their initial offer.

Here’s something you need to remember: you do not have to accept the insurance company’s first offer. You have the right to question it, dispute it, and negotiate for a better one. As a policyholder, you’ve paid your premiums, and you’re entitled to the full coverage you paid for. Understanding this simple fact is incredibly empowering. It changes your mindset from passively accepting what you’re given to actively participating in the outcome. Don’t let an adjuster pressure you into a quick decision. You are allowed to take your time, review the offer, and push back if it feels unfair.

Your insurance policy is a contract between you and the insurance company. It’s worth taking the time to read it carefully to understand exactly what it covers and for how much. The details in your policy can be your best tool for disputing a low settlement. Look for the sections on property damage, collision coverage, and any specific clauses related to repairs or vehicle valuation. If the adjuster’s offer contradicts what’s written in your policy, you have a solid foundation for your dispute. Highlighting these specific sections in your communication shows them you know your stuff.

The insurance adjuster works for the insurance company, so their damage assessment might not be entirely objective. To get a truly unbiased view, get an independent assessment of the damage to your vehicle. Take your car to a trusted mechanic or, even better, hire a licensed public appraiser who specializes in post-accident vehicle valuations. Their expert report serves as powerful, third-party evidence to support your claim. Sharing their findings with the adjuster demonstrates that your requested settlement amount isn’t just a number you came up with—it’s based on a professional evaluation of your actual losses. Our team can help you find the right experts to evaluate your property damage claims.

Communicating with an insurance company can feel like a battle of wills, but you don’t have to be a professional negotiator to get what you deserve. The key is to be prepared, professional, and persistent. Your goal is to clearly state your case, back it up with the evidence you’ve gathered, and create a detailed record of every interaction. This approach shows the insurer that you’re serious about your claim and won’t be pushed into accepting an unfair offer. By handling these conversations with confidence and a clear strategy, you can protect your rights and work toward a fair resolution.

