How to Negotiate a Higher Total Loss Settlement

You can negotiate a higher total loss settlement when the insurer’s offer does not reflect your vehicle’s actual cash value. Start by requesting the full valuation report, correcting errors in mileage, options, and condition, and supporting your counteroffer with comparable local vehicles. Put the dispute in writing and do not accept the first offer until the insurer explains how it calculated the payout.

- Request the complete valuation report.

- Check mileage, trim, options, condition, and comparable vehicles for errors.

- Gather local comparable listings and maintenance or upgrade records.

- Send a written counteroffer with a specific requested amount.

- Escalate through the policy’s appraisal process or legal help if the insurer will not correct a documented undervaluation.

Key Takeaways

- Build Your Case with Hard Evidence: The insurance company’s valuation is just their opening number. To counter it effectively, gather your own proof, including maintenance records, receipts for upgrades, and examples of comparable vehicles for sale in your area to demonstrate your car’s true worth.

- Control the Conversation with a Clear Strategy: Approach the negotiation with a plan. Determine your minimum acceptable settlement amount beforehand, communicate professionally, and insist on getting all offers and important summaries in writing to create a paper trail and keep you in a position of strength.

- Scrutinize Their Offer and Know When to Escalate: Always read your total loss valuation report and check it carefully for errors in your car’s features, mileage, or condition. If an adjuster is unresponsive or refuses to justify a lowball offer, it’s a clear sign that involving a legal professional is the best way to protect your interests.

What is a Total Loss Claim?

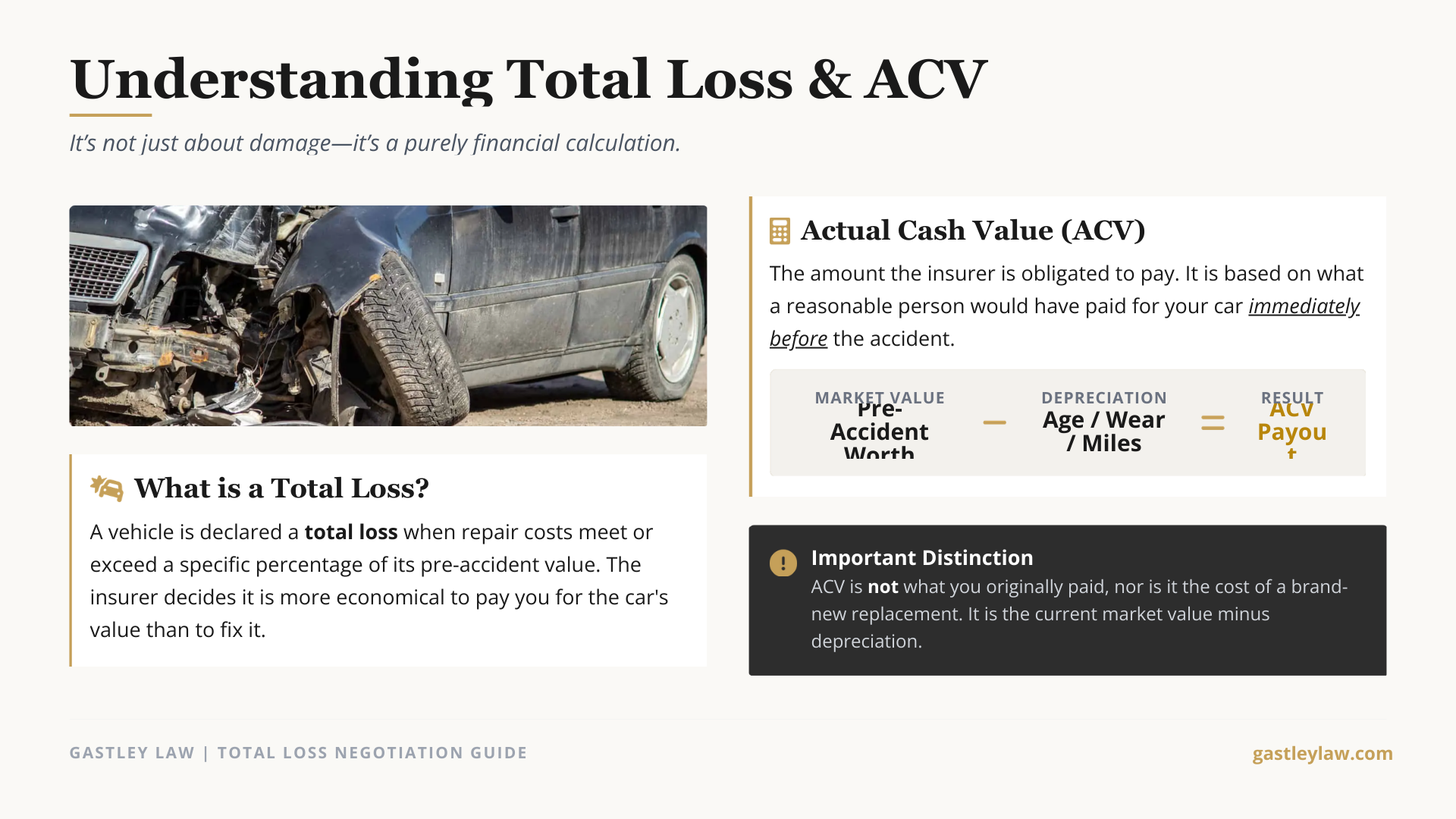

After a serious car accident, hearing the insurance company declare your car a “total loss” can feel like another blow. But what does that term actually mean? Simply put, a total loss claim happens when an insurer decides it costs more to repair your vehicle than it was worth right before the accident. It’s not just about whether the car is a crumpled mess; it’s a purely financial calculation. The insurance company is essentially saying it’s more economical for them to pay you for the car’s value and take possession of the damaged vehicle than it is to pay for extensive repairs.

