Can You Reject a Total Loss Offer? Yes, Here’s How

Yes. You can reject a total loss offer if you believe the insurer undervalued your vehicle. Rejecting the first offer does not end your claim. It starts a negotiation in which you can challenge the valuation with the insurer’s report, comparable local vehicles, maintenance records, upgrade receipts, and other proof of your car’s pre-accident value. Before you accept or sign a release, review how the insurer calculated the offer and put your counteroffer in writing.

If a Georgia insurer will not correct a low total loss valuation, Gastley Law can review the paperwork and explain your options. Contact Gastley Law for help evaluating the offer.

As Georgia’s most prolific diminished value claims law firm, our goal is to give you a clear, actionable plan to fight back. We’ll cover how to find your car’s true market value, what paperwork you need to prove it, and how to negotiate effectively to secure the settlement you are owed.

Key Takeaways

- You can reject the first offer. Ask for the complete valuation report before accepting or signing a release.

- Build an evidence file. Compare the report with local vehicles of the same year, make, model, trim, mileage, options, and condition; save listings, maintenance records, and upgrade receipts.

- Counter in writing and escalate deliberately. State the amount you believe the vehicle was worth, explain the evidence, keep a paper trail, and consider appraisal or legal help if negotiations stall.

What is a “Total Loss” Offer?

After a car accident, hearing the words “total loss” from an insurance adjuster can feel like another blow. Simply put, a “total loss” offer is what an insurance company gives you when they decide the cost to fix your car is more than what the car was worth right before the crash. This offer is for your car’s “Actual Cash Value” (ACV), which is the insurer’s estimate of its market value, accounting for depreciation.

It’s important to remember that this is the insurance company’s initial assessment. It’s a number they’ve calculated based on their own data and formulas, but it’s not the final word. You have the right to review their valuation, understand how they reached that number, and push back if you believe it’s too low. The adjuster’s first offer is just that—an offer. It’s the starting point for a negotiation, and knowing how they arrived at their figure is the first step in making sure you get the fair settlement you deserve.

How Insurers Calculate Your Car’s Value

So, what exactly is “Actual Cash Value”? It’s not what you paid for the car or what a brand-new replacement would cost. ACV is the amount someone would have reasonably paid for your car the moment before the accident happened. To determine this, insurance adjusters look at several factors, including your car’s make, model, age, mileage, and overall condition. They also consider any special features or recent upgrades you’ve made. They plug this information into valuation reports from third-party companies to generate a number. However, these reports can sometimes miss key details or rely on inaccurate comparisons, leading to a lowball offer. Our legal representation can help you challenge these valuations and fight for what your car was truly worth.

What Makes a Car a Total Loss?

An insurance company will declare your car a total loss if it’s not economically practical to repair it. Each state has its own rules, but the general principle is the same: if the estimated cost of repairs plus the car’s remaining salvage value is more than its pre-accident ACV, the insurer will total it. This is a business decision for them. It’s often cheaper for the insurance company to write you a check for the car’s value than to pay for extensive repairs. If you disagree with their assessment or believe the repair estimate is inflated, it’s crucial to act. When you feel the insurer’s math doesn’t add up, it may be time to contact an attorney to review your case.

Know Your Rights When an Insurer Totals Your Car

After a car accident, dealing with an insurance company can feel like a full-time job, especially when they declare your car a total loss. It’s easy to feel pressured into accepting their terms, but it’s so important to remember that you have rights in this situation. The insurance adjuster works for the insurance company, and their primary goal is to resolve your claim for the lowest possible amount. Understanding your rights is the first step toward ensuring you get the fair compensation you deserve for your vehicle. This means knowing that their first offer isn’t final, understanding how Georgia law applies to your situation, and being clear on what the insurance company is legally required to pay you. Arming yourself with this knowledge will help you stand your ground and fight for what you’re owed.

You Don’t Have to Accept the First Offer

When the insurance adjuster calls with a settlement amount for your totaled car, it can feel like a take-it-or-leave-it deal. But here’s the most important thing to remember: you are not required to accept their first offer. In fact, you probably shouldn’t. Think of the initial offer as a starting point for negotiation, not the final word. If the amount seems too low to replace your car with a similar one, you have every right to reject that settlement offer and push for a better deal. Saying no simply signals to the insurer that you know your car’s worth and are prepared to advocate for a fair payment that truly covers your loss.