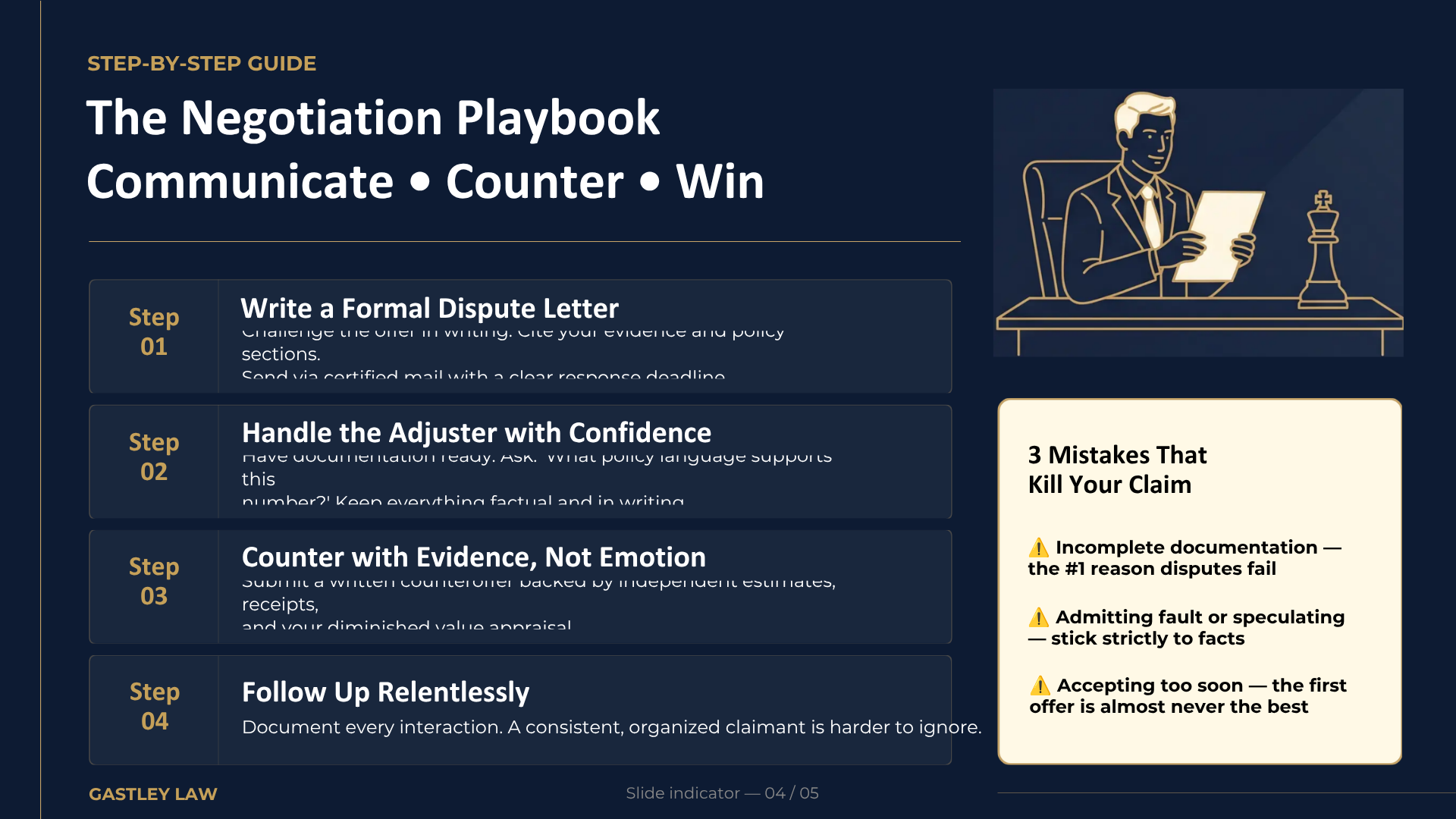

If you’ve received a low settlement offer, your first move should be to put your disagreement in writing. A formal dispute letter officially notifies the insurance company that you are challenging their offer. In the letter, clearly state why you believe the settlement is inadequate, referencing specific evidence like repair estimates and your independent appraisal. It’s also helpful to point to the relevant sections of your policy. Keep your tone polite and professional, and give them a specific deadline to respond, such as 10 business days. Send this letter via certified mail to have a record of its delivery, and consider sending a copy to the adjuster’s supervisor.

When you speak with the claims adjuster on the phone, confidence is your best asset. Before you call, have all your documentation in front of you so you can refer to facts and figures easily. Don’t be afraid to ask direct questions. A great starting point is, “Can you please show me the exact language in my policy that justifies this low offer?” This puts the burden on them to explain their reasoning based on the contract you both share. Stick to the facts of your case, especially the diminished value of your vehicle after the accident. Avoid emotional arguments and never speculate or admit any fault.

Persistence is crucial when dealing with insurance companies. If you don’t hear back by the deadline you set in your letter, follow up with a phone call and another email. If the adjuster is unresponsive or refuses to reconsider their offer, you have other options. You can file a formal complaint with the Georgia Office of Commissioner of Insurance and Safety Fire. This step often gets the insurance company’s attention. It’s also at this stage that many people realize they need professional support. An experienced attorney can take over communications and apply legal pressure, which is often what it takes to get a fair offer.

From your very first call, keep a detailed log of every interaction with the insurance company. After each phone call, jot down the date, time, the name of the person you spoke with, and a summary of the conversation. Better yet, send a brief follow-up email to the adjuster confirming what was discussed. For example: “Hi [Adjuster’s Name], just to confirm our conversation today, you stated that…” This creates a written record that is difficult to dispute later. Save every email and piece of mail you receive in your evidence file. This meticulous record-keeping is one of the most powerful tools you have in a property damage claim.