This decision kicks off a process where the insurer determines your car’s value and makes you a settlement offer, and knowing how to file a third-party insurance claim can help you better understand what documentation and negotiation steps may strengthen your case. Understanding how they arrive at that number is the first step in making sure you get a fair payout. This is where many people feel powerless, but you have more say in the matter than you might think. The initial offer is just that—an offer. It’s the starting point for a negotiation, and being prepared can make a significant difference in the final amount you receive. The entire process can be confusing, but knowing the basics of how property damage claims work will put you in a much stronger position.

When is a Car Considered a Total Loss?

Your car is typically considered a total loss when the estimated cost of repairs meets or exceeds a certain percentage of its pre-accident value—a threshold that varies by state. It’s not just for cars that are completely mangled. Sometimes, a vehicle can look repairable, but hidden structural or electronic damage can make the repair costs skyrocket past its value. A car can also be declared a total loss if it’s stolen and not recovered. The key takeaway is that this is an economic decision made by the insurance company. They compare the repair estimate to the car’s market value. If fixing it doesn’t make financial sense for them, they will “total it out.”

How Insurers Determine Your Car’s Value

So, how does the insurance company decide what your car was worth? They calculate its “actual cash value,” or ACV, at the moment right before the crash occurred. An insurance adjuster will inspect the vehicle and use valuation reports from third-party companies to determine this number. They look at your car’s year, make, model, mileage, overall condition, and any pre-existing damage. They also consider recent sales of similar vehicles in your local market. This valuation is the most critical part of your claim, and it’s often where disagreements arise, especially when the insurer’s number directly affects your third-party insurance claim settlement payout and overall recovery. The insurer’s initial ACV assessment might seem low, which is why understanding your car’s true worth, including its diminished value, is essential before accepting an offer.

Understanding Actual Cash Value (ACV)

Let’s get one thing straight: Actual Cash Value (ACV) is not what you originally paid for the car, nor is it the cost to buy a brand-new replacement. ACV is the market value of your vehicle minus depreciation for age, wear and tear, and mileage. Think of it as what a reasonable person would have paid for your car right before the accident happened. This is the amount the insurance company is obligated to pay you under your policy. Because ACV is based on so many factors, it can be subjective. An insurer might overlook recent upgrades or use poor comps to justify a lower value. If their number seems unfair, you have the right to challenge it, but you’ll need evidence. If you feel overwhelmed, it might be time to contact us for help.