Georgia’s Rules for Total Loss Claims

In Georgia, specific rules determine when a car is declared a total loss. An insurer will typically “total” your vehicle if the cost of repairs is greater than the car’s Actual Cash Value (ACV) before the accident. The ACV is the amount your car was worth right before the crash—think of it as the price you could have sold it for at that moment. The insurance company calculates this value based on your car’s year, make, model, mileage, and overall condition. Understanding this threshold is key, as it’s the basis for the insurer’s decision. It’s not an arbitrary choice; it’s a calculation. However, their calculation of your car’s ACV is where disagreements often begin.

What Your Insurance Company Legally Owes You

If your car is officially a total loss, the insurance company is legally obligated to pay you its Actual Cash Value (ACV), minus any deductible on your policy. This payment is meant to be enough for you to purchase a comparable replacement vehicle. However, the insurer’s initial ACV calculation might not account for recent upgrades, special features, or the excellent condition you kept your car in. It’s their job to pay the claim, but it’s your job to make sure their valuation is accurate. You can challenge their number by providing your own evidence, which is a critical part of securing fair property damage compensation.

How to Know if Their Offer is Fair

After a car accident, the insurance company’s settlement offer can feel like a finish line. But before you accept it, take a moment to breathe and look closer. Insurance adjusters are focused on closing claims quickly and for the lowest amount possible, which means their first offer might not reflect what you’re truly owed. It’s your right—and your responsibility—to make sure the number they’ve presented is actually fair. Remember, the adjuster works for the insurance company, not for you. Their goal is to protect their employer’s bottom line, and they handle dozens of claims just like yours every week.

Doing your own homework is the best way to protect your financial interests. You need to understand your car’s real value, gather the proof to back it up, and account for all the related expenses that the insurer might have overlooked. This isn’t about being difficult; it’s about getting the full compensation you deserve to make things right. By taking a systematic approach, you can confidently assess their offer and decide on your next move. We’ll walk you through exactly how to determine if the offer is fair, what proof you’ll need, and the hidden costs you can’t afford to ignore.