Once you’ve built your case and sent your dispute letter, the negotiation process begins. This can feel like the most intimidating part, but it’s really just a conversation. Remember, the insurance company’s first offer is just that—an offer. It’s a starting point for a discussion, not a final decision. You have every right to reject an offer that doesn’t fairly cover your losses.

The key to a successful negotiation is preparation. You’ve already done the hard work by gathering your evidence and calculating your damages. Now, it’s about communicating that information clearly and confidently. Stay calm, stick to the facts, and don’t be afraid to advocate for what you’re owed. This is a business transaction, and your goal is to ensure the final settlement makes you whole again.

You don’t have to accept an insurance claim settlement if you think it’s too low. When the claims adjuster calls with an initial offer, your best response is to listen calmly and take notes. You don’t need to give them an immediate answer. Instead, thank them for the offer and tell them you need time to review it against your own records.

When you respond, refer back to your evidence. Clearly explain why their offer is insufficient, pointing to specific repair estimates or your diminished value report. The goal is to show them, with facts and figures, that your counteroffer is based on real-world costs, not just what you feel you deserve. Staying professional and fact-based keeps the conversation productive.

After you reject the first offer, the adjuster will likely come back with a second one. This is a standard part of the process. Ask them to explain how they arrived at their new number and request that they send the revised offer to you in writing. This creates a clear paper trail and gives you time to evaluate it without pressure.

If the new offer is still below your calculated damages, you can reject it again. Reiterate your main points and refer back to your documentation. Each exchange is an opportunity to strengthen your position and show the insurer you’re serious about receiving fair compensation for your property damage claim.

Before you get too deep into the back-and-forth, you need to determine the absolute minimum amount you are willing to accept. This isn’t a random number; it should be based on the total damages you calculated earlier, including repairs, rental costs, and diminished value. This is your walk-away number.

Insurance companies often start with low settlement offers because their goal is to save money. Having a firm bottom line prevents you from being worn down by their tactics. It acts as your anchor, keeping you focused on what you truly need to cover your losses. If you’re struggling to figure out what a fair number is, you can always reach out for a professional evaluation.

So, what does a “fair” settlement actually cover? It’s an amount that makes you financially whole again, as if the accident never happened. This includes the full cost of quality repairs, reimbursement for a rental car, and compensation for your vehicle’s loss in resale value. This last part, known as diminished value, is a critical piece of the puzzle that insurers often leave out of their initial offers.

Be cautious of quick settlement offers. Some adjusters make a low offer right away, hoping you’ll take the fast cash before you understand the full extent of your damages. A fair settlement isn’t rushed; it’s calculated based on thorough documentation and a complete assessment of all your losses.