How to Challenge the Insurer’s Total Loss Valuation

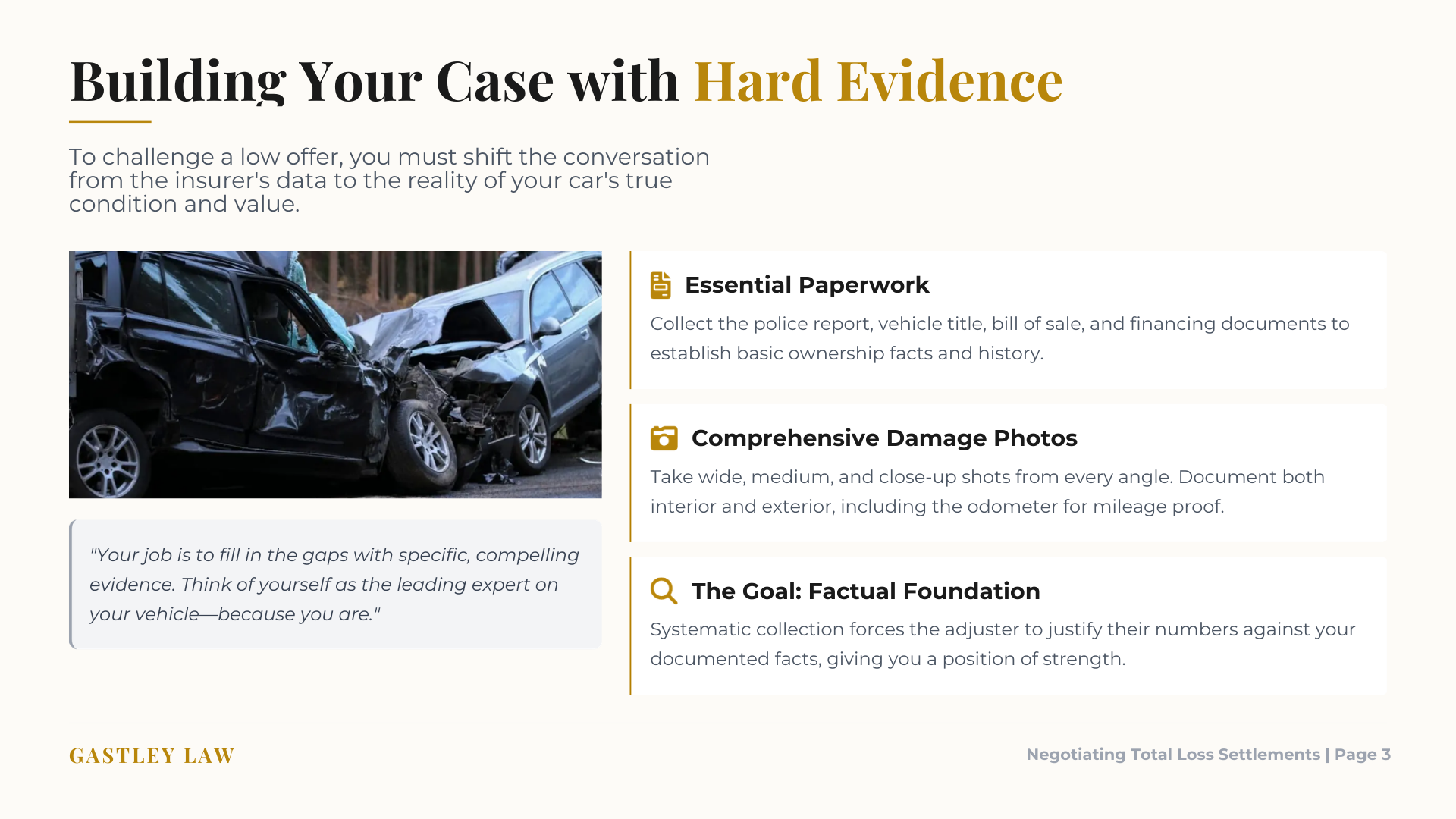

To successfully challenge the insurance company’s low offer, you need to build a case supported by solid proof. The adjuster has their own data, but it often doesn’t tell the whole story of your car’s unique value. Your job is to fill in the gaps with specific, compelling evidence. By systematically collecting documents, photos, and market data, you shift the conversation from their assessment to the reality of what your car was worth. This isn’t about being confrontational; it’s about being prepared. When you present a well-documented argument, you force the adjuster to justify their numbers against your facts, giving you a much stronger position to negotiate from. Think of yourself as the leading expert on your vehicle—because you are.

Key Documents to Collect

Start by gathering all the essential paperwork related to your vehicle and the accident. This includes the police report, your vehicle’s title, the bill of sale from when you purchased it, and any financing documents. These items establish the basic facts: your ownership, the car’s history, and the details of the incident. Having these documents organized and ready makes you look prepared and serious. If you’re unsure which documents are most important for your specific situation, our team can help you identify and organize what you need to build a strong foundation for your claim.

Take Detailed Photos of the Damage

Don’t rely solely on the photos taken by the insurance adjuster. Use your phone to take your own comprehensive set of pictures and videos as soon as possible after the accident. Capture the damage from every angle—wide shots, medium shots, and close-ups. Be sure to document the interior and exterior, including the odometer to show the mileage. Good lighting is key, so try to take photos during the day. This visual evidence is powerful and provides an unbiased record of the vehicle’s condition immediately following the collision, which can be crucial during negotiations.