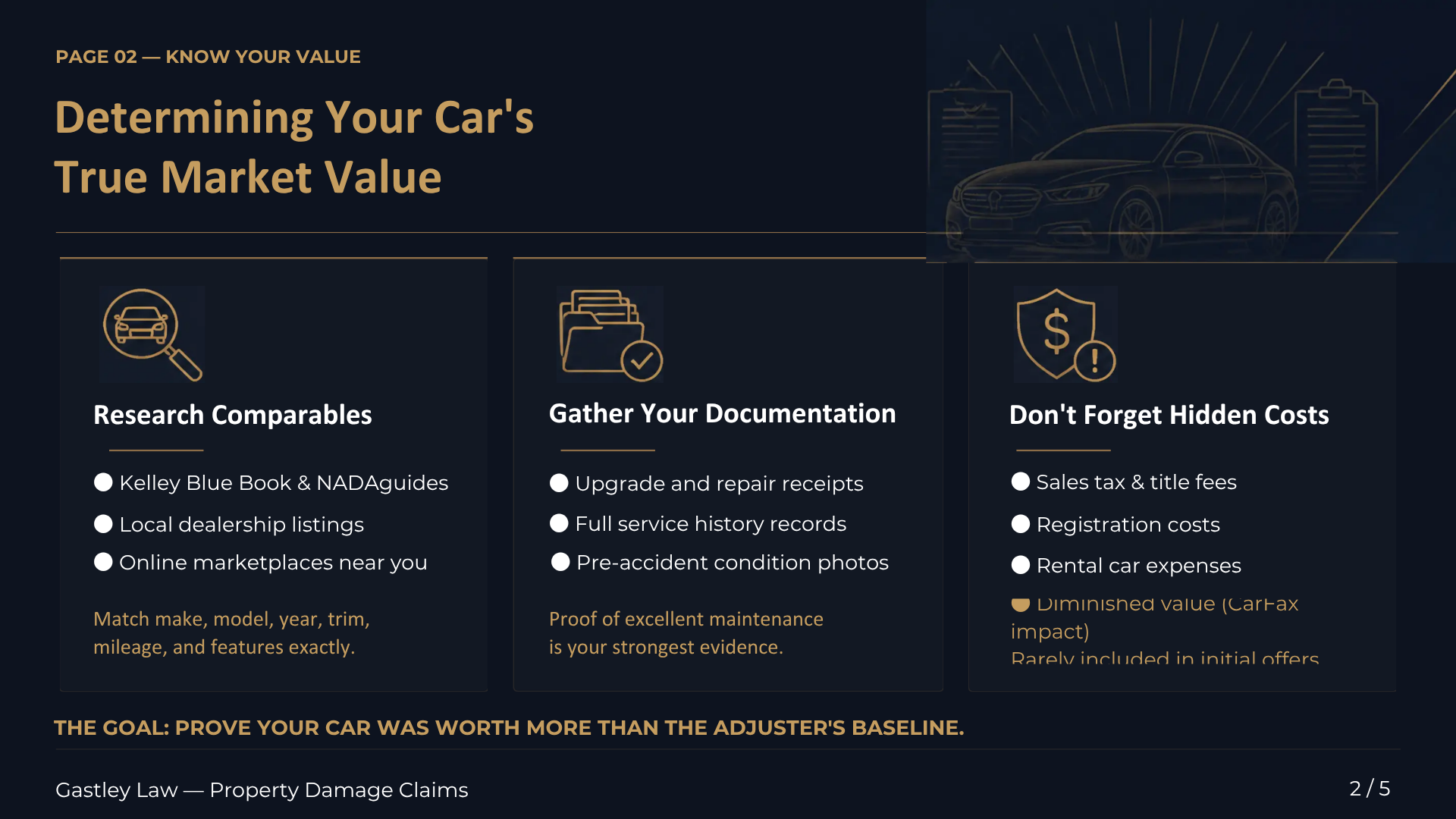

Find Your Car’s True Market Value

The first step in evaluating an offer is to determine your car’s actual cash value (ACV) right before the accident. Don’t just take the insurer’s number at face value. You need to conduct your own research to find out what a willing buyer would have paid for your car. Start by looking up your vehicle’s make, model, year, and mileage on trusted sites like Kelley Blue Book and NADAguides. More importantly, search local dealership sites and online marketplaces for comparable vehicles for sale in your area. Pay close attention to cars with similar trim packages, features, and overall condition. This local market data is powerful evidence when negotiating for a fair settlement.

The Paperwork You’ll Need to Prove It

An insurance company’s valuation is based on a standard formula, but it doesn’t know the specific history of your car. It’s up to you to prove its unique value. Did you recently buy new tires? Add a premium sound system? Keep meticulous maintenance records? Now is the time to gather all that paperwork. Collect receipts for any upgrades or major repairs, pull your full service history, and find photos that show your car’s excellent condition before the crash. This documentation helps paint a clear picture of a well-maintained vehicle that was worth more than the average book value. Having this evidence organized makes it much easier to justify a higher payout and shows the adjuster you’ve done your research.

Don’t Forget These Hidden Costs

A fair offer covers more than just the car itself. You need to account for all the related expenses that come with replacing a vehicle. This includes sales tax, title fees, and registration costs for your new car—all of which should be factored into the settlement. Furthermore, the offer should cover any rental car expenses you incurred. Most importantly, you need to consider your vehicle’s diminished value. Even if your car is repaired, it now has an accident history, which significantly lowers its resale value. Insurance companies rarely include this in their initial offer, but it’s a real financial loss you are entitled to recover. If you need help calculating these costs, our team is ready to review your case.

How to Counter a Lowball Total Loss Offer

Receiving a lowball offer for your totaled car can feel like a final insult after the stress of an accident. But here’s the good news: you don’t have to accept it. The insurance company’s first offer is just that—an offer. It’s the start of a negotiation, and with the right approach, you can push for the fair compensation you deserve. It all comes down to proving your car’s actual worth and confidently presenting your case.

What Evidence Helps You Challenge a Total Loss Offer?

If you want to push back against a low total loss offer, the strength of your evidence often determines the outcome. Insurance companies rely on valuation reports, but those reports are not always complete or accurate. That is why building your own file of supporting documents can make a major difference during negotiations.

Start with local comparable vehicle listings. Look for cars with the same make, model, year, trim level, mileage range, and major features. Local dealership listings and marketplace results can show what similar vehicles are actually selling for in your area, which is often more persuasive than a generic valuation report. You should also gather service records, upgrade receipts, and proof of recent repairs. New tires, brake work, a replacement transmission, or premium aftermarket features may all support a higher value.