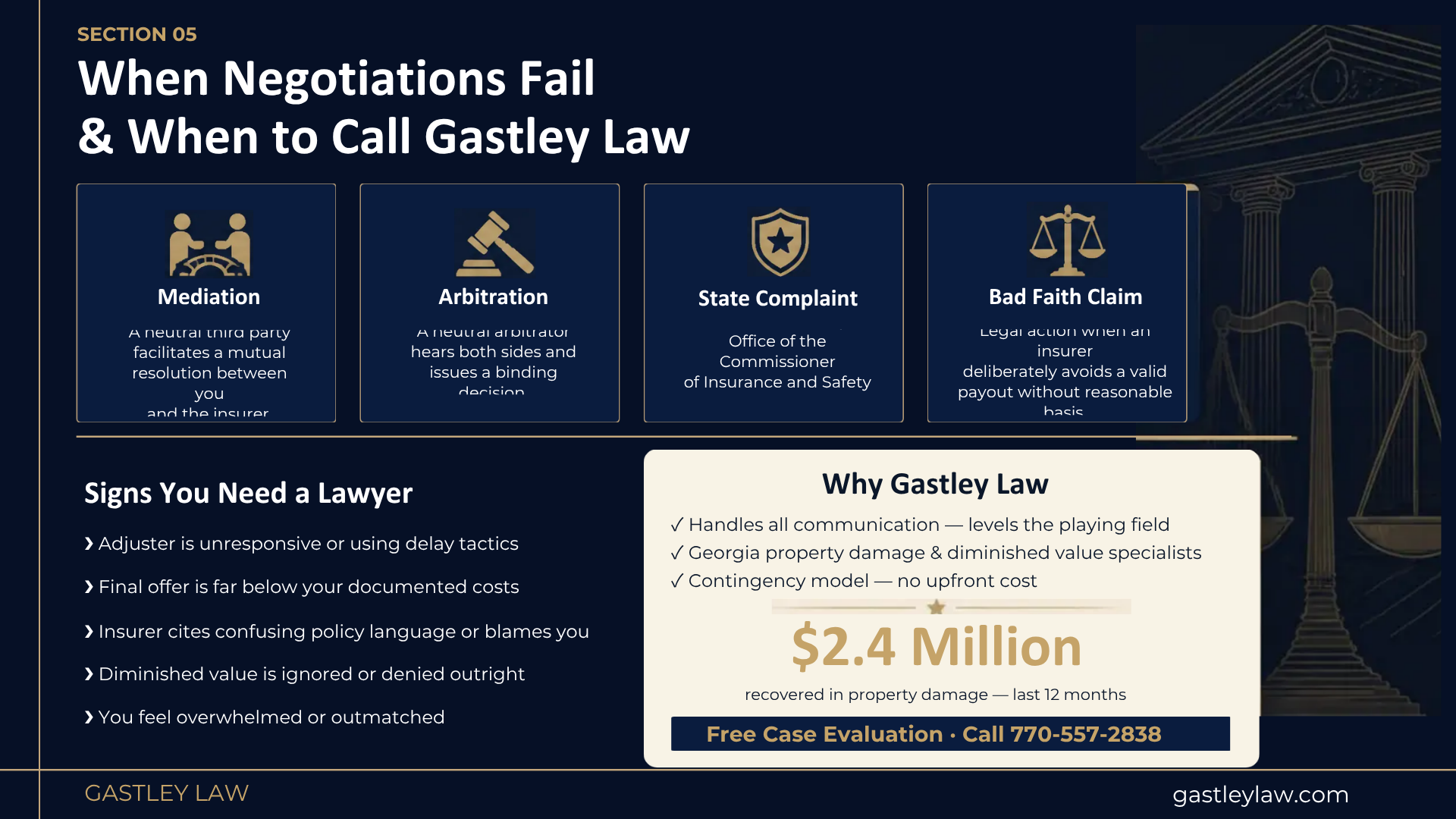

It’s incredibly frustrating when you’ve done everything right, but the insurance company still won’t offer a fair settlement. When you feel like you’ve hit a wall, don’t give up. You still have several powerful options to move your claim forward and get the compensation you deserve. Think of this as a new phase in the process. The back-and-forth is over, and now it’s time to bring in outside help to resolve the dispute. Depending on your situation, you can consider bringing in a neutral third party through mediation or arbitration, filing a formal complaint with state regulators who oversee the insurance industry, or, in more serious cases, pursuing a bad faith claim against the insurer. Each path has its own process and potential outcomes, so let’s walk through what each one involves.

If direct negotiations aren’t working, mediation can be a great next step. Think of it as a structured conversation with a neutral third party, called a mediator, who helps you and the insurance company find common ground. The mediator doesn’t take sides or make decisions for you; their job is simply to guide the discussion toward a resolution that both parties can agree on. It’s a voluntary process, so the insurer has to agree to participate, but it’s often favored because it’s less formal, less expensive, and much faster than going to court. The Georgia Office of Insurance offers a mediation program specifically to help consumers resolve these kinds of disputes.