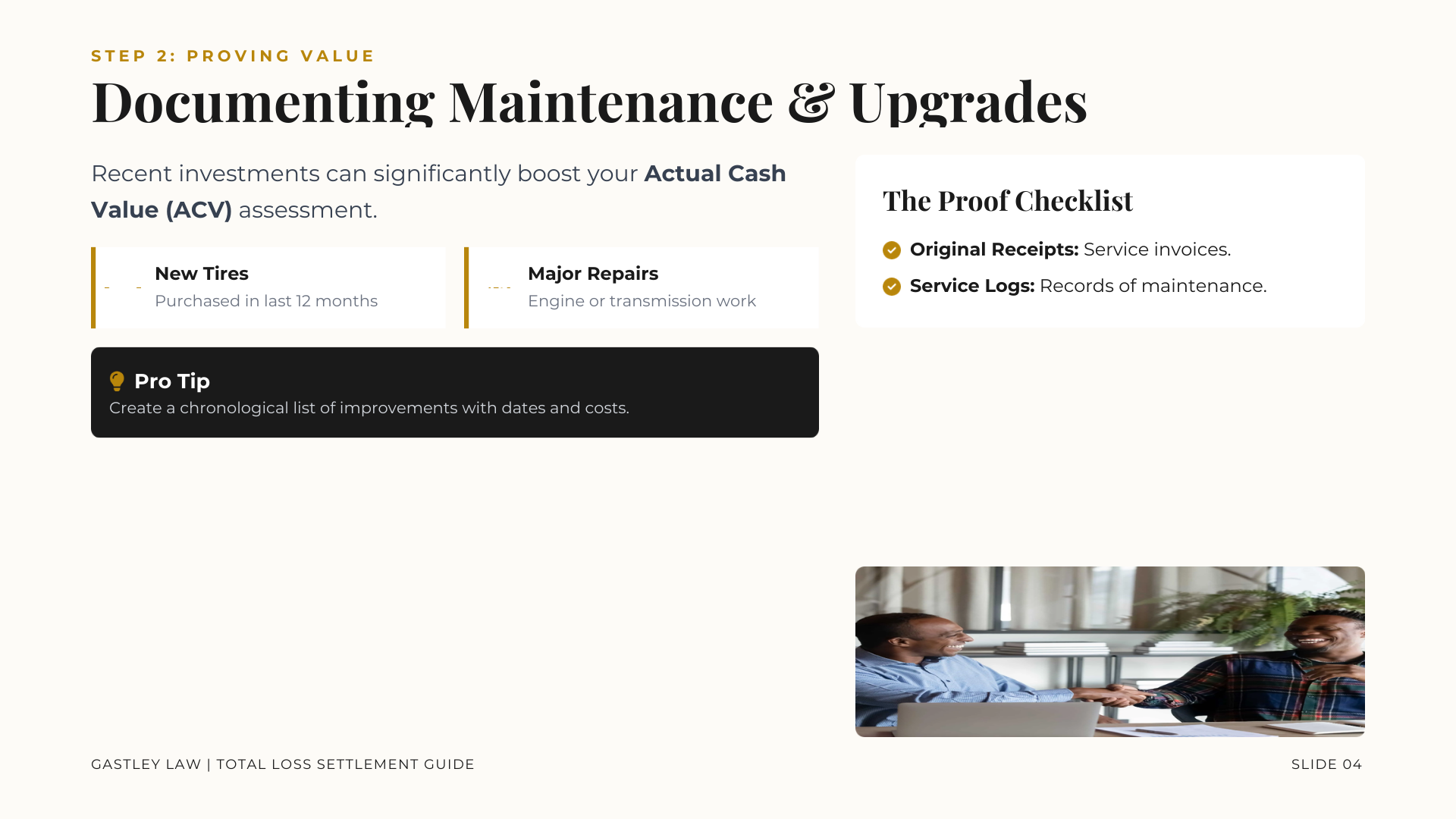

Document All Maintenance and Upgrades

Your car’s value isn’t just about its make, model, and year; it’s also about how well you cared for it. Dig up receipts for any recent maintenance or upgrades. Did you buy new tires in the last year? Get a new battery? Install a premium sound system? All of these things add value. Create a simple list of these improvements with dates and costs, and have the receipts ready to share. This documentation proves your vehicle was in excellent shape before the accident and helps justify a higher valuation, which is a key part of any diminished value claim.