Photos are another powerful tool. Clear images showing your car’s condition before the accident can help prove that the vehicle was well maintained and worth more than the insurer claims. If the adjuster’s report contains mistakes, such as the wrong trim package, incorrect mileage, or missing options, point those out in writing. The more specific your evidence is, the harder it becomes for the insurer to justify a low offer. A well-organized package of proof can move negotiations in your favor and help you pursue a settlement that reflects your car’s true pre-accident value.

Gather Your Evidence

To successfully counter a lowball offer, you need to show the insurance adjuster why your car is worth more. Your opinion alone isn’t enough; you need proof. Start by collecting every document you can find related to your vehicle. This includes maintenance records, receipts for new tires or recent repairs, and proof of any upgrades like a new sound system or custom wheels. As one expert notes, you should “[c]ollect documents, photos, and videos that show your car’s condition and any recent improvements you made.” This evidence builds a strong foundation for your claim and demonstrates the true value of your vehicle before the accident.

Write a Strong Counter-Offer

Once you have your evidence, it’s time to formally reject their offer and present your own. You can absolutely say no to an initial settlement if it doesn’t cover your costs. In fact, “[s]aying no tells the insurance company you want to negotiate for a better deal.” Draft a clear, professional letter or email to the adjuster. State that you are rejecting their offer and explain exactly why, using the evidence you’ve gathered. Itemize the comparable vehicles you found, reference your car’s excellent condition, and attach copies of your receipts and records. The goal is to make it impossible for them to ignore the facts. If you’re unsure how to phrase it, our team can help you craft a compelling response.

Simple Negotiation Tactics

Remember that negotiation is a process. The insurance company is a business, and its first goal is to protect its profits by paying out as little as possible. Because of this, “[i]nsurance companies often offer low amounts first to save money.” Don’t be discouraged if they don’t immediately accept your counter-offer. Stand firm on your valuation and be prepared for some back-and-forth. Respond to their points calmly and refer back to your evidence. Clearly restating the facts and showing you’ve done your homework can make a significant difference. This is where having an experienced attorney handle the negotiation for you can take the pressure off and often lead to a better outcome.

You’ve Rejected the Offer. Now What?

So you’ve said “no” to the insurance company’s initial offer. Take a deep breath—that was a big, important step. Rejecting a lowball offer isn’t the end of the road; it’s the beginning of the negotiation. You’ve signaled to the adjuster that you know your car is worth more and you’re prepared to fight for a fair settlement. This is where you stand your ground and work toward getting the compensation you actually deserve.

Now, the ball is back in your court to make the next move. The adjuster is waiting to see what you’ll do. Your next steps will set the tone for the rest of the negotiation, so it’s crucial to be prepared, organized, and confident. Let’s walk through what happens next and how you can stay in control of the process.

The Counter-Offer Timeline and Process

After you reject the first offer, the next step is to submit a counter-offer. This is where you present the evidence you’ve gathered—your independent valuations, repair estimates, and receipts—and state the amount you believe is fair. This is usually done in writing to create a clear paper trail. From here, a bit of back-and-forth is normal. The adjuster may come back with a slightly higher number, and you might counter again. This can continue until you both reach an agreement. The timeline varies, but don’t be discouraged if it takes a few rounds. If the process feels overwhelming, this is the perfect time to contact an attorney to take over the negotiations for you.

What to Expect from the Insurance Company

Insurance companies are businesses, and their goal is to pay out as little as possible on claims to protect their profits. Their first offer is almost always low for this exact reason. They expect you to negotiate. When you reject their offer, you’re simply playing the game by its rules. The adjuster won’t be surprised or offended. They will likely ask you to justify your higher number, which is why having all your documentation ready is so important. They may try to poke holes in your evidence, but stay firm and stick to the facts you’ve gathered about your car’s true value and your right to diminished value compensation.

Will This Affect Your Insurance Policy?

It’s natural to worry if pushing back on a claim will negatively affect your policy, like causing your rates to go up. Generally, negotiating a settlement for a single claim won’t impact your policy, especially if you weren’t at fault for the accident. You are entitled to the fair market value of your vehicle, and pursuing that is your right as a policyholder. The negotiation is separate from your policy’s terms and premiums. The real decision that affects your policy is what you do with the car. If you keep a totaled vehicle, your insurer may require it to have a salvage title and may limit future coverage on it. This is one of the many complex property damage claims where having an expert on your side can make all the difference.