Arbitration is another way to resolve a dispute outside of the courtroom, but it’s a bit more formal than mediation. In arbitration, you and the insurance company present your cases to a neutral arbitrator (or a panel of them), who acts like a private judge. After hearing both sides, the arbitrator makes a decision. Depending on the terms you agree to beforehand, this decision can be legally binding, meaning you both have to accept it. While it’s more structured than mediation, arbitration is still typically faster and more cost-effective than filing a lawsuit, making it a practical option when you’ve reached a complete standstill in negotiations.

Insurance companies are regulated by the state, and they have a legal duty to handle claims fairly and promptly. If you believe your insurer is not meeting its obligations, you can file a complaint with Georgia’s Office of the Commissioner of Insurance and Safety Fire. This government body is responsible for making sure insurance companies follow the law. Filing a complaint brings official oversight to your case. The department will review your claim and the insurer’s conduct to determine if they have acted improperly. This can put significant pressure on the company to reconsider its position and make a fair offer.

An insurance policy is a contract. You pay your premiums, and in return, the company agrees to cover your losses. If an insurer fails to honor its end of the deal without a reasonable basis—for example, by intentionally offering a ridiculously low settlement, refusing to investigate your claim properly, or creating unreasonable delays—they may be acting in “bad faith.” A bad faith claim is a serious legal action that holds the insurance company accountable for its misconduct. Proving bad faith can be complex, so this is the point where having an experienced attorney is crucial. If you suspect an insurer is deliberately trying to avoid paying what they owe, we can help you evaluate your case.

You’ve done everything right—you gathered your evidence, wrote a solid dispute letter, and tried to negotiate in good faith. But what happens when the insurance company still won’t offer a fair settlement? Sometimes, no matter how organized or persistent you are, the adjuster won’t budge. This is when bringing in a legal professional can make all the difference.

Hiring a lawyer isn’t about giving up; it’s about leveling the playing field. Insurance companies have teams of lawyers working for them, and you deserve to have an expert in your corner, too. An attorney can cut through the red tape and show the insurer you’re serious about getting the compensation you’re owed.

If your conversations with the insurance adjuster are going in circles, it’s probably time to call for backup. A major sign is when the insurer simply stops responding or uses endless delay tactics. Another red flag is receiving a final offer that is still far below your documented repair costs and diminished value. If the insurance company accuses you of being at fault when you weren’t, or if they start using complex policy language to justify their low offer, don’t feel pressured. These are clear signals that you can no longer resolve the issue on your own and need professional legal help.

Let’s be honest: insurance companies often take lawyers more seriously than they do individuals. An attorney immediately changes the dynamic of the negotiation. They know the tactics adjusters use and won’t be intimidated. A lawyer can build your best case by organizing your evidence, bringing in industry experts, and handling all communication with the insurer so you don’t have to. Most importantly, they have the ability to file a lawsuit if the insurance company refuses to be reasonable. This leverage alone is often enough to bring the insurer back to the table with a much fairer offer.

Every state has a “statute of limitations,” which is a strict deadline for filing a lawsuit. If you miss this window, you could lose your right to pursue a claim in court forever. In Georgia, you generally have four years from the date of the incident to file a lawsuit for property damage. While that might sound like a long time, building a strong case can be a lengthy process. An experienced attorney will manage all these critical deadlines, ensuring your claim is protected while they work to secure your settlement. This lets you focus on getting your life back to normal.

If you’ve exhausted all other options, it may be time to prepare for legal action. Hiring a lawyer is the first and most important step. Once you have legal representation, your attorney will review every detail of your case and advise you on the best path forward. This could mean filing a formal complaint with Georgia’s insurance department or, if necessary, filing a lawsuit. Having an attorney signals to the insurer that you will not accept an unfair outcome. If you feel you’ve hit a wall, don’t wait—contact a legal professional to understand your options.

When you’re trying to get fair compensation, the last thing you want is to accidentally sabotage your own efforts. The claims process is tricky, and insurers often look for reasons to pay out less. By avoiding a few common pitfalls, you can protect your claim and put yourself in a stronger position to get the money you deserve.