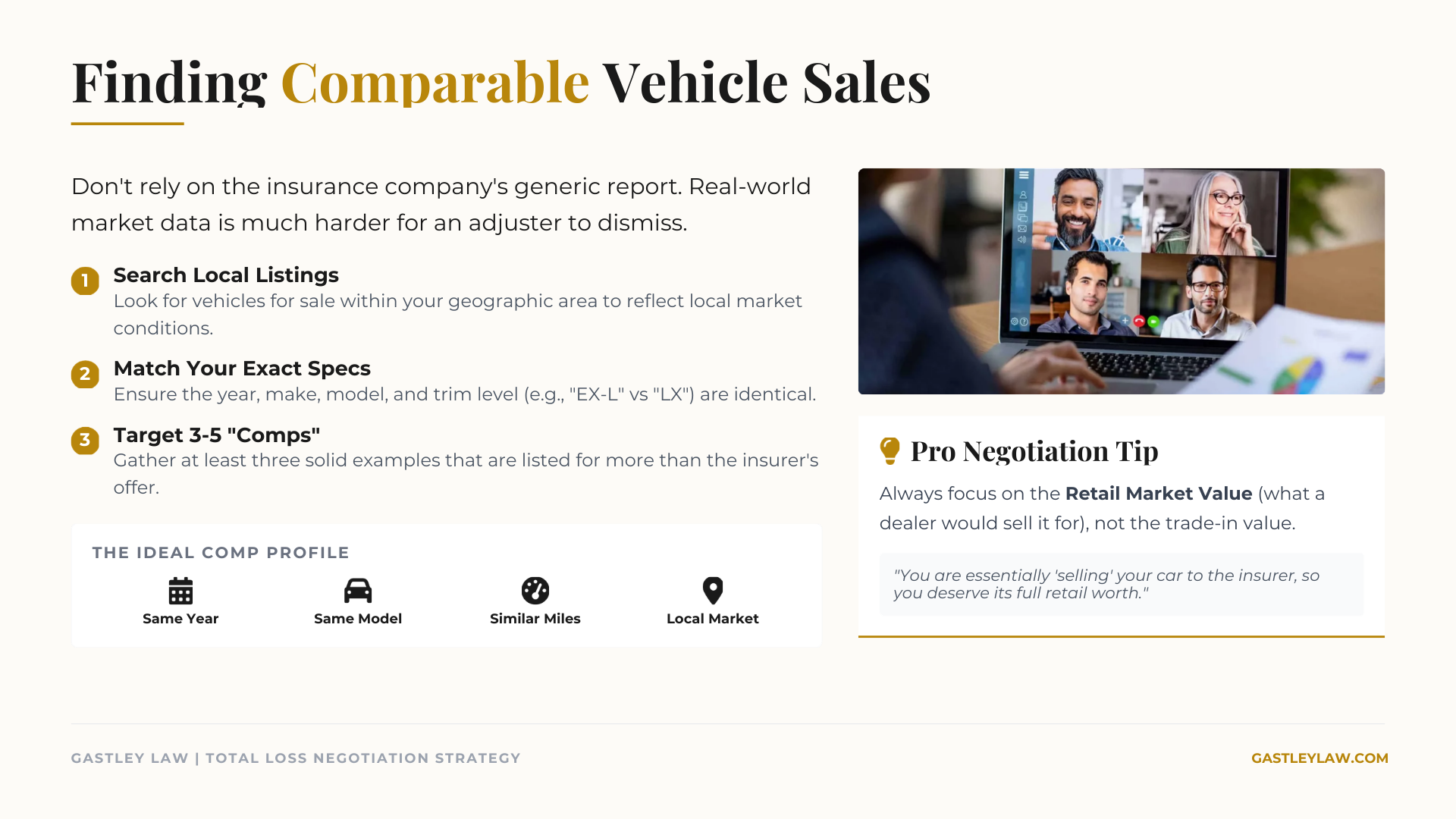

Find Comparable Vehicle Sales

One of the most effective ways to counter a low offer is to show the adjuster what it would actually cost to replace your car. Research comparable vehicles—the same make, model, year, and trim—for sale in your local area. Look for listings on dealership websites and online marketplaces. Pay close attention to cars with similar mileage and features. Save screenshots or printouts of at least three to five “comps” that are listed for more than the insurer’s offer. This real-world market data is much harder for an adjuster to dismiss than a generic valuation report.

One of the most effective ways to counter a low offer is to show the adjuster what it would actually cost to replace your car. Research comparable vehicles—the same make, model, year, and trim—for sale in your local area. Look for listings on dealership websites and online marketplaces. Pay close attention to cars with similar mileage and features. Save screenshots or printouts of at least three to five “comps” that are listed for more than the insurer’s offer. This real-world market data is much harder for an adjuster to dismiss than a generic valuation report.

The Benefit of a Professional Appraisal

If the insurance company won’t budge, consider getting an independent appraisal. An appraisal is a detailed report from a certified professional who assesses your vehicle’s pre-accident value. Many insurance policies include an appraisal clause in auto insurance that allows you to invoke this process. While it comes with a fee, a professional appraisal provides an expert, third-party valuation that carries significant weight in negotiations. It shows the insurer you are serious about getting fair compensation and can be a powerful tool to break a stalemate. Our legal services can guide you on when and how to best use an independent appraisal.

How to Negotiate a Higher Total Loss Settlement Step by Step

Walking into a negotiation without a plan is like going on a road trip without a map. You might get there eventually, but you’ll likely take a few wrong turns. A solid strategy is your best tool for securing a fair settlement for your totaled car. It’s not about being confrontational; it’s about being prepared. By doing your homework and approaching the conversation with confidence, you can clearly communicate why you deserve more than the insurance company’s initial offer. Let’s break down the key steps to building a strategy that works.

Set a Realistic Settlement Goal

Before you even pick up the phone, you need to know your number. Decide on a fair settlement amount for your vehicle that you can realistically aim for. This isn’t just a number you pull out of thin air; it should be the result of your research into your car’s actual value. Having this target in mind serves as your anchor throughout the negotiation process. It keeps you focused and prevents you from accepting a lowball offer simply because you’re tired of the back-and-forth. Think of it as your bottom line—the amount you know your car is truly worth and are prepared to fight for.

Research Your Car’s True Market Value

To argue for a fair settlement, you need to be armed with facts. Your opinion of what your car was worth won’t be enough; you need evidence. Start by researching your vehicle’s true market value based on its make, model, year, mileage, overall condition, and any recent upgrades. Use online resources like Kelley Blue Book to get a baseline. More importantly, look for comparable vehicles for sale in your local area. Finding listings for the same car with similar mileage and features provides powerful proof to counter an insurer’s low valuation. Save screenshots and links to these listings as part of your evidence file.

Write a Powerful Demand Letter

A formal demand letter is a professional and effective way to open negotiations. In this letter, you should formally reject the insurance company’s initial offer and clearly state the amount you believe is fair. The key is to back up your number with the evidence you’ve gathered. Include copies of comparable vehicle listings, receipts for recent maintenance or upgrades, and your independent appraisal if you have one. A well-written letter shows the adjuster you are serious and have done your homework. It forces them to justify their lower number and often prompts them to return with a more reasonable offer.

Use Our Communication Templates

Throughout this process, your motto should be “get it in writing.” After any phone call with the adjuster, send a follow-up email summarizing what was discussed. When you receive an offer, ask them to send it via email along with a copy of their complete valuation report. This document details exactly how they arrived at their number. Keeping a written record of all communication with your insurer creates a clear paper trail. This helps you stay organized and provides a reference point if there are any disagreements about what was said or promised. It’s a simple step that can save you major headaches later.

Follow Up Without Being a Pest

Insurance companies are busy, and sometimes, they use delays as a tactic, hoping you’ll get frustrated and accept a low offer. It’s important to be persistent without being a pest. Follow up regularly, but always maintain a professional and polite tone. At the end of each conversation, ask the adjuster when you can expect to hear from them next. If you don’t hear back by that date, send a polite follow-up email or make a call. This consistent, professional pressure shows them you are on top of your claim and expect it to be handled promptly and fairly.