How to Talk to the Insurance Adjuster

Speaking with an insurance adjuster can feel like a high-stakes conversation, because it is. Their job is to resolve your claim for the lowest possible cost to their company. Your goal is to get the full and fair compensation you deserve. Going into the conversation prepared, calm, and confident can make all the difference. Remember, you are in control of the information you share.

Tips for Clear and Firm Communication

When you speak with the adjuster, stick to the facts of the accident and the details of your car’s value. Avoid speculating, apologizing, or admitting any fault. It’s okay to say, “I don’t have that information right now” or “I need to review my documents before I answer that.” Be polite, but don’t be afraid to be firm. If you believe their offer is too low, you can clearly state that you do not accept it and will be providing evidence to support a higher valuation. You can always negotiate for a better offer if you feel the initial one is unfair. Keep a log of every call, including the date, time, who you spoke with, and what was discussed.

Watch Out for These Common Adjuster Tactics

Insurance companies are businesses, and they protect their bottom line by paying out as little as possible on claims. Because of this, their first offer is almost always a low one. An adjuster might pressure you for a quick settlement, hoping you’ll accept before you realize your car’s true worth. They may also ask to record your statement early on, which can be used to find inconsistencies in your story later. Be wary of friendly conversations that stray from the facts of the claim. Always remember that the adjuster is not on your side, even if they seem helpful. They are trained negotiators working for their employer, not for you.

When It’s Time to Call a Lawyer

If you’ve presented your evidence and the insurance company still won’t offer a fair settlement, it’s time to bring in a professional. You should also seek legal advice if the claims process becomes overwhelming or if the adjuster is using high-pressure tactics. An experienced attorney understands how to value a claim, including often-overlooked aspects like diminished value. They can take over all communication with the insurer, present your case effectively, and fight to get you the compensation you’re owed. If you feel like you’re being ignored or lowballed, don’t hesitate to contact a lawyer to discuss your options.

What to Do When Negotiations Stall

It’s incredibly frustrating when the insurance adjuster stops negotiating or refuses to budge from a lowball offer. You might feel like you’ve hit a wall, but you still have powerful options. When the conversation goes cold, it’s not the end of the road—it’s a sign that it’s time to change your strategy. Instead of giving in, you can take clear, decisive steps to escalate the issue and fight for the fair settlement you deserve. Don’t let the insurance company’s silence be the final word. Here are three effective ways to break the stalemate.

Get an Independent Appraisal

If you and the insurer are at an impasse over your car’s value, it’s time to bring in a neutral third party. Most auto insurance policies contain an “appraisal clause,” which gives you the right to hire your own certified appraiser. This professional will conduct a thorough, independent valuation of your vehicle, considering its pre-accident condition, features, and local market value. Their report serves as powerful evidence to counter the insurance company’s low assessment. An independent appraisal isn’t just another opinion—it’s a professional valuation that can force the insurer to justify their number or come back to the table with a much more reasonable offer.

Hire an Attorney to Fight for You

When an insurance company refuses to negotiate fairly, it’s often because they believe you’ll eventually give up. Hiring an attorney changes that dynamic immediately. A lawyer specializing in property damage claims signals to the insurer that you are serious about getting what you’re owed. They can take over all communication, present your evidence professionally, and dismantle the adjuster’s weak arguments. An experienced attorney understands the tactics insurers use and knows how to counter them effectively. This not only relieves you of the stress of fighting alone but also significantly improves your chances of receiving full and fair compensation for your vehicle.

File a Complaint with the State

Every state has a department that regulates insurance companies and protects consumers. In Georgia, you can file a formal complaint with the Office of Insurance and Safety Fire Commissioner. This action prompts a government agency to review your case and investigate whether the insurance company is acting in bad faith or violating state laws. While this process can take time, it puts official pressure on the insurer to justify their offer and negotiation tactics. Filing a complaint can be a very effective step, especially when combined with other strategies, as it shows the insurance company you are prepared to hold them accountable on all fronts.

How to Finalize Your Settlement

After all the phone calls, paperwork, and negotiation, you’ve finally reached a settlement amount you can agree on. This is a huge step, but the process isn’t quite over. Finalizing your settlement involves a few critical last steps to ensure you get your money and handle the vehicle’s title correctly. It’s tempting to rush through this part just to be done with it, but paying close attention to the details now will save you from major headaches later.