Think of your claim as a story you need to prove, and your documents are the evidence. Without solid proof, it’s just your word against the insurer’s. That’s why it’s so important to keep detailed records of everything related to your accident. This includes saving every email, taking notes during phone calls, and keeping all receipts for repairs. A missing police report or a lost estimate can weaken your position. Start a dedicated folder—physical or digital—from day one and put everything in it. This simple habit makes a huge difference when it’s time to prove your case.

When you’re speaking with an insurance adjuster, remember that your words can be used against you. Adjusters are trained to gather information that benefits their company, not you. Be careful what you say, as even a casual comment could hurt your case later. Avoid admitting any fault, even saying something as simple as “I’m sorry.” Don’t speculate about the accident or downplay the damage to your vehicle. Stick to the facts you know for sure. It’s perfectly okay to say, “I don’t have that information right now.” Keeping your conversations brief and factual is your best strategy.

After an accident, it’s tempting to accept the first offer just to get it over with. But you should know that the first offer is rarely the best one. Insurers often start with a lowball figure, hoping you’ll take it without question. It’s often better to say no to an insurance company’s first offer because it may be far less than you deserve. Don’t let them pressure you into a quick decision. Take time to review the offer, compare it to your repair estimates, and make sure it fully covers your losses, including the diminished value of your car.

Your insurance policy is the contract that outlines what is and isn’t covered. If you don’t understand it, you’re negotiating at a disadvantage. Before speaking with an adjuster, take the time to read your insurance policy carefully to know what it covers. Pay close attention to your coverage limits, deductibles, and any specific exclusions. This knowledge empowers you to challenge an adjuster if they try to deny a part of your claim that should be covered. If the legal language feels overwhelming, it’s a good time to contact a professional who can translate it for you. Understanding your rights is the first step to defending them.

It’s almost never a good idea. The first offer is the insurance company’s opening move in a negotiation, and it’s designed to be the lowest amount they think you might accept. They are counting on you being eager to resolve the situation quickly. Taking that first check often means leaving money on the table that you’re entitled to for things like quality repairs and your car’s lost resale value. It’s always best to thank them for the offer, take your time to review it, and compare it against your own documented evidence.

Diminished value is the loss in your car’s market value after it’s been in an accident, even if it has been perfectly repaired. Think of it this way: if you were buying a used car and had two identical options, but one had a clean history and the other had been in a wreck, you would pay less for the one that was in an accident. That difference in price is its diminished value. It’s a real financial loss you’ve suffered, and you have the right to be compensated for it, but insurance companies often conveniently leave it out of their initial offers.

Documentation is everything. While photos and repair bills are crucial, the most powerful tool is often an independent, third-party appraisal. The insurance company’s adjuster works for them, so their assessment serves their interests. Hiring your own expert to evaluate the cost of repairs and, most importantly, calculate your vehicle’s diminished value gives you unbiased proof of your actual losses. This expert report is incredibly difficult for an insurer to argue with and provides the solid foundation you need for a fair negotiation.

When an adjuster starts using delay tactics or pressuring you, shift all your communication to writing. Send a polite but firm email or a certified letter that summarizes your position, references your evidence, and requests a response by a specific date. This creates a paper trail that shows you are being proactive and that they are being unresponsive. If they still won’t engage fairly, it’s a strong signal that you’ve reached the limit of what you can accomplish on your own and it’s time to consider escalating the issue.

You should consider calling a lawyer when the adjuster gives you a “final offer” that is still well below your documented costs, when they start using confusing policy language to deny parts of your claim, or when they simply stop responding to you altogether. If you feel like you’re going in circles and the process is causing you significant stress, that’s your cue. An attorney can take over all communication and apply legal pressure that an individual simply can’t, which often gets the insurance company to take your claim seriously.