How to Talk to the Insurance Adjuster

Talking to an insurance adjuster can feel intimidating, but it’s a crucial part of getting a fair settlement for your vehicle. The key is to be prepared, confident, and professional. Think of it as a business negotiation where you have the evidence on your side. Your goal is to clearly communicate the value of your car and why their initial offer falls short. By staying calm and organized, you can handle these conversations effectively and make a strong case for the compensation you deserve.

Understand the Adjuster’s Goals

First, it’s important to remember who the adjuster works for: the insurance company. Their primary goal is to resolve your claim while paying out as little as possible. They are trained negotiators, and their first offer is almost always a starting point, not a final number. Don’t take it personally; it’s just business. Understanding their objective helps you approach the conversation with the right mindset. You’re not there to argue, but to present a well-supported counter-position that demonstrates the true value of your vehicle and your property damage claim. Knowing their goal is to minimize costs empowers you to advocate for yourself effectively.

Present Your Evidence with Confidence

Confidence comes from preparation. Before you even speak with the adjuster, you should have all your evidence organized and ready to go. This includes your detailed photos, maintenance records, receipts for upgrades, and a list of comparable vehicles you found during your research. When you present this information, do it with assurance. Instead of just saying you think your car is worth more, you can say, “I have records showing the engine was replaced six months ago,” or “Here are three similar vehicles currently for sale in our area for a higher price.” Solid proof is much more persuasive than opinions. This documentation is also essential for proving your car’s pre-accident value, a key component of any diminished value claim.

What to Do When They Lowball You

It’s extremely common to receive a lowball offer, so try not to get discouraged. When you get the initial valuation, your first step is to politely reject it and state that you believe it’s too low based on your research. Ask the adjuster to provide a detailed breakdown of how they arrived at their number. Carefully review their valuation report for any errors or omissions. Did they list the wrong trim package? Did they miss recent upgrades or fail to account for your car’s excellent condition? Point out these specific inaccuracies and provide the documentation that proves your case. This shifts the conversation from a simple disagreement to a fact-based negotiation.

Best Practices for a Smooth Negotiation

To keep the negotiation process moving smoothly, always communicate clearly and professionally. When the adjuster makes an offer, ask them to send it to you in writing via email. This creates a paper trail and prevents any misunderstandings. Also, request a copy of their complete valuation report so you can review it line by line. Be prompt in providing any documents they request, like your maintenance records or the vehicle’s original window sticker. By being organized and responsive, you show them you’re serious and prepared. This professional approach can make the adjuster more willing to work with you toward a fair resolution.

Keep a Record of Every Conversation

Documentation is your best friend throughout this entire process. Keep a dedicated folder for everything related to your claim. Save every email and piece of mail you receive from the insurance company. After every phone call, jot down notes with the date, time, the adjuster’s name, and a summary of what was discussed. This detailed record is invaluable if there are any disputes later on. It ensures you have proof of what was said and agreed upon. If the negotiation stalls or becomes too difficult to handle on your own, having a complete file makes it much easier for a legal professional to step in and help. If you find yourself in that position, don’t hesitate to contact us for support.

Common Negotiation Mistakes to Avoid

Going through a total loss claim can feel like walking through a minefield, but knowing what not to do is just as important as knowing what to do. Insurance companies handle these claims every day, and they have a process designed to minimize their payout. By avoiding a few common pitfalls, you can keep the negotiation on a level playing field and protect your right to fair compensation. Let’s walk through the mistakes we see most often so you can steer clear of them.

Accepting the First Offer

It can be tempting to take the first offer the insurance company throws your way, especially when you just want the whole ordeal to be over. But please, don’t do it. Remember, the insurance company’s goal is to settle your claim for as little money as possible. Their first offer is almost always a lowball figure, a starting point for negotiation. Instead of seeing it as the final amount, treat it as an invitation to discuss what your car is actually worth. Accepting that initial number means you could be leaving hundreds or even thousands of dollars on the table—money you’re rightfully owed for your diminished value and property damage.

Overlooking Important Documents

When the adjuster presents their offer, always ask them to send it to you in writing, along with a copy of their complete valuation report. This report is the key to their math—it shows how they arrived at their number. Don’t just file it away. As experts at Clearsurance advise, you need to check this report carefully to ensure every detail is accurate. Having these documents on hand creates a paper trail and gives you the information you need to build a strong counter-offer. A verbal offer over the phone isn’t enough; you need to see the data for yourself.

Missing Errors in Their Valuation

Once you have the valuation report, it’s time to put on your detective hat. Insurance adjusters are human, and their reports can contain mistakes that drastically lower your car’s value. Go through it line by line. Did they list the correct trim level for your vehicle? Are all of its special features and upgrades included, like a premium sound system or a sunroof? Is the mileage correct? Even a small error, like misstating the trim package, can change the valuation significantly. If you find any discrepancies, document them immediately. This is often the easiest way to get the adjuster to increase their offer. Our team is trained to spot these errors during our thorough case evaluations.