This final stage is where the insurance company will present you with a settlement agreement or a “release of all claims” form. This document is legally binding, and signing it means you agree to their terms and give up your right to seek any further compensation for this accident. That’s why it’s so important to understand exactly what you’re signing. We’ll cover what to look for in the fine print, how the payment process actually works, and what your options are for your car’s title. Each piece is important. Before you put pen to paper, let’s walk through what to expect so you can close out your claim with confidence and get the full property damage compensation you fought for.

Read the Fine Print: What the Terms Mean

The insurance company will send you a settlement agreement or release form. Read every single word before you sign. This document states the final settlement amount and legally releases the insurer from any future liability for the accident. Once you sign, you can’t come back later and ask for more money, even if you discover additional damage. You can always say no to an offer if the terms aren’t right. Before you finalize anything, make sure the document accurately reflects your agreement. If you have any doubts, it’s always a good idea to have an attorney review the paperwork before you sign.

Get Your Check: The Payment Process

Once you sign the release, the insurance company will process your payment. If your car is totaled, they will pay you its actual cash value (ACV), minus your deductible. However, if another driver was at fault, their insurance company should cover the full amount, and you won’t have to pay your deductible. The check is often made out to both you and your lienholder (the bank or credit union that financed your car). In this case, you’ll need to work with them to pay off the loan balance before you receive any remaining funds. Gastley Law handles these property damage claims to ensure you get every dollar you’re owed.

What Happens to Your Car’s Title?

When your car is declared a total loss, you have two main options. Most people surrender the vehicle to the insurance company. You’ll sign over the title, and they will take possession of the car and sell it for salvage. Your other option is to keep the car. If you do this, the insurer pays you the ACV minus both your deductible and the car’s salvage value. You will then receive a “salvage” or “rebuilt” title from the state. This permanently brands the vehicle, which is the ultimate form of diminished value and can make it difficult to insure or sell in the future.

Related Articles

Frequently Asked Questions

What if I owe more on my car loan than the insurance company is offering?

This is a tough situation known as being “upside down” on your loan, and it’s unfortunately common. The insurance company is only required to pay the car’s Actual Cash Value (ACV), not the balance of your loan. If their final offer is less than what you owe, you are still responsible for paying the difference to your lender. This is where having Guaranteed Asset Protection (GAP) insurance is a lifesaver, as it’s designed to cover this exact shortfall. If you don’t have GAP coverage, negotiating for the highest possible ACV becomes even more critical to minimize your out-of-pocket loss.

Can I really negotiate with the insurance adjuster myself, or do I need a lawyer?

You absolutely have the right to negotiate on your own behalf, and many people do so successfully by presenting solid evidence of their car’s true value. However, the process can be time-consuming and stressful. Adjusters are trained negotiators who handle these claims every day. If you feel like you’re not being taken seriously, if the adjuster is using high-pressure tactics, or if the gap between their offer and your car’s value is significant, bringing in an attorney can level the playing field and often leads to a better outcome without the headache.

How long should I expect this negotiation process to take?

The timeline can vary quite a bit depending on the complexity of your claim and how far apart you and the insurer are on the settlement amount. A simple negotiation where you provide clear evidence might be resolved in a week or two. However, if the insurance company is slow to respond or unwilling to budge from a low offer, it could take several weeks or even longer. The key is to be persistent and organized, but also patient. Rushing the process often means leaving money on the table.

Can I keep my car if the insurance company calls it a total loss?

Yes, in most cases you have the option to keep your vehicle. This is sometimes called “owner retention.” If you choose this path, the insurance company will pay you the car’s Actual Cash Value minus both your deductible and the vehicle’s salvage value (the amount they would have gotten for it at auction). The state will then issue your car a “salvage title,” which can make it difficult to get insurance or sell in the future. It’s a decision that requires careful thought about repair costs and future usability.

Why is the insurance company’s “Actual Cash Value” so much lower than what I need to buy a similar car?

This is the core of most total loss disputes. The insurer’s Actual Cash Value (ACV) is their estimate of your car’s market value the moment before the crash, based on their data. This figure often fails to account for your car’s specific condition, recent upgrades, or the current local market. The price you see on a dealer’s lot for a replacement car includes dealer prep fees, marketing costs, and profit margins, which aren’t part of the ACV calculation. That’s why doing your own research on what comparable private-party cars are selling for in your area is the best way to build a case for a higher, more realistic settlement.