Using the Wrong Communication Style

Dealing with an insurance adjuster can be frustrating, but letting your emotions get the best of you won’t help your case. The best approach is to be firm, professional, and persistent. Insurance companies sometimes use delay tactics, hoping you’ll get tired of fighting and accept a low offer. As legal professionals at Gingras Thomsen & Wachs LLP note, it’s important to “keep the pressure on, but stay professional.” Keep detailed notes of every conversation, follow up regularly via email, and present your evidence calmly and confidently. A polite, organized approach is much more effective than an angry, demanding one.

Not Getting the Final Offer in Writing

After some back-and-forth, you may finally reach a settlement amount you’re happy with. But your work isn’t quite done. A verbal agreement over the phone is not legally binding. Before you consider the matter closed, you must get the final settlement offer in writing. This can be a formal letter or a simple email, but it needs to clearly state the agreed-upon amount. This written confirmation protects you and ensures there are no misunderstandings later on. Never sign a release form or accept a check until you have this final, written offer in hand. If you have any doubts before signing, it’s a good time to contact an attorney for a final review.

What to Check Before Accepting a Total Loss Settlement

Once you have your evidence and strategy in place, it’s time to focus on the negotiation itself. The goal is to secure a settlement that truly reflects what your vehicle was worth. This isn’t about being confrontational; it’s about being prepared and firm. Insurance adjusters handle these claims every day, but you have the advantage of knowing your car better than anyone. By focusing on the facts and presenting a clear, well-supported case, you can confidently work toward a fair outcome. These five steps will help you make sure you’re covering all your bases and leaving no money on the table.

What to Check Before Accepting a Total Loss Settlement

Before accepting a total loss settlement, take time to review every part of the insurer’s offer carefully. Many drivers focus only on the headline number, but the real value of the settlement depends on how that number was calculated. Start by reviewing the valuation report line by line. Confirm that the insurer listed the correct year, make, model, trim, mileage, optional features, and overall condition of your vehicle. Even a small mistake can reduce the offer by hundreds or thousands of dollars.

Next, compare the insurer’s comparable vehicle listings against the local market. If the report uses vehicles from outside your area or comps with fewer features than your car had, the valuation may be artificially low. You should also confirm whether the settlement includes related costs such as taxes, title fees, registration fees, and any other amounts allowed under your policy or state rules.

It is also important to check whether the insurer properly considered recent maintenance, upgrades, and the car’s pre-accident condition. If you installed new tires, replaced major components, or kept the vehicle in excellent shape, that information should support a higher value. Finally, never accept a verbal agreement alone. Ask for the final offer in writing and review it before signing any release. A careful review at this stage can prevent you from settling for less than your claim is actually worth.

Include All Eligible Costs

It’s important to understand that insurance companies pay the “Actual Cash Value” (ACV) of your car, which is its market value right before the accident—not what it costs to buy a brand new one. However, ACV should cover more than just the vehicle itself. Check your policy and your state’s regulations, as you may be entitled to reimbursement for sales tax, title transfer fees, and registration costs for a replacement vehicle. Don’t forget to factor in the car’s loss of value, even after repairs. This is known as a diminished value claim, and it’s a crucial part of your total compensation that insurers often overlook unless you bring it up. Make a comprehensive list of every eligible expense to ensure your final settlement is complete.

Use Your Evidence to Your Advantage

Your negotiation power comes directly from the quality of your evidence. Simply stating that you think your car is worth more won’t get you very far. When the adjuster provides their initial offer, ask them to send it via email along with their official valuation report. This document shows exactly how they arrived at their number. Carefully compare their report to the research you’ve gathered, including your maintenance records, photos, and list of comparable vehicles. If you find discrepancies—like incorrect mileage, missing features, or comps from a different geographic area—you can present your proof to counter their assessment. A well-documented argument is much harder for an adjuster to dismiss.

Get Multiple Valuations

Don’t rely on the insurance company’s valuation alone. The number they give you is just their starting point. To build a strong counteroffer, you need to establish your car’s retail market value. Search online auto sites for vehicles that are the same make, model, year, and trim as yours, with similar mileage and in similar pre-accident condition. Save screenshots of at least three to five local listings. This shows the adjuster what it would actually cost you to buy a comparable car in your area. Remember to focus on the retail price (what a dealer would sell it for), not the trade-in value. You are essentially “selling” your totaled car to the insurer, so you deserve its full retail worth.

Know Your Rights as a Policyholder

Your auto insurance policy is a contract, and it outlines your rights in a claims dispute. If you believe the settlement offer is too low, you have the right to negotiate. Many people don’t realize this and simply accept the first number they’re given. Before you even speak to the adjuster, review your policy for a section on dispute resolution or an “appraisal clause.” This clause allows you and the insurer to each hire an independent appraiser to determine the vehicle’s value if you can’t agree. Knowing your policy’s specific terms gives you confidence and shows the adjuster you’ve done your homework. If the language is confusing, our team can help you understand your legal options.

Time Your Negotiations Strategically

Patience is a powerful tool in any negotiation. Insurance companies often make a low initial offer, hoping you’ll accept it quickly to get the process over with. Don’t fall for this tactic. When you receive the first offer, politely decline it and ask the adjuster to walk you through how they calculated that specific amount. This opens the door for you to present your own evidence and start a productive conversation. Avoid ultimatums or emotional arguments. Instead, remain calm, professional, and persistent. If you feel the negotiation has stalled or the adjuster is unwilling to be reasonable, it may be the right time to get in touch with an attorney.

Know When to Call for Legal Help

Negotiating with an insurance adjuster can feel like a full-time job, and sometimes, despite your best efforts, you hit a wall. While you can handle many parts of the process yourself, there are moments when bringing in a professional is the smartest move you can make. An experienced attorney knows the insurance company’s playbook and can step in to advocate for you, ensuring your claim is taken seriously. Think of it as bringing in an expert to level the playing field and manage the fight for you, so you can focus on everything else.

Signs It’s Time to Contact an Attorney

You might be wondering if your situation really calls for a lawyer. If the insurance company is using delay tactics, giving you the runaround, or simply ignoring your calls and emails, it’s a major red flag. Another clear sign is a lowball offer that doesn’t even come close to your car’s actual cash value. When the adjuster refuses to provide a logical reason for their low valuation or pressures you to accept a settlement immediately, it’s time to pause. If you feel overwhelmed, intimidated, or that you’re not being treated fairly, trust your gut. You don’t have to accept their terms, and a quick call can help you understand your options.

The Benefits of Professional Legal Support

Hiring an attorney does more than just put a stop to frustrating phone calls. A legal professional understands the specific laws in Georgia that protect you. They can conduct a detailed analysis of your claim, accurately calculate your vehicle’s diminished value, and identify all the costs you’re entitled to recover. An attorney handles all communication with the insurance company, presents your evidence in the most compelling way, and negotiates from a position of strength. This not only saves you an incredible amount of time and stress but also significantly improves your chances of receiving a fair settlement that truly reflects what you’ve lost.

How to Review the Final Settlement

Before you even think about accepting an offer, you need to see it in writing. Ask the adjuster to email you the official settlement offer along with a copy of their valuation report. This report, often from a third-party service like CCC Intelligent Solutions, is the basis for their offer, and it’s frequently full of errors. Carefully check it for the correct trim level, mileage, and optional features your car had. They might have missed your recent tire replacement or that premium sound system. Finding these mistakes and pointing them out is one of the most effective ways to challenge a low offer and demand a higher payout.

What to Expect During the Final Steps

If your negotiations reach a stalemate and the insurance company won’t offer a fair amount, you have other options. The next step might involve mediation or even filing a lawsuit. This is the point where having an attorney is critical. A lawyer can manage the entire legal process, from filing the necessary paperwork to representing you in court, if it comes to that. While most claims are settled before a trial becomes necessary, the insurance company is much more likely to make a serious offer when they know you have an expert on your side who is fully prepared to take your case to court. Our team is experienced in handling these legal services for our clients.

Finalize Your Claim and Get Paid

Once you and the insurer agree on a number, get the final settlement agreement in writing. This document is legally binding, so read it carefully before you sign. It will likely include a “release of all claims,” which means that once you accept the payment, you can’t ask for more money for this incident later on. An attorney can review this paperwork for you to make sure there are no hidden clauses and that the terms are exactly what you agreed to. After you sign, the insurance company will issue the check, closing out your claim and allowing you to finally move forward.

Related Articles

- Can You Reject a Total Loss Offer? A Simple Guide

- Diminished Value Claims – Gastley Law Advocates

- What to Do: Disagree With a Car Damage Appraisal

Frequently Asked Questions

What happens if I owe more on my car loan than the insurance company’s settlement offer?

This is a tough situation, and it happens more often than you’d think. If the settlement for your car’s actual cash value is less than your loan balance, you are typically responsible for paying the difference. This is where GAP (Guaranteed Asset Protection) insurance comes in handy, as it’s designed to cover that exact “gap.” If you don’t have GAP coverage, negotiating for the highest possible settlement becomes even more critical to minimize your out-of-pocket costs.

Can I keep my car even if it’s declared a total loss?

In many cases, yes, you can choose to keep your vehicle. If you go this route, the insurance company will pay you the car’s actual cash value minus its salvage value—the amount they would have gotten for selling the damaged car to a scrap yard. Just be aware that your car will be issued a “salvage title,” which can make it difficult to insure, register, and sell in the future.

Is it really worth hiring an attorney for just a car damage claim?

While it might seem like overkill, it’s often a smart financial move. Insurance companies have teams of people working to pay out as little as possible. An attorney who specializes in property damage claims levels the playing field. They know how to accurately value your loss, including diminished value, and can often negotiate a final settlement that is significantly higher than what you could get on your own, more than covering their fee.

How long does a total loss negotiation usually take?

The timeline can vary quite a bit, from a few weeks to several months. The length depends on how far apart you and the insurer are on the car’s value and how responsive the adjuster is. Having all your evidence organized from the start can help move things along, but it’s important not to rush. The insurance company’s first offer is designed for a quick, cheap settlement, so taking the time to negotiate properly is almost always worth it.

What’s the single biggest mistake I can make during this process?

The most costly mistake is accepting the insurance company’s first offer without questioning it. That initial number is a starting point, not a final decision. By immediately accepting it, you’re likely leaving money on the table that you are rightfully owed. Always take a step back, ask for their valuation report in writing, and do your own research before ever agreeing to a number.